NEWS

3 Jul 2026 - The underappreciated strength of European banks

|

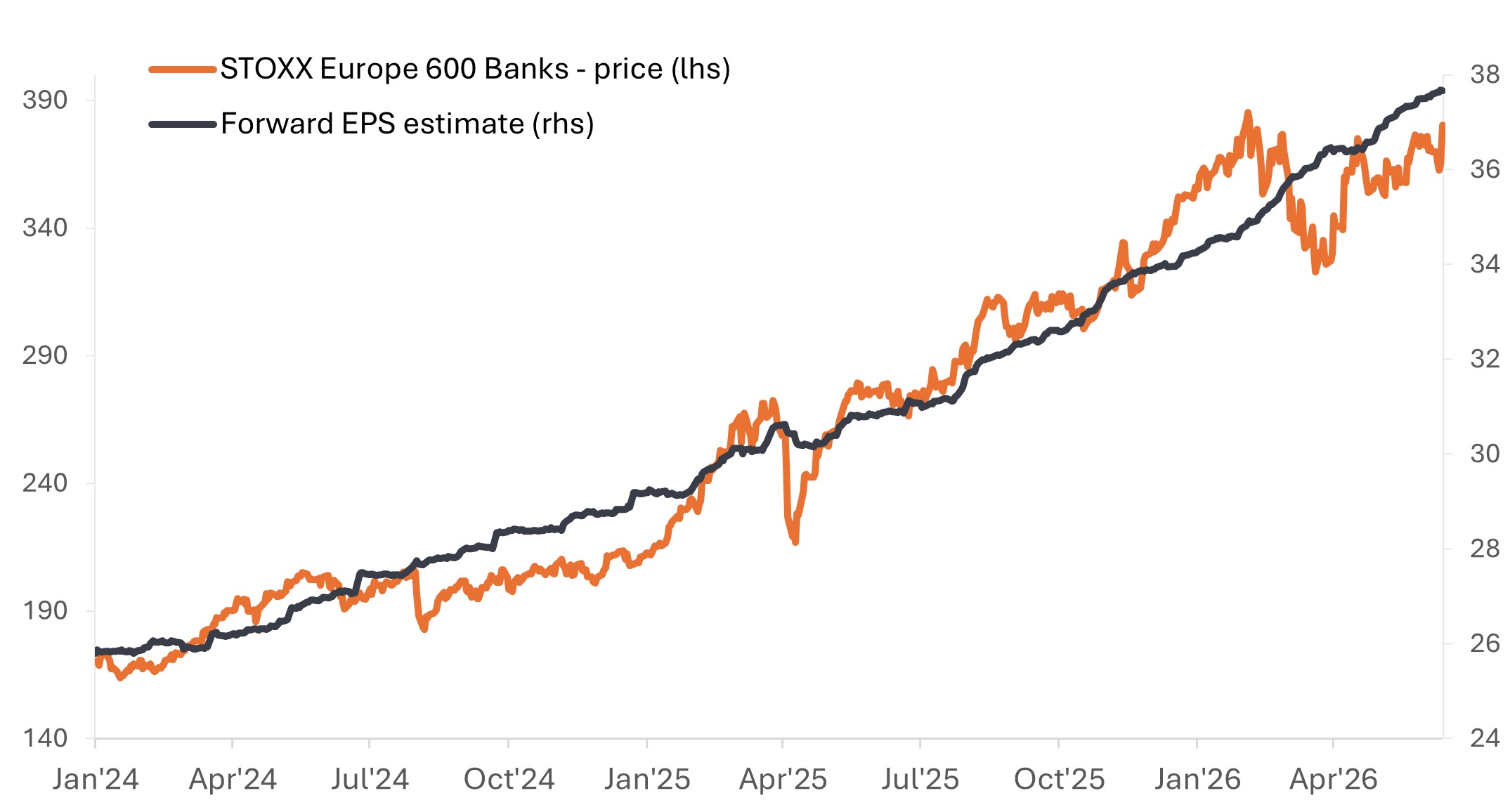

The underappreciated strength of European banks Janus Henderson Investors June 2026 (7-minute read) After more than a decade contending with the aftereffects of the Global Financial Crisis (GFC), European bank stocks have reemerged as one of the notable bright spots across the region's equity markets in recent years. In 2024 and 2025, the STOXX® Europe 600 Banks Index returned an impressive 35% and 77%, respectively, outperforming the broader STOXX® Europe 600 Index by more than 105 percentage points over that span.1 Importantly, this followed a long stretch of relative underperformance as tougher banking regulations and ultra-low interest rates weighed on profitability and loan growth. But while a low starting point and recognition of deeply depressed valuations - and subsequent multiple expansion - may explain some of the rally, improved fundamentals have been an underappreciated aspect of the story, in our view. Indeed, the rally over the last two years has been underpinned by earnings growth, as shown in the chart below. And while the Iran conflict injected a fresh dose of macro-driven volatility, valuations across the sector remain modest, and we believe the case for further rerating is firmly intact. Exhibit 1: Strong 2024 and 2025 performance driven by significant upward earnings revisions and multiple expansion

