NEWS

16 Oct 2024 - Glenmore Asset Management - Market Commentary

|

Market Commentary - September Glenmore Asset Management October 2024 Globally, equity markets were broadly positive in September. In the US, the S&P 500 rose +2.0%, the Nasdaq increased +2.7%, whilst in the UK, the FTSE declined -1.7%. In Australia, the All Ordinaries Accumulation Index outperformed, rising +3.5%. The top performing sectors on the ASX were resources and technology, whilst healthcare was the worst performer. Resources was boosted by news of stimulus from the Chinese government, following a period of weak economic growth, whilst technology benefited from lower bond rates as the US Federal Reserve commenced its easing cycle. Notably, small caps outperformed large caps on the ASX (ASX small ords increased +5.1%) as investor risk appetite improved. As discussed, a key event for equity markets in September was the US Federal Reserve cutting interest rates by 0.5% due to inflation reaching acceptable levels and a slowing economy. Whilst the event was expected by the markets, it is still an important milestone for equities, particularly small/mid cap stocks. Currently, Australia is not as close to rate cuts as the US, however we believe some easing in monetary policy is likely in the next 9-12 months. In bond markets, the US 10 year government bond yield fell -8 basis points to 3.78%, whilst in Australia the 10 year bond rate was flat at 3.97%. Funds operated by this manager: |

15 Oct 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

||||||||||||||||||||||

| Dimensional Global Core Equity Trust (AUD Hedged Class) - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional Global Core Equity Trust (Unhedged Class) - Active ETF | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional Emerging Markets Sustainability Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Emerging Markets Value Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Global Large Company Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Vanguard Balanced Index Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 850 others |

14 Oct 2024 - Manager Insights | Altor Capital

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Benjamin Harrison, Chief Investment Officer at Altor Capital. The Altor AltFi Income Fund has a track record of 6 years and 5 months and has outperformed the RBA Cash Rate + 5% benchmark since inception in April 2018, providing investors with an annualised return of 11.68% compared with the benchmark's return of 6.67% over the same period.

Disclaimer This video presentation (the "Content") has been prepared by Australian Fund Monitors Pty Ltd, "AFM" (AFSL 324476) and has been prepared without taking into account the investment objectives of the viewer or recipient. The Content is intended for information purposes only, and recipients should conduct full research and take appropriate advice prior to making any investment decisions. The Content is believed to be accurate at the time of publication, but past performance is not guaranteed. Copyright, Australian Fund Monitors Pty Ltd. October 2024. |

11 Oct 2024 - Are high grade bonds a natural choice for strengthening your fixed income allocation

|

Are high grade bonds a natural choice for strengthening your fixed income allocation JCB Jamieson Coote Bonds September 2024 In a rapidly evolving macroeconomic landscape, Australian investors are increasingly turning to global high grade government bonds as a highly defensive component of their investment portfolios. This move is predominately driven by global government bond markets offering greater portfolio diversity, enhanced return potential and broad sources of yield. In this article, we unpack the key themes influencing investors' long-term views on the value of including global high-grade bonds into a fixed income portfolio. Where are we now in the cycle?The key question facing investors today is: Where are we in the current business cycle, and when will the next shift occur? A glance at the economic growth of the world's major economies and stock markets over the past decade reveals that we've been in an extended expansionary phase. However, determining exactly when the cycle will peak is notoriously difficult. While certain indicators have pointed to an approaching recession, accurately predicting this shift remains a challenge. At a time where geopolitical tensions are intensifying and policy makers are grappling with softening global growth and persistent inflation, investors face a landscape of heightened uncertainty on many fronts. Global central banks are embarking on a synchronized interest rate cutting cycle as the narrative has switched this year from inflation concerns to growth concerns. Global inflation has moderated from its peak levels, with current annual rates of inflation at 2.50% in the US (the lowest since February 2021), 2.00% in Canada, 2.20% in the UK, 2.20% in EU and 3.8% in Australia, although forecasted to fall to 2.70%. Meanwhile economic growth has started to show some cracks, which until now has been supported by government spending. Employment remains a key determinant in the direction of growth and recent signs from the US indicate that this is turning. US employment data was recently sharply revised lower - which has triggered anxiety amongst central bankers. In response, they are eager to get on the front foot and curb labour market weakness before it deteriorates sharply. Savings are already getting depleted, and signs of rising delinquency are cautionary tales that will be exacerbated from job losses. Asset allocations can be dynamically adjusted to optimise performance during different phases of the cycle. With the recent loss of US employment momentum, are we moving from Slowdown to Recession? If so, improving asset quality and liquidity will be important to navigate the coming market environment. Chart 1: Phases in the business cycle.The economic cycle consists of four key phases: Boom, Slowdown, Recession and Recovery, which then leads back to another Boom - continuing the cycle.

