NEWS

5 Feb 2025 - Responsible AI use in corporates with Jessica Cairns

|

Responsible AI use in corporates with Jessica Cairns Alphinity Investment Management January 2025 |

|

Jessica Cairns joins the Greener Way Podcast with Rose Mary Petrass to discuss the RAI Framework. With the rapid adoption of artificial intelligence, companies are facing growing pressure to ensure their AI practices are ethical, transparent, and aligned with environmental, social, and governance (ESG) principles. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Global Sustainable Equity Fund, Alphinity Sustainable Share Fund This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

4 Feb 2025 - Australian Secure Capital Fund - Market Update

|

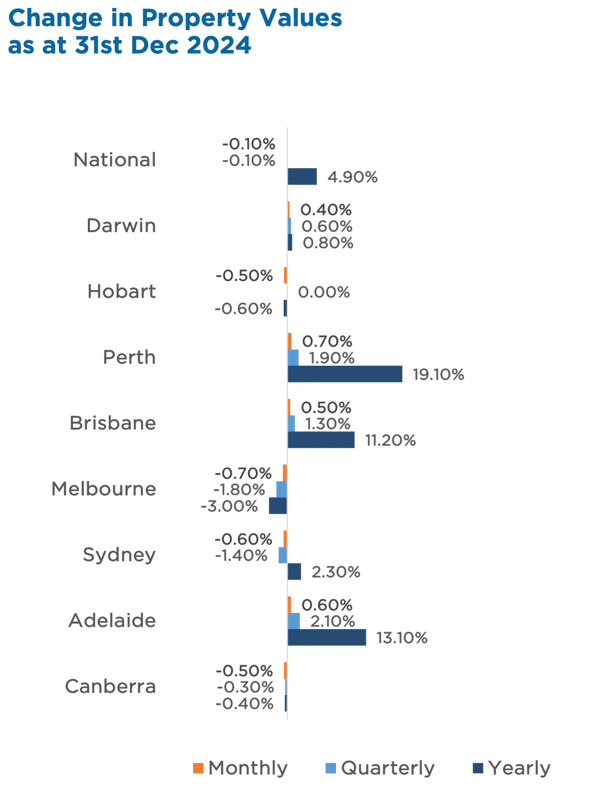

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund January 2025 CoreLogic's Home Value Index (HVI) recorded a 0.1% decline in December, the first national drop in nearly two years. This slight downturn capped a robust growth period from February 2023 to October 2024, where property values showed remarkable resilience despite high interest rates, cost of living pressures, and reduced borrowing capacity. The national decline was mirrored in the quarterly figures, with values also falling 0.1%, signalling a shift in momentum. Five of the eight capitals recorded declines between July and December, although Adelaide and Perth continued to perform strongly. Adelaide overtook Perth as the best-performing market in the December quarter, with values rising 2.1% compared to Perth's 1.9% and Brisbane's 1.3%. In annual terms, Australian home values rose 4.9% in 2024, adding approximately $38,000 to the median home value. The mid-sized capitals led the charge, with Perth (+19.1%), Adelaide (+13.1%), and Brisbane (+11.2%) achieving double-digit growth. However, Melbourne, Hobart, and the ACT recorded declines over the year, with values falling -3.0%, -0.6%, and -0.4%, respectively. Looking ahead, as highlighted in our market update above, anticipated rate cuts in 2025 should help stabilise the market, while a weaker Australian dollar may attract international investment, particularly in property. Regional markets, which outperformed the capitals with a 6.0% annual growth, are expected to remain a bright spot, driven by strong performances in WA, SA, and QLD. Property Values as at 31st of December 2024 |

3 Feb 2025 - Trump's TikTok Intervention

|

Trump's TikTok Intervention Magellan Asset Management January 2025 |

|

TikTok, one of the largest social media platform in the US along with Meta's Facebook and Instagram, has faced ongoing uncertainty regarding its existence in the US due to national security concerns under Chinese ownership. President Trump intervened in the Supreme Court's decision to ban TikTok in the US. Investment Director, Elisa Di Marco chats with Investment Analyst, Claire Britton reflecting on the implications of this intervention, the potential sale of TikTok, and its impact on the social media landscape, particularly for Meta. They discuss how Meta stands to benefit from the increased likelihood of a sale and the potential shifts potential shifts in user engagement and market dynamics.

|

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Core Infrastructure Fund, Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged) Important Information: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