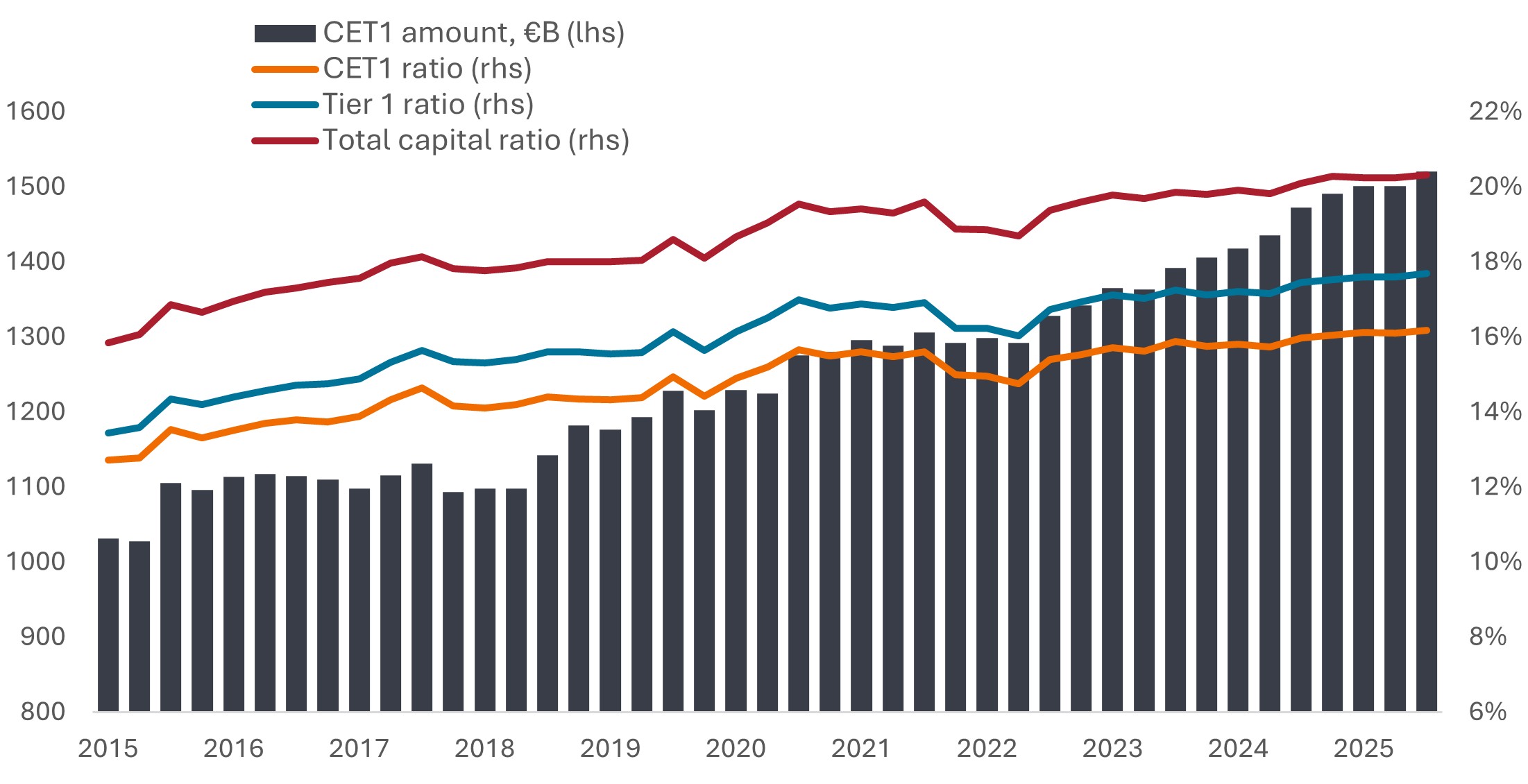

Source: Bloomberg, data from 1 January 2024 to 12 June 2026. Past performance does not predict future results. Emerging from a 15-year post-GFC deleveraging cycle In Europe, banks have spent more than a decade improving the size and quality of their capital reserves, as evidenced by a steady rise in Common Equity Tier 1 (CET1) levels and capital ratios (Exhibit 2). While this has supported banks' ability to weather exogenous shocks, it has also constrained lending, resulting in a period of muted - and at times, negative - loan growth. This, in turn, weighed on economic growth across the region, as banks provide the majority of financing to the corporate sector. More recently, there has been growing debate about whether the pendulum may have swung too far toward over-regulation. To date, progress toward deregulation has been limited, but discussions are underway around proposals to free up capital, support lending, and improve the competitiveness of European banks. Exhibit 2: European banks have built materially stronger capital positions

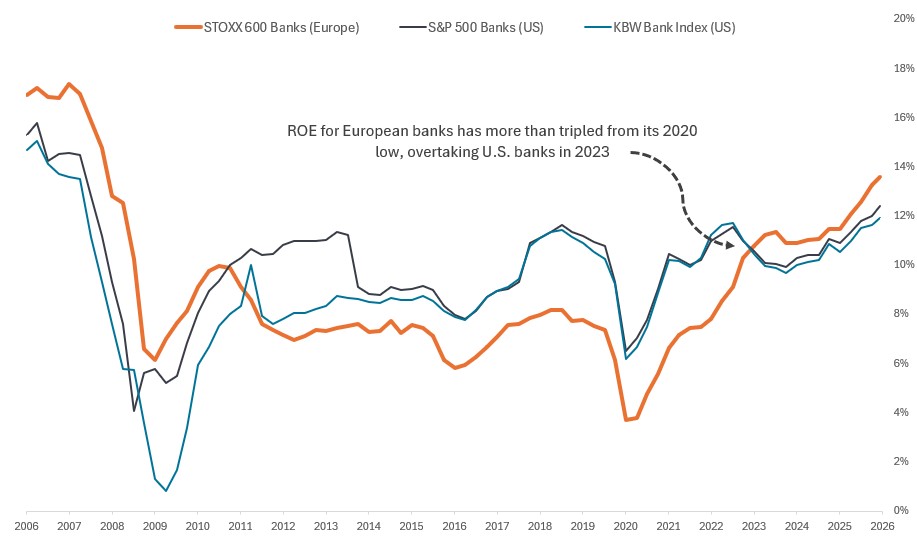

Source: ECB, "Supervisory Banking Statistics for significant institutions, fourth quarter 2025", 18 March 2026. At the same time, risk controls and cost-cutting measures honed during the days of negative rates have vastly improved many firms' operating efficiency. Loan books have also been significantly de-risked, with the non-performing loans ratio for significant institutions falling to roughly 2% in recent European Central Bank (ECB) data, down from more than 7% a decade ago.2 The upshot is that European banks have emerged from the prolonged deleveraging cycle as a healthier, more profitable sector, with higher interest rates providing an additional tailwind to earnings. A more constructive operating environment Consequently, the region's banks have been achieving their highest profitability of the post-GFC era, as measured by return-on-equity (ROE) levels. After bottoming in the mid-single-digits range in the aftermath of the pandemic, European banks have closed the gap with their U.S. peers and, in some cases, moved ahead for the first time in years. Exhibit 3: European banks have closed the profitability gap with U.S. peers