Expanding horizons: Unlocking enhanced alpha opportunities that may awaitNot all bonds are created equal. High quality sovereign global bonds offer a lower risk profile due to their stability and creditworthiness. These bonds are typically issued by governments with strong financial standing, making them less susceptible to default and economic fluctuations compared to lower-rated or corporate bonds. As a result, they can serve as a safer option for investors seeking to mitigate risk within their portfolios. Global high grade bonds currently present unique alpha opportunities for investors.

Chart 2: Global Government Bonds Have Outperformed International Equities During Major Sell-OffsGlobal government bonds are among the safest investments in an investor's portfolio, offering capital preservation and helping to reduce equity volatility due to their long-term negative correlation with stocks. They also provide stability to portfolios, especially during market downturns. We can observe how global sovereign bonds perform during periods of financial market crises and significant events in the chart below. During the dot-com crash, the global financial crisis and European debt crisis, global government bonds outperformed equities providing capital preservation and a hedge against the equity market collapse. During the COVID-19 pandemic, global sovereign bonds and equities once again exhibited contrasting performances, although the dynamics were more complex than during previous crises. The pandemic caused a sharp, short-term market shock in early 2020, followed by an unprecedented recovery, largely driven by aggressive fiscal and monetary stimulus.

Source: JCB team analysis based on data from Bloomberg. How should investors position fixed income portfolios as global rate cuts begin?When considering the long-term value of fixed income, high grade bonds stand out as one of the safest investments in an investor's portfolio. Not only do they preserve capital but also help reduce equity volatility due to their long-term negative correlation with stocks, ultimately stabilising portfolios during tough market conditions. We believe that now could be an ideal time to lock in elevated income levels and broaden fixed income portfolios to include a variety of global bonds. The onset of the cutting cycle is likely to lead to a decrease in bank deposit rates, making government bonds a more attractive option for investors seeking capital appreciation. As a significant amount of dollars currently parked in money market funds is expected to flow into the government bond sector, this shift is further supported by the frothy nature of the private credit market, which has more than doubled in size since 2019. Interest rate cuts mean private credit's floating rate is less attractive, redirecting capital away from it into higher interest bearing assets. The transparency and liquidity of government bond funds provide a compelling argument for this reallocation. Adapting to market changes: why global sovereign bonds matter nowFalling interest rates signal a shifting investment landscape, presenting new opportunities for asset allocators. Rate cutting cycles underscore the importance of diversification, especially as economic conditions can change rapidly. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A), CC Jamieson Coote Bonds Dynamic Alpha Fund, CC Jamieson Coote Bonds Global Bond Fund (Class A - Hedged) |