31 Jan 2025 - Future Quality Insights: Pandemic Memories

|

Future Quality Insights: Pandemic Memories Yarra Capital Management December 2024 From pandemic pups to investment peaks Like many other households during the global COVID pandemic, we welcomed a new resident into our home: a small furry pooch named Benji. As our eldest son was leaving the family nest, getting a dog was a shameless act of replacement. It is not that our son Jamie used to follow us around the house and beg for food (at least not all the time) but the sense of quiet at home when he moved away to university became even more acute during the pandemic lockdown. Like many, we found solace in the comfort, loyalty and affection that dog owners will understand only too well. For those of you wondering what relevance this has in an investment article, it might be worth noting that Benji is now approaching the ripe old age of four. Although still a puppy at heart, he is moving through his adolescent phase and entering the human equivalent of his 20s. He is in his prime, but not for much longer. In the next couple of years, the millions of pets around the world adopted during lockdown will start to reach middle age. As humans of a certain age know only too well, this is when medical bills begin to rise. In short, we believe that there is a coming boom in pet healthcare never seen before (if only my son had studied something practical like veterinary medicine). In our view, this boom will not only benefit veterinarians but also present opportunities for companies in the animal pharmaceutical industry -- a sector where we have been doing some additional research recently. As an investment team, this link between the pandemic and pet healthcare got us thinking about other industries that were impacted by COVID-related demand cycles. We were prompted to consider how this might be currently unfolding and whether it is creating opportunities for long-term investment. The first thing that struck us during our reflections was the apparent existence of a COVID-related cycle in human memory, which seems to hamper our attempts to remember certain parts of the past. This could be the continuation of an existing trend, although we could not quite remember. Have we been systematically outsourcing our memory to Google for the last 20 years? In my case, almost definitely. Are we about to outsource our imagination to AI? Very possibly. Psychologists attest that we remember events to which we attach emotions, like the pain of a stock investment that went wrong. So why is it so difficult to remember the details of the pandemic? Almost two years of our lives were turned upside down, yet we struggle to recall precisely what happened and when. According to one theory, we were overloaded with emotion during the pandemic as we grappled with stressful daily updates about death rates, lockdown rules and restrictions on liberty. Faced with such a daunting picture, the theory goes that it is much easier for us to simply forget. With the aid of Google and a bit of Chat GPT, it is possible to piece this tricky bit of history back together and remember the industries that were impacted the most. So here it is--the painful (though not exhaustive) top 10 or so activities we did or saw during lockdown. For those with a nervous disposition who still wish to forget, feel free to look away now...cue the music please Benji. Let us start with the things we saw more of...

Then the things we did less of...

While the examples above may seem somewhat light-hearted and anecdotal, the consequences of these demand cycles are still being felt in many cases. Take, for example, Mark Schneider, the outgoing CEO of Nestle, or Laxman Narasimhan, the recently ousted CEO of Starbucks. Both were leaders of multinational consumer brands who struggled to adapt to the post-COVID world of volatile inflation and shifting consumer preferences. In fact, the list of consumer-facing businesses struggling with these issues is extensive. Companies like Diageo, Remy Cointreau, LVMH, L'Oreal, Estee Lauder, Burberry, Kerry Group and Kering, to name a few, have all suffered sharp share price reversals after the pandemic. The virtuous cycle turned vicious, and while these companies will likely recover, the dismissal of otherwise talented executives with successful track records shows the difficulty of distinguishing between cyclical trends and structural changes. We are likely witnessing these consumer-facing industries going through a classic long-tailed inventory cycle. Investors, including ourselves in the case of Diageo, became overly optimistic about the trajectory of demand for luxury goods, cosmetics and spirits in the reopening phase of the pandemic. Investors appear to have mistaken a stimulus-fuelled acceleration in demand, further boosted by inventory restocking, as a structural shift rather than a cyclical one. Currently, it is possible that the reverse is starting to occur. As tighter monetary policy hurt consumption, an inventory destocking phase began. Weaker demand, inventory destocking and falling valuations could be creating a compelling long-term investment opportunity. However, we may need patience -- a virtue that is seemingly in short supply in this post-pandemic world. These consumer-facing companies will likely bounce back, just as those left in the wake of the 1990s tech bubble emerged as some of the leading stocks of the early 2000s. One industry that may be springing back to life is video gaming. After a pandemic-induced boom in gaming, growth rates naturally moderated in the aftermath. Sony, for example, saw their operating margin within its gaming division drop from over 10% to just 5%, causing its share price to stagnate while the rest of the Japanese equity market surged. However, demand is now recovering, as evidenced by Sony's most recent results, with the company posting a gaming operating margin approaching 14%. The gaming recovery has been further confirmed by positive earnings reports from Tencent's gaming division and sports-related software producer Electronic Arts. We should not forget that all cycles turn eventually. The medical device sector is another industry that experienced a COVID boom followed by a dramatic post-pandemic slowdown in the last few years. While we were busy consuming alcohol, buying luxury goods and playing video games during the pandemic, the pharmaceutical and biotech industries were spending record amounts on developing new drugs. This created an excess inventory in equipment used to discover and produce these new therapies. Companies like Danaher and Bio-techne have struggled to contend with high inventories in their key end markets and a moderation in demand. Fortunately, this trend appears to be turning a corner, with an observable acceleration in orders and shipments across the industry. This shift has been welcome news for the companies in which we are invested. Patience indeed seems to be a virtue. Finally, it would be an oversight not to mention politics, which was impacted the most by COVID. It is difficult to explain how a candidate who, while US President, suggested that COVID could be defeated by ingesting bleach, could subsequently be re-elected even after alleging that citizens were eating their neighbours' pets (I'll let you know when it's safe to come out from under the sofa Benji). Collective amnesia brought upon by COVID could have played a part; however, the shift in the US political landscape may have more to do with the impact inflation had on the real incomes of the lower-income households. Perhaps for the first time in recent history, the Republicans attracted majority support from less affluent voters, a sobering thought for Democrats reflecting on their last four years. The outlook for the post-election world remains uncertain. The impact of a truly "America first" policy could be far reaching. However, it appears that the tail risks of such a policy are inflationary rather than deflationary. As such, we feel more strongly than ever that investors should strive for a diversified global portfolio of quality companies that can thrive in an environment where the cost of capital may be higher than previously expected. Our collective experience of the pandemic reminds us that such an approach is a fairly good idea. |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