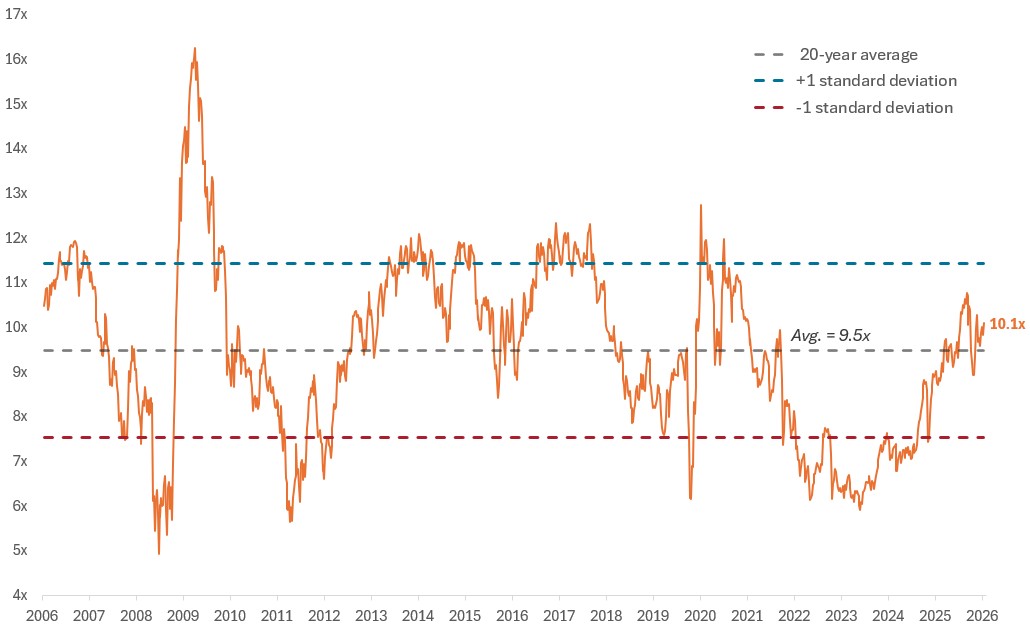

Source: Bloomberg, data as of 12 June 2006 to 12 June 2026. Past performance does not predict future results. Valuations suggest room for further rerating Despite this improved fundamental picture, European bank stocks continue to trade at a meaningful discount to U.S. banks and the broader European equity market. Although valuations have risen from deeply depressed levels, they have only recently returned to their long-term average.

Exhibit 4: European bank valuations are yet to fully reflect improved fundamentals

Source: Bloomberg, data as of 12 June 2006 to 12 June 2026. Past performance does not predict future results. Meanwhile, European banks have been returning capital to shareholders at a healthy clip in the form of dividends and share buybacks, with the dividend yield on the STOXX Europe 600 Banks Index north of 5%, more than double that of comparable U.S. benchmarks.4 All of this would argue in favor of room for further multiple expansion, in our view. While some discounting to U.S. peers may be warranted, we believe the persistently wide valuation gap also reflects anchoring bias - a tendency among investors to reference past underperformance when making investment decisions. Longer-term structural shifts and potential implications Beyond the improved earnings trajectory and still-attractive valuations, a combination of structural shifts and secular drivers is reshaping the investment landscape for European banks and could further support the case for additional upside.

While recent geopolitical turmoil has strengthened the case for European nations to boost defense spending - a potential tailwind that could support lending growth - the Iran conflict and resultant energy shock have cast a pall over the economic outlook for the region. The dual threat of higher inflation and potential demand destruction poses a risk for net energy-importing countries and bears close monitoring. The ECB responded on June 11 with its first rate increase since 2023, and markets are pricing in expectations for at least one additional rate hike this year, as of this writing. For now, the combination of modestly higher rates and still-resilient, albeit less-robust, economic growth aligns with the sort of environment in which banks typically thrive. That said, even with the recent Iran ceasefire extension, questions remain about how fully the Strait of Hormuz will reopen and the extent to which any lingering supply disruption could weigh on Europe and the broader global economy. This uncertain backdrop makes selectivity all the more critical. While we believe the case for further valuation rerating remains compelling, it is unlikely to be uniform across the European banking sector. In our view, deep fundamental research and bottom-up stock selection are essential to identifying institutions with strong capital positions, diversified earnings streams, and exposure to attractive markets supported by longer-term secular tailwinds. IMPORTANT INFORMATION Actively managed investment portfolios are subject to the risk that the investment strategies and research process employed may fail to produce the intended results. Accordingly, a portfolio may underperform its benchmark index or other investment products with similar investment objectives. Diversification neither assures a profit nor eliminates the risk of experiencing investment losses. Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments. Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition. Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund , Janus Henderson Conservative Fixed Interest Fund , Janus Henderson Diversified Credit Fund , Janus Henderson Global Natural Resources Fund , Janus Henderson Tactical Income Fund , Janus Henderson Australian Fixed Interest Fund - Institutional , Janus Henderson Conservative Fixed Interest Fund - Institutional , Janus Henderson Cash Fund - Institutional , Janus Henderson Global Multi-Strategy Fund , Janus Henderson Global Sustainable Equity Fund , Janus Henderson Sustainable Credit Fund All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

2 Jul 2026 - Performance Report: Equitable Investors Dragonfly Fund

[Current Manager Report if available]