10 Oct 2024 - ESG Insights: China emerges as green energy leader.

|

ESG Insights: China emerges as green energy leader. Tyndall Asset Management September 2024 I recently spent a few days in Hong Kong meeting with Asian companies and experts to explore China's economic shift from relying predominantly on infrastructure and real estate to its emergence as a global leader in renewable energy. Government policies support emerging industriesChina's rapid economic growth over the last few decades has been driven by investment, infrastructure development, and real estate. In 2021, real estate investment accounted for 27% of China's total fixed asset investment, but by 2023, this figure had fallen to 22% and is arguably even lower today. The sector has faced shrinking investments, declining sales, and a notable drop in housing prices. Between January and July 2024, real estate development investment decreased by 10.2% year-on-year (YoY) to RMB 6.09 trillion. The gross floor area (GFA) of new construction starts also saw a significant decline, with a 23.2% YoY decrease, while the GFA of completed projects dropped by 21.8% YoY. Although real estate remains a significant contributor to the economy, the Chinese government has been actively working to diversify the country's economic drivers. The government has introduced policies aimed at reducing payments and interest rates on property loans to prevent a collapse in the real estate market, which remains a vital part of China's economy. At the same time, the government has implemented significant reforms and provided incentives to encourage the growth of key industries such as EVs, solar energy, and lithium-ion batteries. These new sectors are crucial not only for domestic growth but also for China's goal to become a global leader in renewable energy and green technologies. I will discuss two of these industries in further detail in this paper. Global leader in EV manufacturingThe electric vehicle (EV) sector is a cornerstone of China's new industrial policy. As the world shifts toward cleaner energy, China has positioned itself at the forefront of the EV revolution. By 2024, domestic EV penetration had surpassed 50%, reflecting the growing consumer demand for environmentally friendly alternatives to internal combustion engine (ICE) vehicles. The Chinese government's push for sustainable transport has been instrumental in shaping this industry. However, subsidies are no longer the primary source of EV growth, as these vehicles have become competitive with ICE cars. The rapid growth of China's EV market is one of the most significant trends in the country's industrial landscape. In 2023 alone, EV sales in China reached 7.8 million units, representing a significant share of the global EV market. This growth has been driven by several factors, including government subsidies, the development of battery technology and an extensive charging infrastructure network. Additionally, Chinese consumers are increasingly favouring EVs over ICE vehicles. China's EV market is not only expanding domestically but is also influencing global markets. Chinese automakers such as BYD, Li Auto, and NIO are rapidly gaining market share within China and overseas. Chinese EV manufacturers have overtaken many traditional automakers in sales and technological innovation, with BYD now ranked fifth in global EV sales. However, Chinese automakers face challenges in expanding globally, due to the impact of trade barriers and tariffs. In 2024, the European Union imposed tariffs up to 38% on EVs imported from China, while the United States and Canada have also increased tariffs on Chinese EVs. The US and Canada appear to be particularly concerned about the software within the vehicles with a built-in internet connection. The issue relates to concerns on Chinese companies collecting data on American drivers and infrastructure together with the potential for foreign adversaries to remotely manipulate connected cars on the US roads. Overcapacity increases price competitionThe Chinese government's massive investments in EV manufacturing have resulted in an oversupply of vehicles. Many companies, particularly smaller startups, are struggling to maintain profitability due to the high cost of production and competition from established players. While companies like BYD and NIO have scaled production efficiently, others are facing challenges with underutilised capacity and financial losses. This overcapacity has led to price competition, with many manufacturers slashing prices to maintain market share. This has resulted in thin profit margins across the industry, particularly for companies still in the early stages of scaling production. China dominates solar energy productionSolar energy is another key sector in China's energy transition. China is the world's largest producer of solar panels, accounting for over 90% of global production. Between 2021 and 2023, China's solar capacity more than doubled, driven by strong demand and technological innovation. The country added over 200 gigawatts (GW) of solar capacity during this period, making it the largest solar energy producer in the world. The Levelised Cost of Energy (LCOE) for solar power has dropped significantly, making it cost-competitive with traditional energy sources such as coal and natural gas. By 2023, the LCOE for solar power in China fell to just $0.04 per kilowatt-hour, on par with the cost of coal-fired electricity. Chinese companies have improved solar efficiency while reducing production costs, making solar energy more affordable and accessible. This has enabled China to export its solar products globally, particularly in Europe, Asia, and the Americas. One of the most significant innovations in the solar industry has been the development of "N-type" solar cells, which offer higher conversion efficiency than traditional "P-type" cells. These advanced solar cells have helped reduce the overall cost of solar energy, making it more competitive with other forms of electricity generation. Despite this impressive growth, China's solar industry faces similar challenges to the EV industry. The rapid expansion of production capacity has led to an oversupply of solar panels, causing prices to plummet. Between 2021 and 2023, the average cost of solar panels fell by more than 60%, squeezing manufacturers' profit margins. To address overcapacity, the Chinese government has implemented policies encouraging consolidation within the industry. Smaller, less efficient producers are encouraged to exit the market, while larger companies expand their market share. This process of consolidation is expected to help stabilise prices and improve profitability in the long term. Expansion into global marketsChina's solar industry is also expanding its presence in international markets, particularly in Southeast Asia and the Middle East. Chinese companies such as Longi, Jinko Solar, and Trina Solar have established production facilities in countries like Malaysia, Vietnam, and Thailand, where they can benefit from lower production costs and favourable trade policies. In the Middle East, these companies are scaling up operations to meet the region's growing demand for renewable energy. The United Arab Emirates and Saudi Arabia have become key markets for Chinese solar products. China's dominance of the Global Battery marketThe rise of electric vehicles (EVs) has significantly increased the global demand for lithium-ion batteries. As countries strive to transition to cleaner energy sources, the battery industry has become a critical component of this shift. China has emerged as a dominant force in battery production, contributing to a substantial oversupply in the market. China's battery production capacity in 2023 alone matched global demand, highlighting its overwhelming presence in the industry. The country has invested heavily in research and development, with companies like BYD and CATL leading the charge. This dominance is not just in sheer volume but also in technological advancements, making China a formidable player in the global battery market. Global lithium-ion battery manufacturing capacity has outpaced demand, with an estimated 2,600 GWh produced in 2023 against a demand of 950 GWh. This oversupply is expected to increase, leading to falling prices and squeezing profit margins for manufacturers. For consumers, this could mean more affordable EVs and stationary storage solutions. The low prices are making it difficult for new entrants outside of China to compete, even with generous support provided by the US Inflation Reduction Act and other such support structures. The sustainability of the low battery prices is an intriguing question and will likely result in an industry shakeout as is normal during overcapacity cycles. Lithium, a key raw material cost is in over supply and thus helping keep battery prices low. However, regulatory and environmental approvals are making it more difficult to bring on new mining or refining capacity than build a battery plant. This may help bring the supply and demand fundamentals back into balance. ConclusionChina's industrial transition represents a fundamental shift in its economic model, as the country moves away from traditional investment-driven sectors like real estate and toward new, innovative industries such as EVs, solar energy and lithium-ion batteries. These sectors are crucial to China's long-term economic sustainability and its efforts to reduce carbon emissions and become a global leader in green technology. Exports of the traditional labour-intensive products are declining due to falling competitiveness. However, the capital and technology intensive industries are rapidly filling the gap. This transition is not without its challenges. EV, lithium-ion battery and solar industries all currently face significant issues related to overcapacity, profitability, and growing international competition. The Chinese government's role in managing these challenges through policies and supply-side reforms will be critical in ensuring the success of these industries. As China continues to expand its global presence in the EV and solar sectors, it is poised to remain a dominant player in the global market for green technologies. However, the country must navigate complex trade dynamics and competition from other global players to maintain its competitive edge. Western World governments do not want to be totally reliant on China for these technologies. Australia plays a significant role in China's ongoing industrial transition and its legacy industries given its endowment of both critical minerals and iron ore. Tyndall currently holds a modest overweight in the resources sector, exposing it to the short-term stabilisation of the property market and the China economy, as well as to the longer thematic that relates to global decarbonisation and China's industrial transition. Author: Brad Potter, Head of Australian Equities Funds operated by this manager: Tyndall Australian Share Concentrated Fund, Tyndall Australian Share Income Fund, Tyndall Australian Share Wholesale Fund |