30 Jan 2025 - From Resilience to Risk: Australian Market Outlook for 2025

|

From Resilience to Risk: Australian Market Outlook for 2025 Sage Capital January 2025 |

|

As we reflect on the key developments of 2024 and look ahead to 2025, this article provides an in-depth analysis of the trends shaping both global and Australian equity markets. Key Takeaways

2024 in Review: Global Strength, Local Surprises, and Shifting Market DynamicsLooking back, 2024 was a strong year for the Australian equity market as it trended higher with a strong performance by US equities being a key driver. The subsidence of inflationary pressures allowed the US Federal Reserve (US Fed) to shift to an easing monetary policy bias, cutting the official cash rate three times by a total of 100 basis points. This helped boost sentiment and asset prices in general as the market took comfort that downside economic risk was controlled. The US presidential election and the eventual Trump victory saw a strong finish to the year for markets. Equities, the US dollar, gold and cryptocurrencies were all aggressively bid as investor sentiment shifted into euphoric territory. The Australian market was a little more subdued as resources were generally under pressure across the year with sluggish Chinese growth and a lack of material stimulus. The most notable feature of the local market was the strong performance by the banks with CBA rerating to around a 25x Price Earnings ratio and forming over 10% of the index, leaving even seasoned investors, including us, puzzled. This breakdown in market efficiency appears linked to the increasing dominance of passive indexation and the growth of superannuation funds, that have divergent goals to maximising returns. Navigating 2025: Balancing Optimism with Emerging ChallengesAs we look forward to 2025, Sage Capital sees a generally positive outlook for Australian equities, though several risks are emerging. The primary risk is the potential impact of new US trade tariffs, which may drive domestic investment higher in the medium term but could disrupt short term growth and intensify inflationary pressures. Linked to this is the significant disconnect building between the bond market and the equity market. Bond yields have been pushing higher throughout the year as stronger US growth and more persistent core inflation have seen interest rate cut expectations pared back. There is also a supply-demand dynamic at play, with large budget deficits requiring funding, while the US Fed's quantitative tightening―by not repurchasing its considerable holdings of government bonds as they mature, adds further pressure. This process of quantitative tightening and interest rate cuts has seen the yield curve steepen but may act to constrain growth given that US mortgage interest rates are priced off the long end. Further increases in US bond yields may challenge markets, particularly across growth stocks which were largely immune from valuation impacts last year. We've seen similar dynamics at work in Australia where higher interest rates have largely been ignored by long duration growth stocks, across both healthcare and technology. Whilst this is the area of the market that is delivering the most consistent earnings growth with a combination of pricing power, low fixed costs and high margins, it's also the area of the market which has become the most crowded and valuations have been pushed beyond historical extremes in many cases. It's hard to ignore growth stocks when looking for high quality earnings compounders, but the risk of a sharp valuation correction is rising if these bond market dynamics continue. Our approach is to remain broadly neutral while identifying areas of relative valuation and earnings outperformance. Commodity prices have been generally soft, hampered recently by the strength in the US dollar, but broadly reflecting softer growth in China. It is difficult to be positive going forward on bulk commodities as China's population declines and an apparent lack of policy desire to stimulate the property and infrastructure sectors given the overbuilding that has already occurred. Our preference remains for base metals such as aluminium and copper where electrification demand is a key support for prices. Lithium remains oversupplied in the short term and western tariffs against Chinese EVs are unlikely to boost demand. However, the downside is also limited by cost curve support, so Sage Capital are relatively neutral and focused on stock selection. Energy has been unpopular as macro growth concerns and softening demand growth in China amongst a strong EV transition, although supply discipline by Organisation of the Petroleum Exporting Countries (OPEC) has helped provide price support. Energy stocks look cheap, and the space is heavily shorted so a contrarian move wouldn't surprise, particularly if the incoming US government drives stricter adherence to Russian and Iranian sanctions on oil exports. The Australian economy has remained reasonably strong, though higher interest rates have put pressure on heavily leveraged households. This has created a two-speed economy, split along demographic and generational lines, with older generations that have accumulated wealth benefiting from higher income flows, while younger generations, burdened by mortgage debt and higher rents, have faced greater financial strain. We expect this dynamic to persist in the short term, with a tight labour market and persistent services inflation likely keeping the RBA on hold until mid-2025. Even then, policy isn't that tight, and absent a growth shock, interest rates are unlikely to be significantly reduced. Sector Insights: Opportunities in Travel, Financials, and Diversified StrategiesSage Capital maintains a preference for travel stocks where older cohorts with wealth have an increasing preference to travel. While we don't foresee a material downturn in spending, weaker terms of trade with softer commodity prices, higher interest rates eroding savings buffers, and uncertainty surrounding the federal election are likely to keep consumer spending constrained. While performing well, some discretionary retailers, much like the banks, have re-rated to valuation levels that can't be justified by their growth outlooks. A solid, if unspectacular, growth outlook for the Australian economy and a strong labour market suggest that a bad debt cycle isn't imminent for the Australian banks. By the same token, banks have limited earnings growth potential as mortgage competition keeps net interest margins under pressure, book growth is limited given high household indebtedness, and rising costs are difficult to control amidst ongoing technology, security and regulatory demands. The valuation expansion doesn't appear justified by fundamentals, presenting more opportunities for shorting positions. Sage Capital's preference within the Yield group has for some time remained with insurers and diversified financials, and this is unchanged. These stocks all have ongoing earnings growth, even as the insurance premium cycle nears maturity. Valuations are closer to fair than cheap given the broad re-rating across the last year, but they are still clearly preferable than those in the banking sector. The portfolios are constructed using Sage Groups to minimise macro volatility with a focus on individual companies within these groups. Sage Capital maintains low net exposure to each Sage Group to limit the impact of unpredictable macro risks, and as always, the portfolios are well diversified and liquid. |