2 Jul 2026 - Global infrastructure: Why a selective approach matters

|

Global infrastructure: Why a selective approach matters abrdn June 2026 (Reading time: 5 Mins) What if the biggest risk in infrastructure investing today is treating it as a single asset class? Historically, global infrastructure has been perceived as an asset class offering relatively stable and predictable returns which may vary depending on market conditions. Yet, as the asset class evolves in response to structural shifts such as decarbonisation, digitalisation, and changing supply chains, broad categorisations are becoming less useful. The infrastructure label alone no longer tells investors enough about revenue quality, risk transfer, policy exposure or long-term resilience. The key question is not simply whether an asset sits within an infrastructure sector, but whether it has the economic characteristics investors expect from infrastructure in the first place. A more nuanced investment universeInfrastructure today is not a monolith. It spans a diverse range of subsectors, each with distinct drivers, regulatory frameworks, and risk-return profiles. Traditional assets such as utilities and transport continue to play a core role, but they are increasingly complemented by newer areas like digital networks, district heat, equipment leasing and other energy transition solutions. Investors need to distinguish between assets with genuinely defensive infrastructure characteristics and those that may simply be exposed to attractive themes. In this context, we believe a selective approach is becoming essential. Investors need to distinguish between assets with genuinely defensive infrastructure characteristics and those that may simply be exposed to attractive themes. This enables a clearer understanding of where risks lie - and where opportunities may be underappreciated. DecarbonisationOpportunity with complexityOne of the most powerful forces reshaping infrastructure is the global energy transition. Governments and corporates are accelerating efforts to decarbonise, driving significant capital investment into renewables, grid modernisation, energy efficiency and the wider infrastructure needed to make lower-carbon systems reliable and affordable. A selective perspective helps investors distinguish between different risk profiles, allowing for more targeted allocation. However, this opportunity set is far from uniform. In our view, the dispersion in renewable returns is being underestimated depending on geography, regulatory support, and technological maturity. Some assets benefit from long-term contracted revenues, while others are more exposed to merchant pricing, grid constraints and policy evolution. A selective perspective helps investors distinguish between these different risk profiles, allowing for more targeted allocation. It also helps avoid the assumption that every asset associated with the transition automatically offers infrastructure-like downside protection. Digital infrastructure comes of ageAt the same time, the digital economy is transforming what constitutes infrastructure. The rapid growth in data consumption has fuelled demand for fibre networks, towers, and data centres. Some of these assets exhibit infrastructure-like characteristics, including high barriers to entry, essential demand and long-term contracts. For investors, the distinction between durable digital infrastructure and technology-led growth exposure is increasingly important. Yet these assets are not without their own complexities. Technological change, evolving customer requirements, and competitive dynamics can all influence long-term value. Understanding these factors at a detailed level is critical to identifying assets that combine structural growth with durable cash flows. Rethinking transport and logisticsTransport infrastructure, long a cornerstone of the asset class, is also evolving. While passenger volumes have recovered unevenly in the wake of the pandemic, longer-term trends such as remote working and decarbonisation are reshaping demand patterns. Meanwhile, freight and logistics infrastructure has gained prominence, supporting changing supply chains and demand for more resilient networks. Here again, selectivity matters. Assets supported by contracted, availability-based or take-or-pay revenues can have a very different risk profile from those exposed mainly to volumes or discretionary demand. Regulation and inflationDetail mattersRegulation remains a defining feature of infrastructure investing, but its influence is becoming more complex. Policymakers must balance attracting private capital with achieving social and environmental objectives, creating both opportunities and risks. A detailed, bottom-up approach is essential to assess (revenue linkage, contract structures, and regulatory mechanisms) accurately. Inflation adds another layer of nuance. While infrastructure is often viewed as a potential hedge against rising prices, the degree of protection varies. Some assets benefit from explicit indexation, while others rely on pricing power, regulatory resets or contract renegotiation. Revenue linkage, contract structures, cost pass-through and regulatory mechanisms all play a role in determining how effectively inflation protection works in practice. A detailed, bottom-up approach is essential to assess these dynamics accurately. The case for active, selective investingIn an increasingly diverse and complex asset class, active management is gaining importance. Broad or passive approaches may overlook the dispersion of returns across subsectors and geographies. By contrast, a selective strategy grounded in detailed analysis can better identify mispriced opportunities, anticipate regulatory shifts, and allocate capital to areas with the strongest long-term fundamentals. For us, this means focusing on assets where essential-service demand, defensible revenues and active ownership can combine to create value, rather than relying on thematic growth alone. This also enhances diversification, ensuring that portfolios are constructed from assets with genuinely complementary characteristics, rather than simply broad exposure. Final thoughtsThe case for global infrastructure remains compelling, underpinned by a significant investment gap across energy, digital connectivity, and urban development. However, capturing these opportunities requires a more sophisticated approach than broad asset-class exposure can provide. As the market evolves, success will depend on moving beyond high-level classifications and focusing on the assets that genuinely combine essentiality, resilience and growth, embracing a more selective perspective. For investors, this shift is not only about managing risk. It is about accessing the best of what infrastructure can offer in a rapidly changing world. |

|

Funds operated by this manager: abrdn Sustainable Asian Opportunities Fund , abrdn Emerging Markets Equity Fund , abrdn Sustainable International Equities Fund , abrdn Global Corporate Bond Fund (Class A) |

1 Jul 2026 - Monthly Market Commentary

|

Monthly Market Commentary Arculus Funds Management June 2026 (3-minute read) Monetary Policy & Rates The RBA held the cash rate steady this month following three consecutive 25bp increases to open the year, a unanimous decision that Governor Bullock paired with an acknowledgement the economy still carries "a bit of excess demand." We read the pause as genuine, not the end of the cycle. Our central case is that the Bank remains on hold through the second half of the year before delivering a further 25bp increase in the December quarter - a move we expect to be driven by cost-push inflation crystallising even as the broader economy looks lacklustre. Underlying inflation is building beneath a softer headline The case for a final hike is building beneath a softening headline. May headline inflation fell to 4.0% YoY, but almost entirely on a 12% fall in fuel and a 6.9% drop in travel prices; the trimmed mean rose to 3.6% YoY, the high of its series. The persistence sits in roughly a third of the basket and is supply- and cost-side in character: new dwelling construction is running at 5.6% YoY - its fastest since mid-2023 and adding some 42bps to headline inflation on its own - while rents are reaccelerating toward 4% and market services inflation remains broad-based. Critically, this is all evident before the Fair Work Commission's 4.75% award wage increase - which lifts pay for around a fifth of the workforce - takes effect on 1 July (the concurrent ~6% rise in the National Minimum Wage reaches under 1% of employees and is macroeconomically immaterial). We expect that award step-up to feed market services through the second half, with the late-October Q3 CPI the most likely trigger for the Bank to move. A hike into a cooling economy That this tightening would land into a cooling economy is, in our view, the defining feature of the outlook rather than a contradiction of it. The housing downturn has begun, hours worked softened in the month, and household spending is growing at its slowest pace in a year. Yet the labour market remains genuinely tight: unemployment fell back to 4.4% as April's spike reversed, employment rebounded 40k, and broader spare-capacity measures - underutilisation at 10.2%, underemployment near its cycle low - sit at generational tights. A central bank facing sticky, cost-driven inflation against a still-tight labour market has limited room to look through it, weak demand notwithstanding. The 2027 risk: a wage-price spiral Beyond the December move, we see a credible path to a second 25bp increase during 2027, though we treat it as conditional and sequenced. The first condition is that money supply growth remains strong, sustaining the monetary impulse behind demand; only if that holds does the second condition - a broadening in wages growth - become the mechanism that converts cost-push pressure into a self-reinforcing wage-price dynamic. Absent strong money supply growth, we would not expect wages alone to force the Bank's hand. We flag this as a risk case rather than our base but note it runs directly counter to prevailing assumptions of an easing cycle from late 2027. On our trajectory the next move is up, then held, and the eventual cut sits materially later than consensus. Positioning With the market pricing only around 8bps of tightening over the next twelve months, we regard the front end as under-pricing both the December hike and the medium-term risk profile. This is a higher-for-longer environment, and we continue to favour carry and income over duration, with elevated BBSW reflecting a rate path that has further to climb before it turns. Funds operated by this manager: |