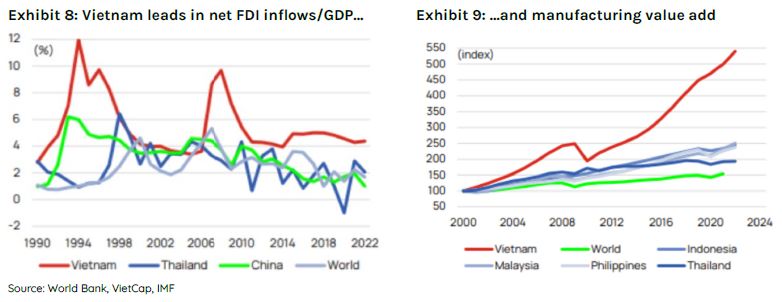

9 Oct 2024 - Trip Insights: LatAm (Part 1)

8 Oct 2024 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

||||||||||||||||||||||

| Dimensional Two-Year Sustainability Fixed Int. Trust AUD Class | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional World Allocation 70/30 Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

| Dimensional World Allocation 30/70 Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional World Allocation 50/50 Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Dimensional Sustainability World Allocation 70/30 Trust | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

||||||||||||||||||||||

| Magellan Core Global Fund | ||||||||||||||||||||||

|

||||||||||||||||||||||

| View Profile | ||||||||||||||||||||||

|

Want to see more funds? |

||||||||||||||||||||||

|

Subscribe for full access to these funds and over 850 others |

4 Oct 2024 - The Rate Debate - Ep51 The rest of the world is changing, so why aren't we?

|

The Rate Debate - Ep51 The rest of the world is changing, so why aren't we? Yarra Capital Management September 2024 The big question remains: will Australia follow the Fed's lead or stick to its current path? In Episode 51 of The Rate Debate, Co-Head of Fixed Income Darren Langer and Investment Manager Jessica Ren unpack the Fed's recent decision, explore the chances of rate cuts before Australia's next federal election, and debate the importance and reliability of employment data for the RBA. They also take a closer look at inflation pressures, from petrol prices and energy rebates to rising service costs. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