|

Funds operated by this manager: CC Sage Capital Equity Plus Fund, CC Sage Capital Absolute Return Fund |

29 Jan 2025 - Airlie Australian Share Fund Quarterly Update

|

Airlie Australian Share Fund Quarterly Update Airlie Funds Management December 2024 |

|

Emma Fisher discusses key drivers and insights from the recent quarter and how the portfolio was positioned to navigate the market. Emma also highlights the best performers for the fund and outlines opportunities the team continues to monitor as we move into 2025. Funds operated by this manager: Airlie Australian Share Fund, Airlie Small Companies Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

28 Jan 2025 - Global Matters: 2025 outlook

24 Jan 2025 - The Advantages Of Being A Small Investor

|

The Advantages Of Being A Small Investor Marcus Today January 2025 |

|

I have never liked the expression "Smart money". It is demeaning to individual investors and used by the finance industry to imply they are smart and the rest of you are by implication "Dumb". But a lot of supposedly smart professionals do some very dumb things, and a lot of non-professional investors (you guys) do some very clever things. What Big Investors Can Do That You Can't There are a few "Smart Money" activities available to institutional investors that most individual investors can't access. These include: Access to IPOs and Placements Big institutions often get priority access to IPOs, share issues, and placements. They get it because the brokers controlling the issue want to suck up to them to get their secondary market business. Inside Information There's an old broker's saying--"If you're not on the inside, you're on the outside." Many private investors assume that institutional investors have access to inside information and that the market is rigged against them. But this isn't the case. I once stood in a lift with a very experienced professional trader who overheard two brokers discussing an inside tip. In his gravelly voice of experience, he said, "If I'd never been told any inside information, ever, I'd be a million dollars better off." While inside information might exist, it's neither legal nor common, even among professionals. The misconception that everyone else has it is simply not true. That's not the game. Writing Options for Incremental Gains Wealthy investors sometimes write out-of-the-money call options against existing holdings. While this strategy can generate small, incremental returns, it doesn't provide substantial gains. It's also not practical for most individual investors. Why Being a Small Investor Is an Advantage Despite the perks available to big investors, small investors enjoy significant advantages that professionals can only envy. Liquidity Isn't an Issue Institutional investors often face liquidity problems, struggling to enter or exit positions without affecting share prices. Small investors can buy and sell quickly without influencing the market. Despite the perks available to big investors, small investors enjoy significant advantages that professionals can only envy. Freedom to Adapt Unlike fund managers who must follow strict mandates, small investors can shift strategies whenever they like. You're free to act without needing approvals or explanations. The Ability to Hold Cash Fund managers often can't hold cash even when markets drop. Small investors can exit the market and wait for better opportunities, avoiding unnecessary losses. No Need for Over-Diversification Fund managers must diversify to meet benchmarks, even if it means including underperforming stocks. Small investors can focus on a few high-quality opportunities instead. No Reporting Requirements Professionals deal with compliance regulations, financial services guides, and audits. Small investors avoid these headaches, saving time and money. Minimal Costs Running a self-managed portfolio means avoiding the overheads that come with managing large funds. There are no compliance fees, licensing costs, or administrative burdens. Instant Decisions Small investors can react to market events in real-time. Fund managers, on the other hand, face internal approvals that delay decisions. The Downsides of Being a Small Investor Of course, small investors do miss out on some perks available to institutional players: No Broker Perks Big investors enjoy access to IPOs, discounted placements, and premium research. Brokers often court them with lunches and events. Limited Research Support Institutions have teams of analysts hunting for investment opportunities. Individual investors typically rely on their own research. No Excuses for Losses While fund managers can justify losses by pointing to market-wide downturns, small investors face personal accountability for their results. Why Flexibility Beats Big Money Sure, big investors get the perks--lunches, research, and IPOs but they're also stuck in a system full of rules, reports, and restrictions. Small investors, on the other hand, have the freedom to move quickly, cut costs, and make decisions without answering to anyone. And let's be honest when it comes to investing, freedom is worth more than a free lunch. Author: Marcus Padley |