30 Jun 2026 - Performance Report: Insync Global Quality Equity Fund

[Current Manager Report if available]

29 Jun 2026 - Performance Report: Bennelong Emerging Companies Fund

[Current Manager Report if available]

29 Jun 2026 - 10k Words | June 2026

|

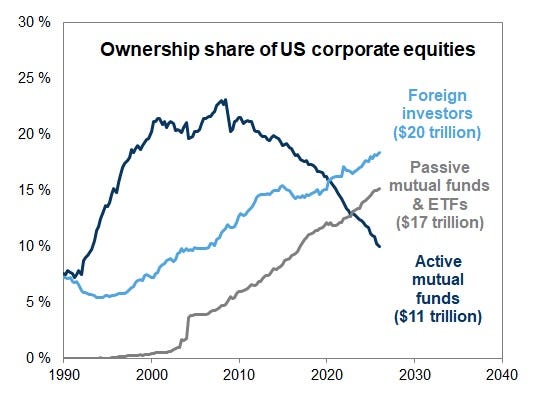

10k Words Equitable Investors June 2026 (2-minute read) A takeover of the US equities market by foreign investors and passive vehicles; leading into the equal-weighted index lagging. Demand for power surging as free cash flow generation at the "Mega Tech" collective goes the other way; fund managers' most crowded trade amid all that is semi-conductors; and AI attracts new founders like moths to the flame. The value of US equities and housing is at record levels relative to GDP; but investor sentiment remains positive; and the number of investors expecting multiple expansion is evenly balanced with those predicting contraction. Elsewhere, we see evidence of softness in the Australian employment market and the widened gap between the top decile and bottom decile of US consumers. Ownership share of US corporate equities

Source: FT.com, Goldman Sachs Ratio of the equal-weighted S&P 500 to the S&P 500 index is down to 1.1, near the lowest since 2003

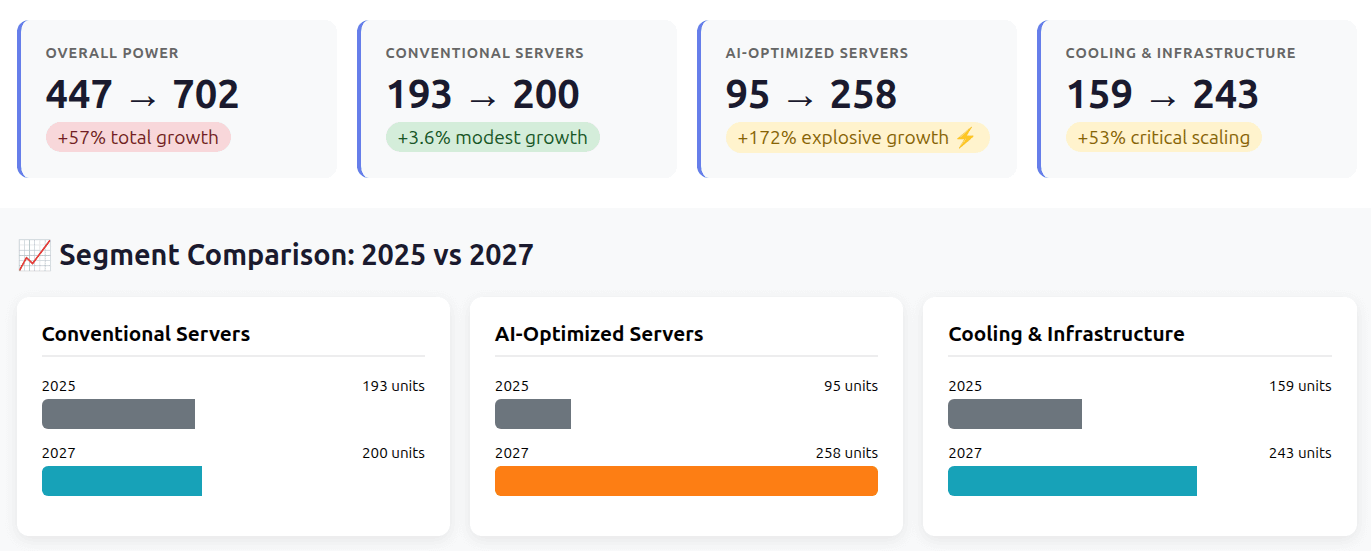

Source: The Kobeissi Letter, TheDailyShot Worldwide data centre power consumption projections (TWh): 2025 - 2027