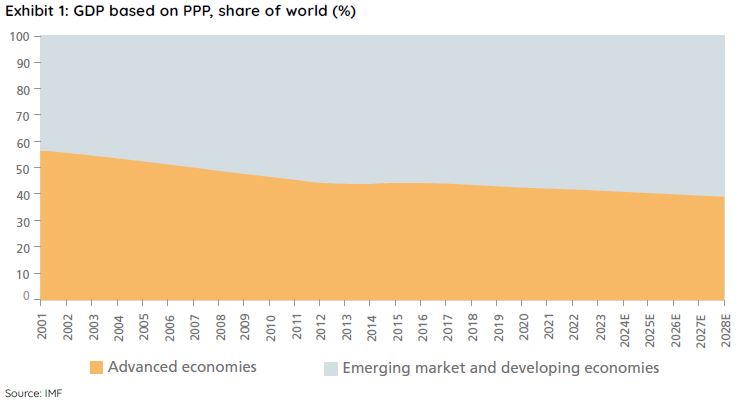

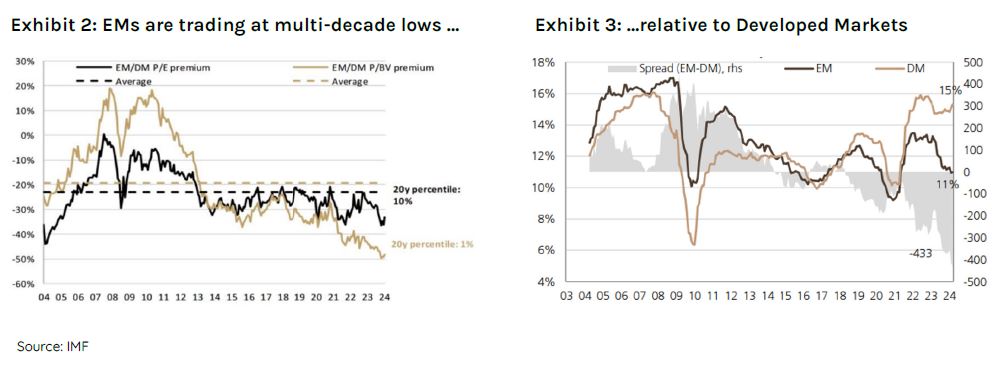

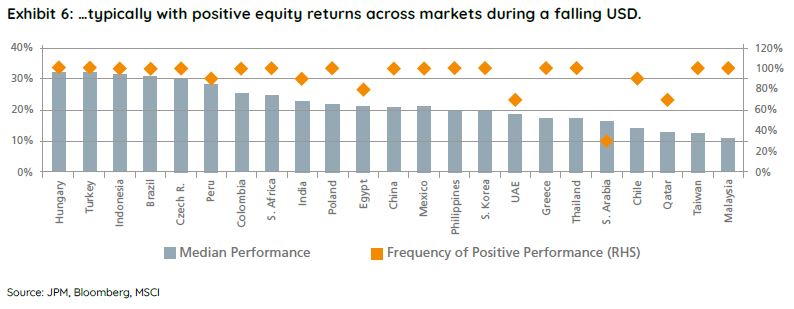

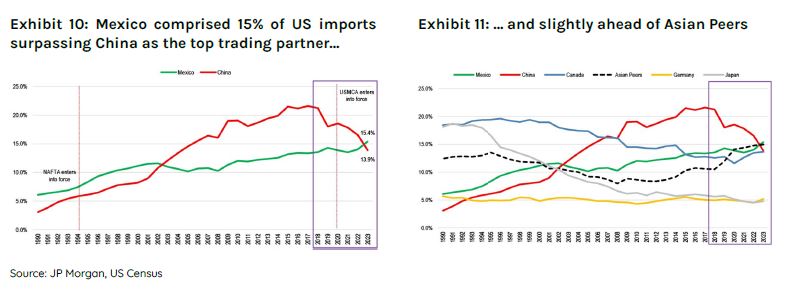

3 Oct 2024 - Emerging Markets are offering one of the biggest opportunities in a lifetime

|

Emerging Markets are offering one of the biggest opportunities in a lifetime Ox Capital (Fidante Partners) September 2024 The term "BRICS" was coined in 2001, and it refers to a collection of developing countries - Brazil, Russia, India, China and South Africa. Since then, the BRICS nations' share of global GDP (based on purchasing power parity) has surpassed that of developed economies, contributing to over ~60% of global GDP. China for example, grew its share of world GDP (PPP) to ~19% from ~8% in 2001. While China's growth is more mature, many other emerging economies are poised to continue the economic catch-up, as these economies still have relatively low-income per capita levels, and growth is driven by sound economic policies.  Notably, emerging markets equities are at a multi-decade low in price to earnings and price to book valuations compared to that of developed markets. It is an important fact given EM equities have historically outperformed developed market over the long-term. A general lack of interest has led to extraordinarily appealing valuations. We are looking at an attractive entry point with forward price to earnings multiples at depressed levels for quality companies with sustainable long-term growth and a backdrop supportive of outperformance. Moreover, many EM economies are undergoing continued economic development and political reforms. The economic fundamentals are much better than in prior years. Inflation is trending lower in many EMs allowing central banks to cut rates. A slowing developed markets economy is set to benefit emerging economies as we believe a slowdown in growth for the US will lead to interest rate cuts. Additionally, a declining US dollar and official interest rates are set to benefit emerging market equities.  The recent period of underperformance for emerging markets, is an outlier in our view. EM economies were much more indebted and starting valuations were high over a decade ago. The present outlook is vastly different. Fiscal balances are healthy while debt to GDP ratios are at stable levels. Corporates are in a healthy position. Moreover, many EM regions are rich in key commodities for the upcoming Net Zero energy transition. We remain optimistic on emerging markets and believe the fundamentals are in place for EMs to outperform developed economies. Our proprietary quant model (the MOAT) is pointing to a very difficult environment for many developed markets into 2H2024 into 2025 including the US, versus an improving outlook for many EM countries, including China. Ox Capital is positioned now to benefit by investing in quality companies with sustained growth at attractive valuations across EM countries. In a volatile environment such as the one we are in; it is important to try to hedge the volatility. Ox has the capability to manage the portfolio dynamically that has reduced volatility in the past. Theme 1: A weaker USDThe US interest rate hikes by the central bank (Federal Reserve) has driven a stronger US Dollar. The recent strength of the "greenback" has been a headwind for emerging economies. This is logical as a stronger dollar can impact capital flows, trade, direct investment, and can impact credit growth. We believe the eventual decline in the USD will provide a tailwind for emerging market equities as returns are typically higher when the USD is declining in value. Historically, EMs outperformed the market by ~20% on average over the period since 2003.   