|

Funds operated by this manager: |

23 Jan 2025 - Trump nominated a vaccine sceptic for health secretary. What does that mean for investors?

|

Trump nominated a vaccine sceptic for health secretary. What does that mean for investors? Redwheel December 2024 |

|

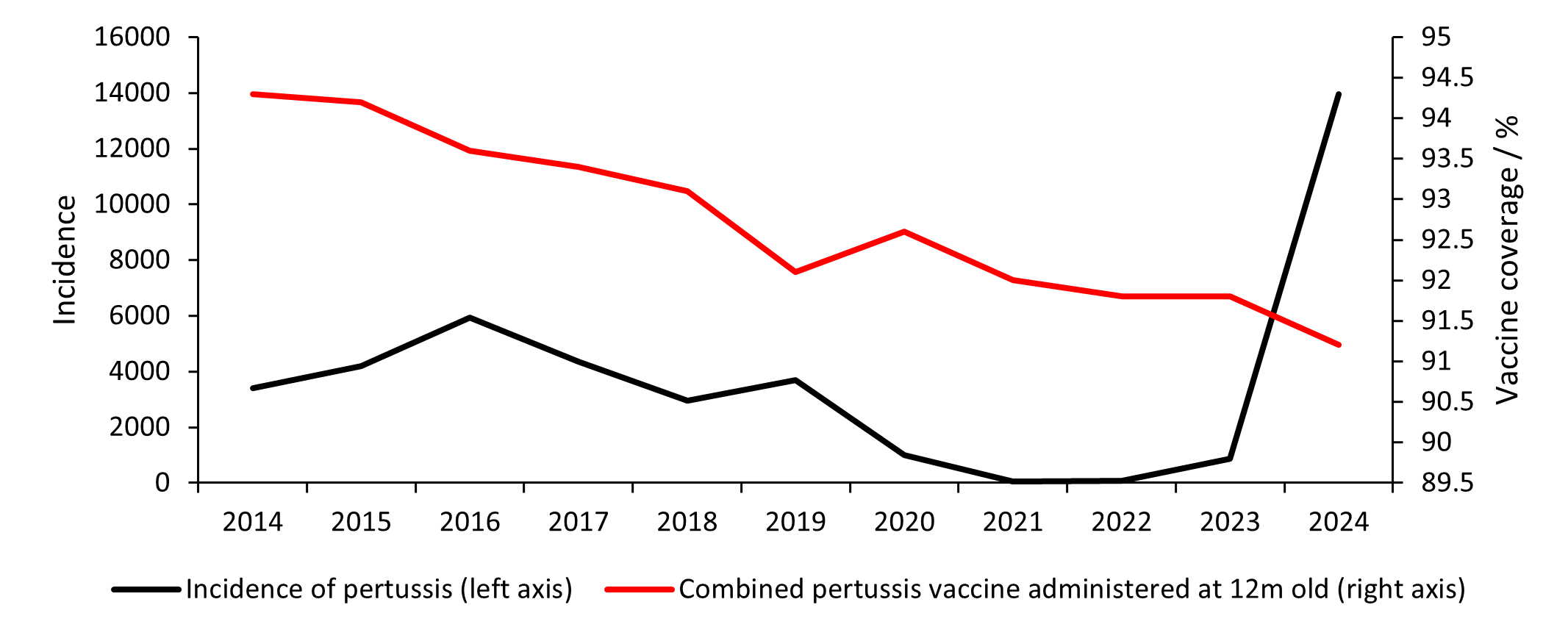

Vaccines are among the most impactful medical inventions in history.[i] Globally, vaccines exist to prevent more than 20 life-threatening diseases.[ii] New estimates suggest that global immunisation efforts over the past 50 years have prevented 154 million deaths from diseases like diphtheria, tetanus, pertussis, yellow fever, and measles.[iii] Despite worldwide immunisation success, the COVID-19 outbreak and resulting vaccination race brought into focus the global prevalence of vaccine hesitancy and appeared to trigger a further decline of trust in vaccinations.[iv] A US survey found that the proportion of surveyed adults who do not think approved vaccines are safe rose by 6% to 16% between 2021 and 2023.[v] Similarly, a survey in Germany shows that public vaccine scepticism increased from 21% in 2022 to 25% in 2024.[vi] As a result of decreasing vaccine uptake and concerns over the prevalence of preventable diseases, the World Health Organisation has declared vaccine hesitancy as one of the top global health challenges.[vii] Whooping cough (pertussis) in England shows the concerning effect of increasing vaccine scepticism, declining vaccination rates, and consequent rising incidence of the disease. Although historically associated with lower-income countries where there is greater mistrust of vaccines, Figure 1 demonstrates how growing scepticism can have a marked impact on disease prevalence in higher-income countries too[viii]. In 10 years, the infant pertussis vaccine coverage in England fell from 94% to 91%, meanwhile the maternal pertussis vaccine coverage fell from 75% to 59% from 2017 to 2024[ix]. Incidence of the disease has more than tripled over the same time-period.