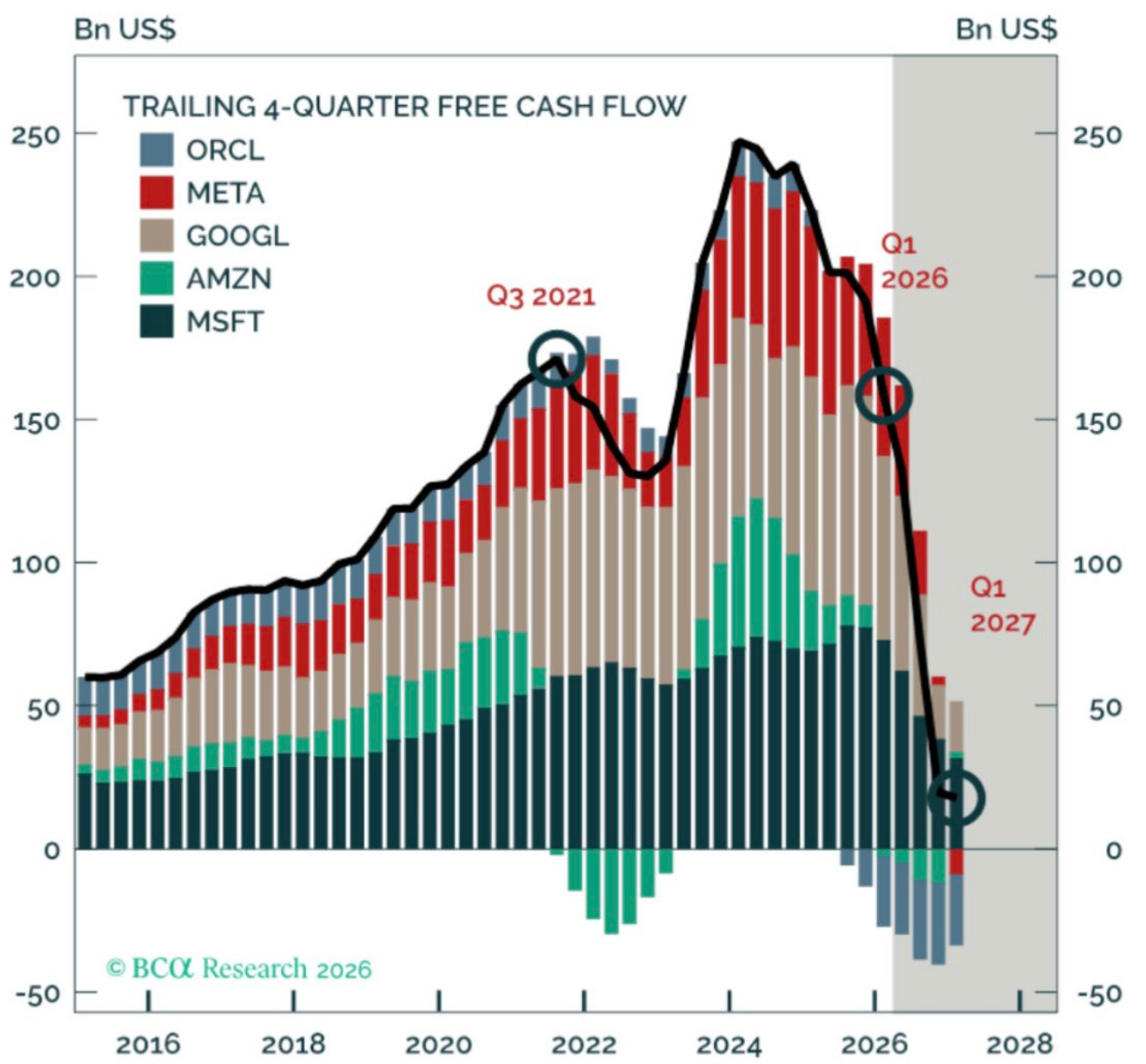

Source: Equitable Investors, Gartner "Mega Tech" free cash flow diminished - "capital light" model gone

Source: BCA Research Most crowded trade

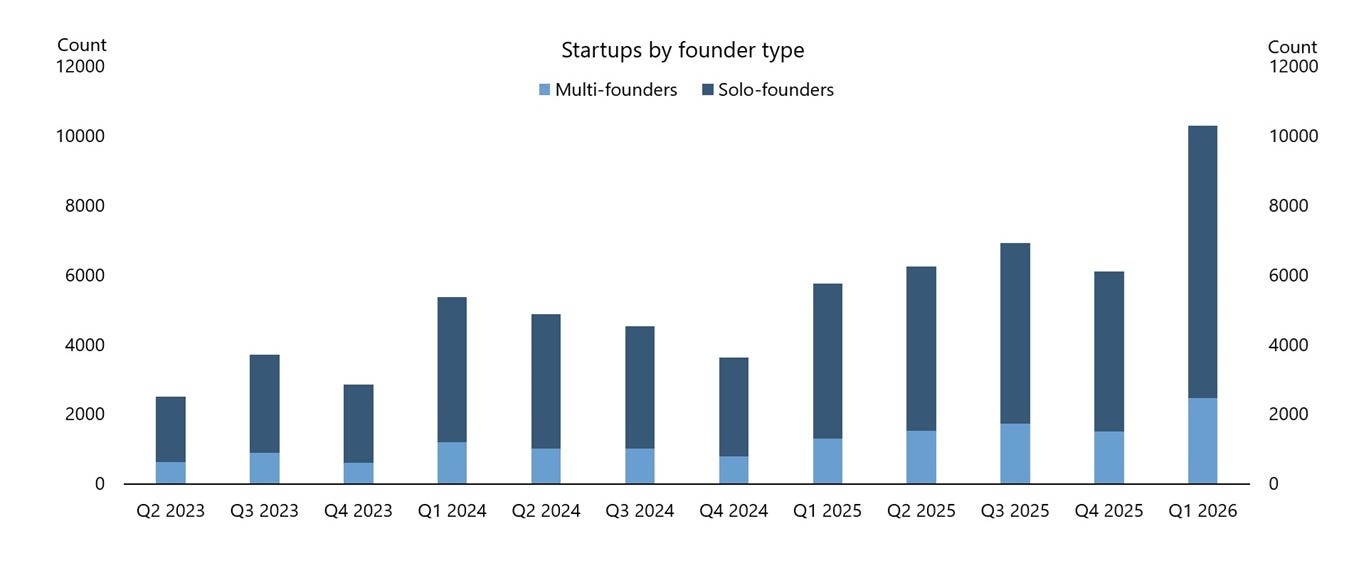

Source: Bank of America Fund Manager Survey AI-driven surge in number of startup founders