Theme 2: Rate CutsThe US federal funds rate has peaked and the FOMC is likely to cut rates as inflation moderates within its targets range. EM markets have historically performed well when the US cuts interest rate. Moreover, local central banks have been fiscally responsible. Many central banks have already started to cut official interest rates as inflation has trended back towards many central bank targets. Rate policy looks too restrictive, and cuts are likely to continue.  Theme 3: Supply chain reconfiguration and nearshoring.A reconfiguration of global supply chains will boost economic growth for a number of economies, especially nearshoring in ASEAN and LATAM, boosting GDP growth through foreign direct investments. Vietnam is a notable beneficiary of this trend. Greater foreign direct investment into an ever more open and market driven economy, with some of the most comprehensive free trade agreements in place globally, is providing strong employment opportunities for this young and vibrant country. As such, we believe this backdrop provides a foundation for alpha generating opportunities.  Moreover, nearshoring is a significant opportunity for the LATAM region in the coming years based on their geographical proximity to North America, and relatively cheap skilled labour. Nearshoring could add US$78 billion per annum in additional export revenue in LATAM in the coming years with Mexico being the primary beneficiary. Trade is especially important for Mexico. Mexico relies heavily on its industrial sectors for exports, with the manufacturing sector representing >80% total exports. Mexico's manufacturing sector has grown and matured over the years. Most recently, the top three export categories include auto-components, electronics, and machineries. Mexico is well placed with its long-established export capabilities to fulfil manufacturing orders for an increasing number of international companies. Mexico's relationship with the US is already well-established, as it is the largest exporter to the US. The country's ~15% share of US imports has now surpassed China's ~14%.  Growth in developed economies is expected to slow as rates have likely peaked. In contrast, despite recent economic challenges, the Chinese economy is expected to grow faster than the US, Japan, and Euro Area. Although China's growth is lower than in recent years, its economy is showing signs of bottoming, on the back of the Chinese authorities showing a willingness to stimulate and support the economy. Keep in mind that interest rates in China are low with minimal inflation relative to the rest of the developed world. A positive set up for equities in the year ahead. Moreover, Emerging countries make up the bulk of global growth, contributing to over ~60% of global GDP, but is under appreciated by global investors. Funds operated by this manager: Ox Capital Dynamic Emerging Markets Fund Important Information: This material has been prepared by Ox Capital Management Pty Ltd (Ox Cap) (ABN 60 648 887 914) Ox Cap is the holder of an Australian financial services license AFSL 533828 and is regulated under the laws of Australia. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriaten |