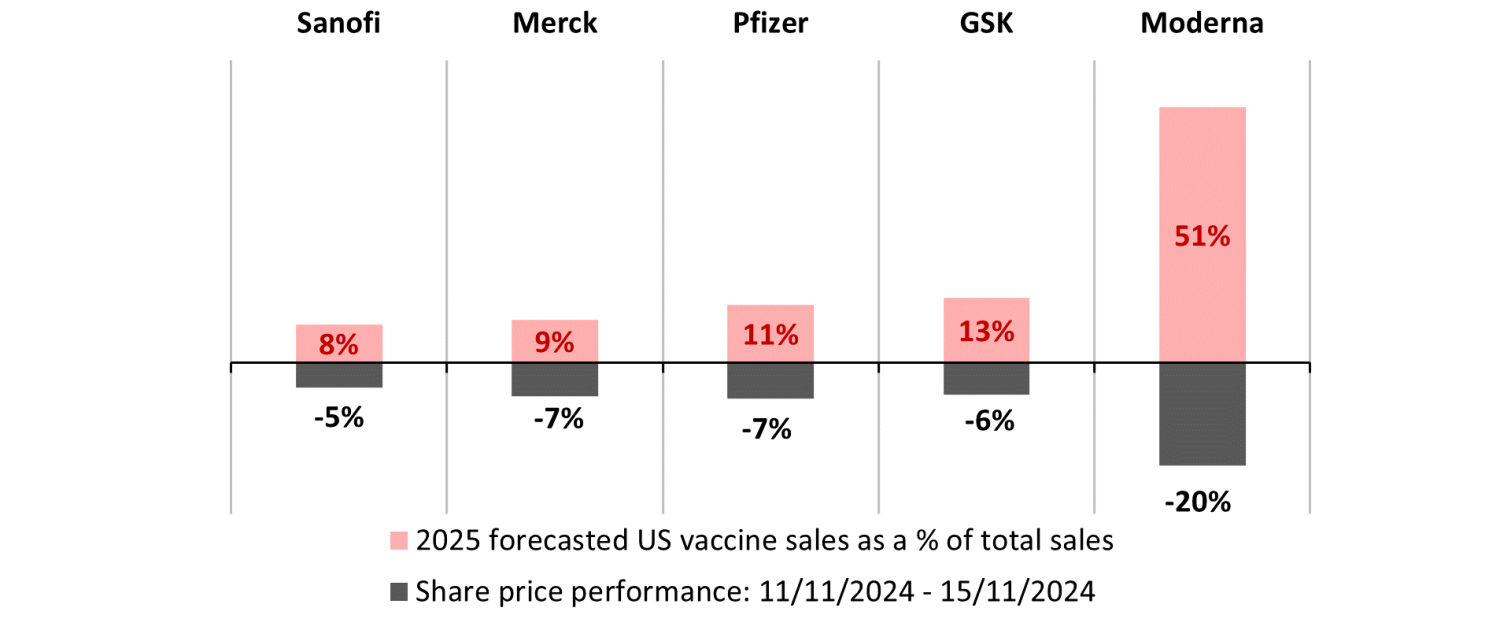

A similar trend can be detected with measles, where misguided concerns over a link with autism in children have led to declining vaccination rates[x]. 2023 saw a 20% rise in global cases compared to 2022[xi], while nearly 60 countries experienced outbreaks in the past year. Globally, only 83% of children received a first dose of the measles vaccine in 2023 and only 74% received the recommended second dose, despite national coverage of 95% or greater being necessary to prevent outbreaks of the contagious disease.[xii] During the COVID-19 pandemic it was found that antivaccine messages from authority figures were a common reason for vaccine hesitancy.[xiii] Now that President-elect Donald Trump has nominated Robert F Kennedy Jnr. (RFK Jnr.) - who has been skeptical of vaccines in the past - to head up the Health and Human Services Department, there are increasing concerns of an even greater erosion of people's willingness to get vaccinated in the US.[xiv] How does this impact investors? RFK Jnr.'s nomination as Head of Health and Human Services (HHS) precipitated a sharp sell-off in healthcare stocks. Sanofi, Merck, Pfizer, GSK, and Moderna have greater exposures to the US vaccine market and hence were punished most by the market in the week of his nomination.