Source: Apollo Value of US equities and housing stock relative to GDP

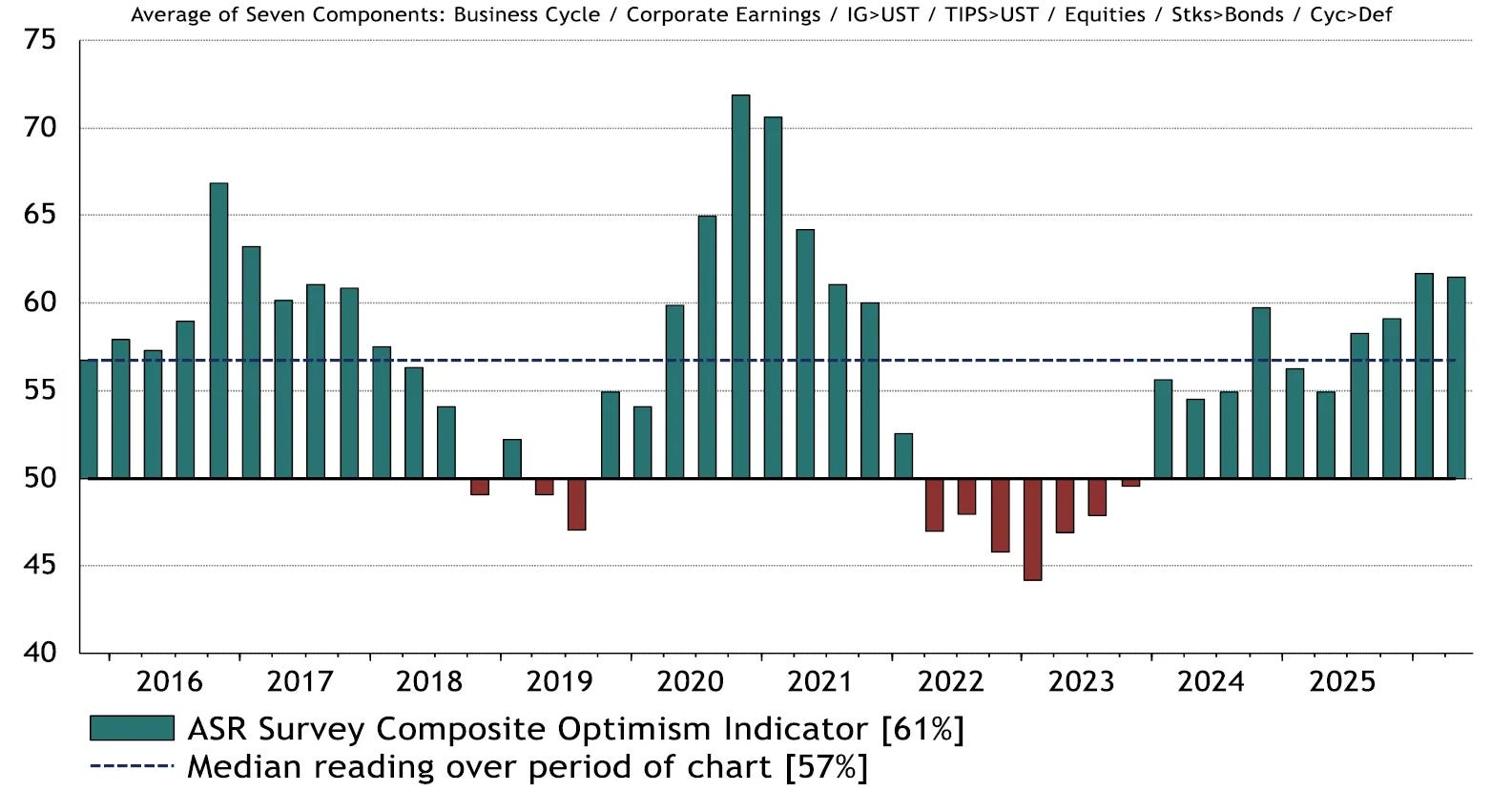

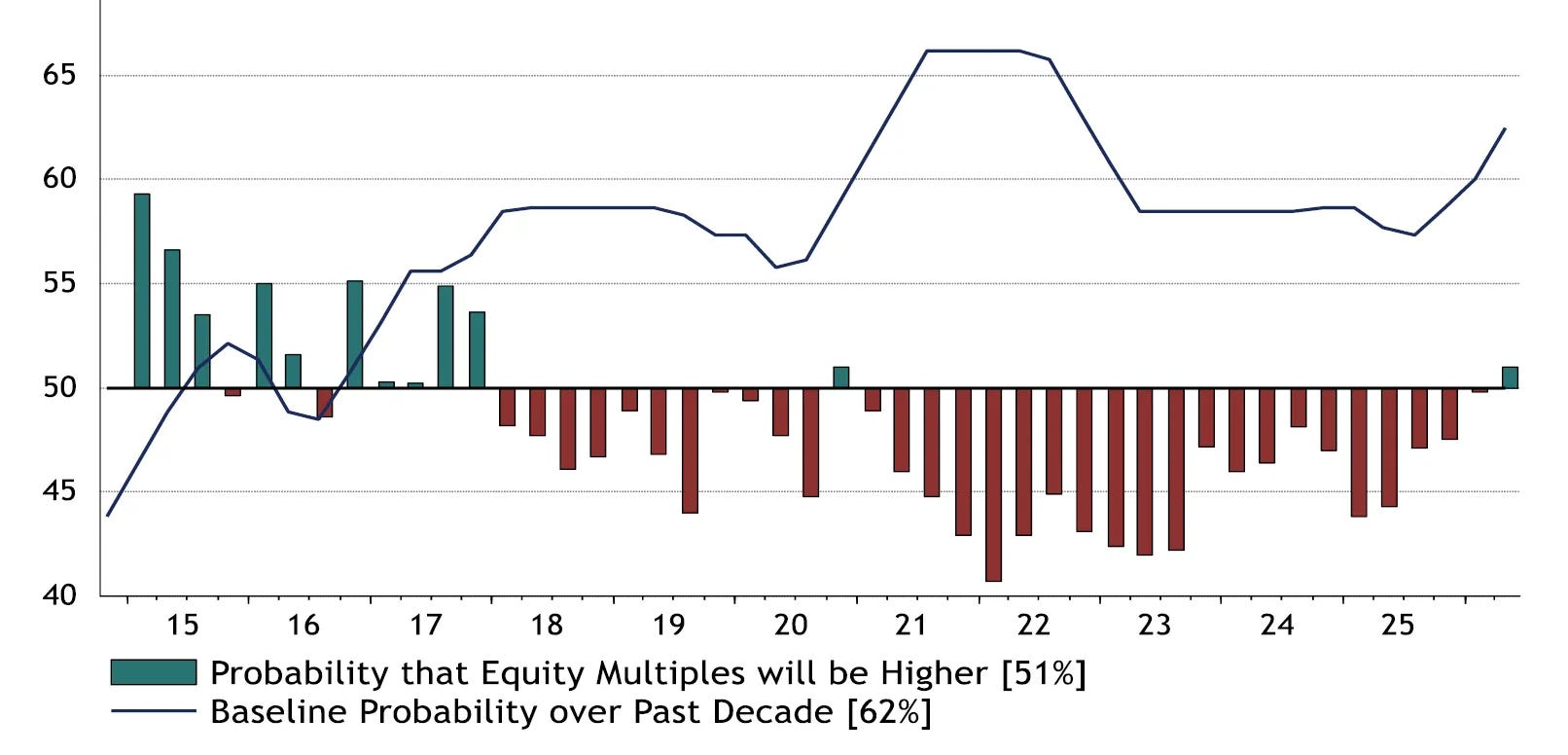

Source: re:venture ASR Asset Allocation Survey - composite optimism indicator

Source: Bloomberg, Absolute Strategy Research Survey on probability that global equity multiples will be higher a year from now

Source: Bloomberg, Absolute Strategy Research Seek Employment Index - May 2026

Source: Seek US consumer spending by income percentile

Source: FT.com, Moody's Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

26 Jun 2026 - Hedge Clippings |26 June 2026

|

|

|

|

Hedge Clippings | 26 June 2026 Central banks are trying to sound calm. Markets are trying to sound confident. Neither looks entirely convincing. RBA | Waiting is not relief The Reserve Bank left the cash rate unchanged at 4.35%, but nobody should have confused that with comfort. After a year of policy reversals, first down, and then back up, the Board is now in the only other position available: waiting. That is not the same as relief. More a case of being stuck between a rock and a hard place. The latest inflation data gave both sides of the argument (and politics) something to cling to. Annualised headline CPI fell to 4.0% in May, helped by fuel-price effects, which was quickly treated in some corners as evidence that pressure is easing. The more important number, however, was the trimmed mean, which rose to 3.6% and reached its highest level since September 2024. That is the measure the RBA watches most closely, and as the chart above shows, it is not moving in the right direction. The difficulty the RBA has at this point in the cycle - apart from inflation remaining above their 2-3% trimmed mean target - is that they can see more volatility to pricing ahead. In July the fuel excise respite is due to halve, and at some stage will be removed altogether. While hostilities in the Middle East have abated (for now) it is going to take some time for the aftermath of the war, and its effects on supply driven inflation, to work through the system. The only certainty seems to be uncertainty. The labour market adds to the ambiguity. May employment rose by 40,300, which looks solid at first glance. But 35,200 of those jobs were part-time, while total hours worked fell. Unemployment eased to 4.4% from April's 4.5%, but this is not a labour market roaring back to life. It is a labour market holding headcount while reducing hours. That matters. It gives the RBA no clean reason to cut, and no urgent reason to hike. Instead, it keeps the Board exactly where it has been: staring at the next inflation print and hoping the economy does not force its hand. However, according to Renny Ellis from Arculus Funds Management, the market is only pricing in around 8 bps of tightening over the next 12 