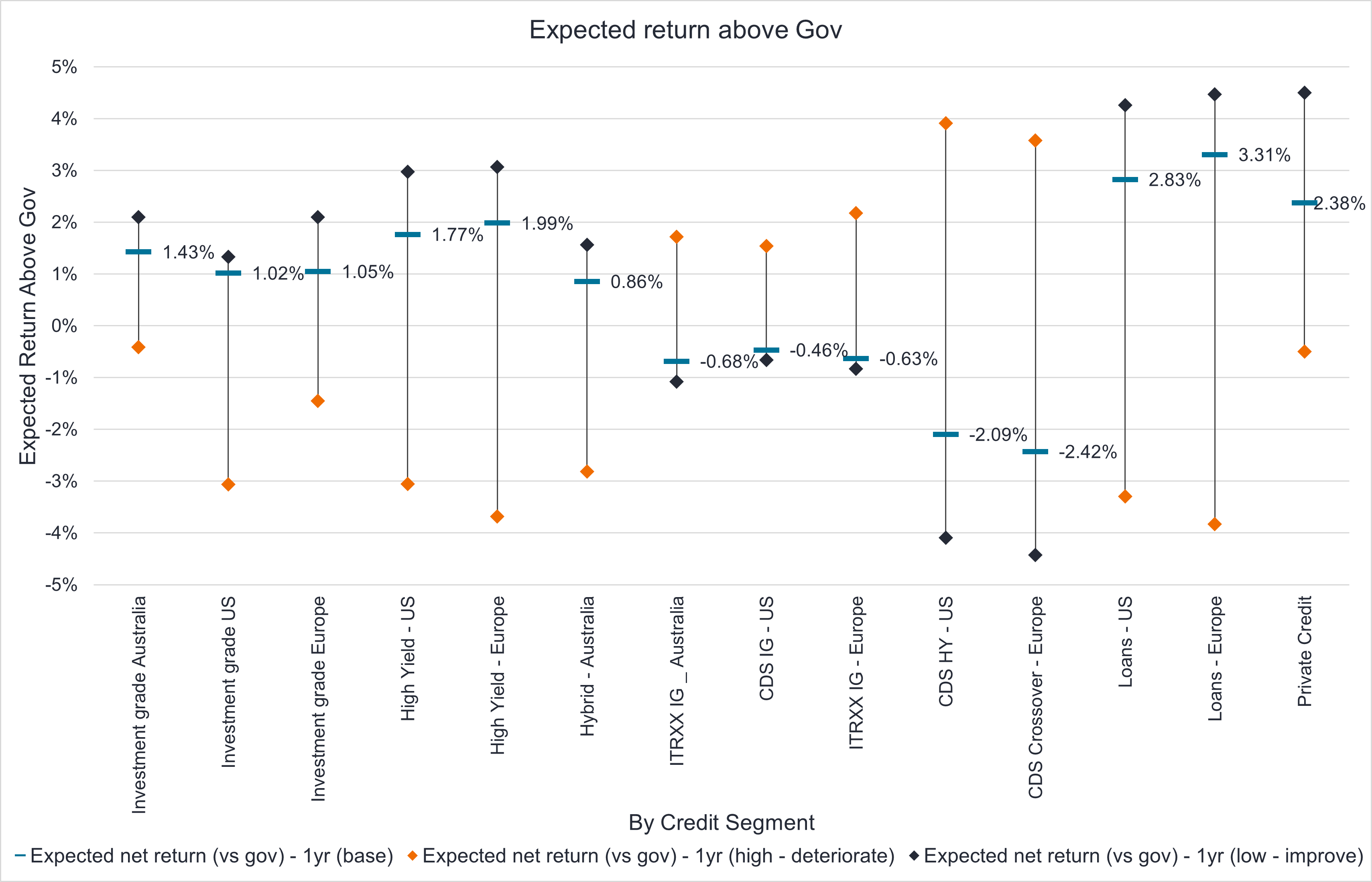

2 Oct 2024 - Why the coming downturn is good for credit investors

|

Why the coming downturn is good for credit investors Janus Henderson Investors September 2024 Jay Sivapalan, Head of Australian Fixed Interest, discusses the current state of credit markets and explores how active management strategies, mixed with nuanced credit investing, can lead to positive returns for investors. As monetary policy works its way through various economies reducing final demand it has, by design, the dual outcomes of softening labour markets and lowering corporate profitability. The world has changed, and the price of money, in our view, is now at much healthier levels whilst the availability of credit becomes more discerning. Funding costs for corporates have normalised, not just from the abnormally easy conditions during the pandemic, but also versus the decade of cheap money between the Global Financial Crisis and the pandemic. For investors, the late stage of this economic cycle has arrived and this brings the normal advent of rising delinquencies, re-structures and defaults. Whilst ordinarily this phase of the cycle would spell caution for investors, we believe ultimately it is a healthy development and that taking a nuanced approach to credit investing will likely deliver investors strong risk adjusted returns over the period ahead. Key considerations for investors include:

Starting point mattersAs the economic and business cycle nears the latter stages, any slowdown in economic growth, softening of labour markets will inevitably impact corporate earnings adversely. This cycle will be no different. However, the starting point is worth assessing for different segments of the corporate debt market. To provide some context, corporates in Australia and abroad were healthy, making adequate profits prior to the pandemic. During the pandemic, these very companies shifted upward to making abnormally high profits, aided by both monetary and fiscal policy as well as a resumption of demand. Inflation on nominal revenues also assisted the larger, stronger companies in gaining market share and achieving margin expansion. Meanwhile, highly-levered consumer cyclical and small-medium enterprise (SME) segment survived and in some cases temporarily thrived during the pandemic. However, this segment was never fundamentally strong nor sustainable and is now facing the reality of falling demand and higher funding costs. A different cycleFor the most part investment grade companies today remain well funded with debt termed out and highly profitable. From a fundamentals perspective, they remain relatively resilient to an economic growth slowdown. We see profits as moderating rather than falling precipitously. The same cannot necessarily be said for the SME segment. Nor for highly leveraged and/or cyclical, consumer centric businesses. A default cycle has commenced in loans, and pockets of high yield and private credit across the globe. Domestically this was most visible in SME delinquencies. It was initially centred around the property construction sector, but is now widening to hospitality, domestic tourism, recreational goods and services, and other consumer segments. Business models reliant on ongoing cheap debt or easy re-financing with little or no revenue is in the grips of a reality check, likely with harsh ramifications. A nuanced approach to credit investingNot all default cycles end in a crisis for credit markets. This cycle would suggest that defaults in investment grade companies should remain quite low by historical standards, but may be elevated in higher yielding segments. Importantly, rather than a uniform spike of defaults, we are more likely to see a rotation of defaults from industry to industry within lower quality credit. This will, in turn, keep the default rate rolling over multiple years. Recovery rates in these lower quality segments are being realised at lower levels than the past. Of course, market dislocations can occur with concerns around defaults lower down in credit markets, and cause mark to market underperformance in higher quality credit segments. We would assess these events as opportunities to add to investment grade credit without fear, rather than one to be cautious about. Outsized credit returns availableOverall, higher quality credit in the investment grade space remains the sweet spot for delivering healthy yields. However, to assess relative value, the sticker yields of lower credit quality, higher yielding segments need to be adjusted down for defaults and loss. The relative value of higher beta segments of the credit market currently remains less compelling in our assessment but a widening of credit spreads in this area would be valuable entry points for investors.

With the exception of a left field event, the most probable scenario points to strong prospective relative performance of credit, with investment grade credit being the sweet spot for investors on a risk adjusted basis. For the brave, the loans segment is potentially shaping up to be an opportunity, albeit security selection will be critical given the expected higher defaults and lower recoveries. A beta exposure is not recommended. Cheap ways to invest in credit and hedge tail risksTail ends of economic and market cycles have always been volatile, with investors seeking duration, quality risk-free assets and high compensation for default risk. Liquidity can also become fleeting in an environment of uncertainly. In order to preserve capital and also extract good returns in this environment, one must not passively sit on the sidelines; this is the wrong part of the cycle to be beholden to benchmarks. To ensure portfolios retain their defensive attributes, levers such as active management of duration, yield curve positioning and credit protection through the Credit Default Swap (CDS) market can be invaluable. We are confident dislocations will occur and opportunities will emerge. Again, actively utilising the full spectrum of inflation linked bonds, bond/swap and bond/semi-government spreads, corporate and asset backed betas (such as global loans, high yield and emerging market debt) can further drive return outcomes. Individual industry positioning will become important if markets dislocate more meaningfully. Today, both CDS protection and duration are cheap and effective tools that can be relied upon whilst fully utilising the prospective value in investment grade credit. We assess this as a great way for investors to enhance overall portfolio outcomes on a risk adjusted basis. Author: Jay Sivapalan, CFA |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund, Janus Henderson Australian Fixed Interest Fund - Institutional, Janus Henderson Cash Fund - Institutional, Janus Henderson Conservative Fixed Interest Fund, Janus Henderson Conservative Fixed Interest Fund - Institutional, Janus Henderson Diversified Credit Fund, Janus Henderson Global Equity Income Fund, Janus Henderson Global Multi-Strategy Fund, Janus Henderson Global Natural Resources Fund, Janus Henderson Tactical Income Fund This information is issued by Janus Henderson Investors (Australia) Institutional Funds Management Limited (AFSL 444266, ABN 16 165 119 531). The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson Investors (Australia) Institutional Funds Management Limited believe that the information is correct at the date of this document, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson Investors (Australia) Institutional Funds Management Limited to any end users for any action taken on the basis of this information. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson Investors (Australia) Institutional Funds Management Limited is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. |