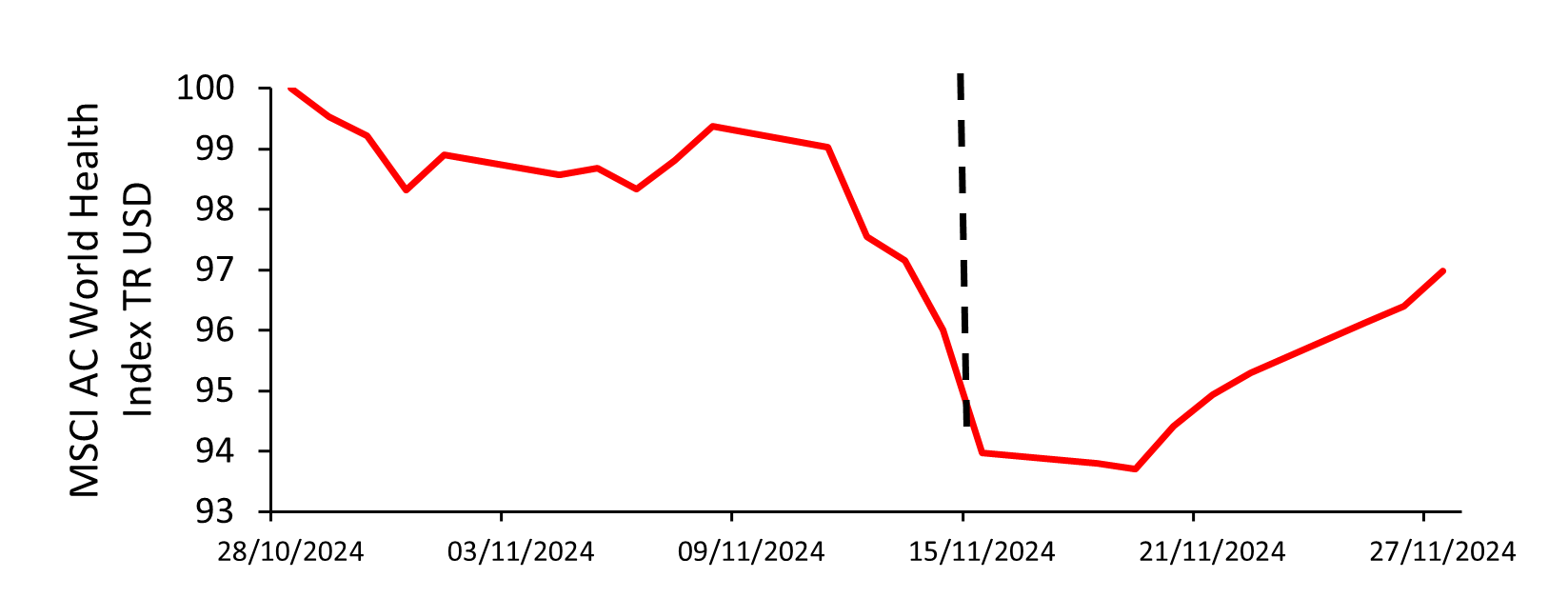

Although there is very little clarity over the shape of future US health policy, there is a presumption in the investment community that RFK Jnr.'s vaccine stance may lead to larger and longer clinical trials, stricter labels for approved products, lower vaccination rates, and therefore lower revenues for vaccine makers. Further, with Republican control of both chambers of Congress and the White House, a hawkish health department could seek to repeal the National Childhood Vaccine Injury Act of 1986 which protects vaccine makers from litigation due to injury. An increase in lawsuits - even if not successful - may increase costs for manufacturers. Ultimately, if significant legislative changes were to occur then investing in vaccine makers could be riskier. However, whilst commentators have focussed largely on RFK Jnr.'s more harmful rhetoric, not all news has been entirely negative. RFK Jnr. has stated that vaccines were 'not going to be taken away from anybody'[xv], while Vivek Ramaswamy - who will co-lead the newly created Department of Government Efficiency (DOGE) - confirmed that the new US healthcare leadership 'understand innovation is a key part of the solution.'[xvi] And it is interesting to note that Ramaswamy has made comments suggesting that he wants DOGE to reduce regulatory burden on pharma, biotech and medical device companies that require US Food and Drug Administration (FDA) approval. He recently posted on X, "My #1 issue with FDA is that it erects unnecessary barriers to innovation", so it could be argued that the FDA under the Trump administration may be supportive of getting treatments to patients more quickly, which would most likely be a net positive for manufacturers. Further, it is our view that despite potential disruption in US healthcare, many treatments will continue to have a life-changing impact on patients' lives, and hence, best-in-class businesses will keep their competitive advantage. In the week of RFK Jnr.'s nomination, the MSCI AC World Health Index declined by more than 5%[xvii], which included companies with no exposure to vaccines. With that discount, we believe there are significant opportunities for us to invest in these life-changing solutions at compelling valuations.

|

|

Funds operated by this manager: Redwheel China Equity Fund, Redwheel Global Emerging Markets Fund |

|

Sources: [i] UN, 2024 [ii] WHO, 2024 [iii] WHO, 2024 [iv] Larson et al., 2022 [v] Annenberg Public Policy Center, 2023 [vi] Statista, 2024 [vii] WHO, 2019 [viii] RACGP, 2024 [ix] GOV UK, 2024 [x] Hviid et al., 2019 [xi] Reuters, 2024 [xii] CDC, 2024 [xiii] Griffith et al., 2021 [xv] NPR interview, 06/11/2024. [xvi] Vivek Ramaswamy's push for FDA changes could boost his wealth - The Washington Post, accessed 27/11/2024. [xvii] Bloomberg, November 2024 Key Information |