months, which he believes is under-pricing the medium-term risk of a "higher for longer" environment, which in his view is leading to a further rate rise in Q4 this year. Ellis also sees the risk of "a credible path to a second 25bp increase in 2027" as being possible. You can read his Market Commentary via this link. Property | The policy squeeze arrives before the policy changes The housing market is already showing strain. The combined capitals' preliminary auction clearance rate fell to 47.4%, the lowest weekly reading since April 2020. That is not a market looking through rate hikes. It is a market absorbing them. Sydney and Melbourne remain the key pressure points. Affordability is stretched, borrowing capacity has been hit, and consumer confidence has not been helped by the Budget's changes to negative gearing and capital gains tax. National home values were flat in May, while Sydney values are already below their November 2025 peak. The important point is that the tax changes have not yet landed. The CGT discount reform and negative gearing restrictions are not due to apply until July 2027, while the SMSF residential LRBA ban is expected around August 2026. The current weakness is therefore a combination of rate-driven, combined with investors reacting to uncertainty and fear of the tax reforms that will bite later. If consumer confidence deteriorates further, the property market could shift from a source of household wealth comfort to a source of household anxiety very quickly. Chalmers can argue about the technicalities of the property market being in a correction or not, but the reality for homeowners with a high LVR, or selling their house into a softening market are feeling the reality pinch. The bottom line This was a week of misleading headlines and uncomfortable details. Headline inflation fell, but underlying inflation rose. Jobs grew, but mostly part-time. GDP expanded, but only because data-centre investment did the heavy lifting. Property softened before the major tax reforms have even begun to bite. For investors, the lesson is familiar. Volatility does not just reveal market direction. It reveals process. It shows which managers are relying on beta, which are managing risk, and which have a framework strong enough to survive when the story changes. That is where FundMonitors matters. Weeks like this are exactly why manager research, peer comparison and performance analysis are worth doing properly. News | Insights Is the Consensus on Equities the Riskiest Trade in the Room? | East Coast Capital Management Market Commentary | Glenmore Asset Management May 2026 Performance News Seed Funds Management Financial Income Fund DAFM Digital Income Fund (Digital Income Class) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

26 Jun 2026 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]