22 Jan 2025 - Long-term Investing

|

Long-term Investing Airlie Funds Management December 2024 |

|

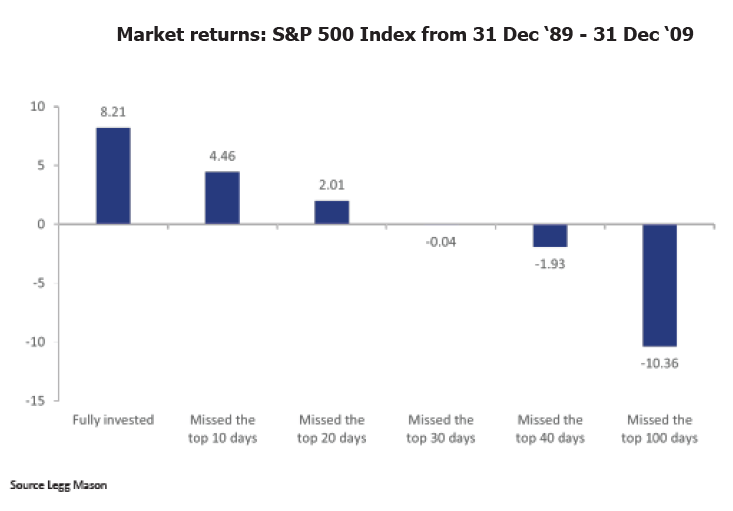

Investing in Australian listed companies with a long-term outlook entails retaining investments for a minimum of five years or longer. While the exact time frame for long-term investing can differ, the core principle is dedication, regardless of market turbulence and fluctuations in asset prices. We delve into key strategies tailored for those investors keen on harnessing the potential of Australian listed companies for long-term wealth accumulation. Objectives, risk tolerance and investment horizonLong-term investing begins with a clear understanding of your financial objectives, risk appetite, and investment time frame. Whether your aim is to secure your retirement, finance education expenses or a dream property, clearly defining your goals is essential. Assessing your risk tolerance, which means finding out if your risk level is conservative, moderate or aggressive, helps you understand the level of risk you're willing to accept in pursuit of your investment objectives. Generally, investors with longer horizons can afford to embrace higher risks compared to those nearing retirement. It's important to consider your investment time horizon, as this is when you'll need access to money to achieve your financial objectives. Some of the factors that influence your time horizon include your financial goals, income, age and risk tolerance. Tailoring your investment strategy to align with your unique circumstances is foundational for long-term success in the Australian market. Diversify your portfolioThe Australian investment landscape, like any other, is prone to unpredictability and market fluctuations. Spreading your investments across different industry sectors can potentially help to mitigate risk. Diversification may help reduce the potential negative impact of any single asset's downturn on your overall portfolio. This approach helps in balancing out the performance, as when one asset or sector underperforms, another may outperform, stabilising the portfolio's returns. It's important to align diversification with your individual risk tolerance and investment goals, ensuring a well-rounded and resilient investment strategy. Stay committedEmotions often run high during market downturns, tempting investors to deviate from their chosen investment strategies. However, succumbing to fear-driven decisions can jeopardise long-term returns. Resist the urge to time the market, as consistently predicting market movements is exceedingly challenging. Long-term investing requires discipline and resilience, where investors are encouraged to adhere to their investment strategies even amidst turbulent market conditions. Avoid falling into the trap of chasing short-term profits, as maintaining investment during market cycles can be essential for realising the full potential of the market. It's easy to feel drawn to timing the markets, aiming to choose tomorrow's winners from yesterday's winners. However, evidence suggests that market timing is a tough game. Take the buy low, sell high approach, for instance; it hinges on predicting when a stock will rise or fall, a task fraught with complexity. Successful long-term investing, on the other hand, demands a commitment to staying invested, resisting the urge to constantly chase the next big thing. The chart below illustrates the risks of trying to time the market.

Leverage expertise and regular reviewAchieving success in investing requires a thorough understanding of market dynamics and investment strategies. Consider investing in managed funds where investment experts are actively researching and managing a portfolio, aiming for optimal diversification with continued dedicated oversight. Review your investment strategy regularly to ensure it remains aligned with your long-term objectives. Rebalancing your portfolio and adjusting the weightings of your portfolio helps to ensure alignment with your intended long-term goals. Over time, some investments may perform better than others, causing your portfolio to shift from its original strategy. Rebalancing brings your portfolio back to its original plan, ensuring it continues to reflect your investment goals and risk tolerance. Long-term investing in Australian-listed companies entails a strategic approach tailored to your unique financial goals and risk tolerance. By embracing diversification, maintaining discipline, and leveraging expert guidance, investors may have greater confidence in navigating the dynamic Australian market landscape. Funds operated by this manager: Airlie Australian Share Fund, Airlie Small Companies Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |