NEWS

17 Dec 2024 - Proprietary Data - Strategic AI Advantage

|

Proprietary Data - Strategic AI Advantage Insync Fund Managers December 2024 Proprietary data sets provide businesses with competitive advantages due to their uniqueness, quality and relevance. They are often more specific, accurate, and tailored to a company's particular needs or industry, providing a rich data source for AI algorithms. RELX Plc is a global provider of information-based analytics and decision tools providing products that help researchers advance scientific knowledge across medical, legal, financial services, and government sectors. They recently showcased their Legal division's advancements highlighting cutting-edge AI-enabled tools like Lexis+ and its next-generation AI assistant, Protégé. This division underwent a remarkable transformation, shifting from print and basic electronic reference services to advanced analytics and decision-making platforms. Growth rates have accelerated by 14%, with the division now targeting an 8% growth rate by 2025.

RELX's competitive advantage lies in its extensive proprietary datasets, leading brands, and a robust installed user base. Analysts increasingly recognize RELX as an AI beneficiary.

By integrating RELX's vast 100+ billion document datasets with clients' internal knowledge, their AI assistant addresses legal professionals' top demands, enhancing productivity. This unlocks a 20% total addressable market (TAM) expansion. At Insync, we see RELX as a prime example of technology driving structural growth. The company's accelerating growth and discounted valuation relative to peers underscore our conviction, making RELX one of our key holdings. Funds operated by this manager: Insync Global Capital Aware Fund, Insync Global Quality Equity Fund Disclaimer |

16 Dec 2024 - Investment Perspectives: Why a Trump presidency could be deflationary

13 Dec 2024 - Risks & Issues in 2025 - Part 2

13 Dec 2024 - Trump trade 2.0 - Who is going to buy all this stuff?

|

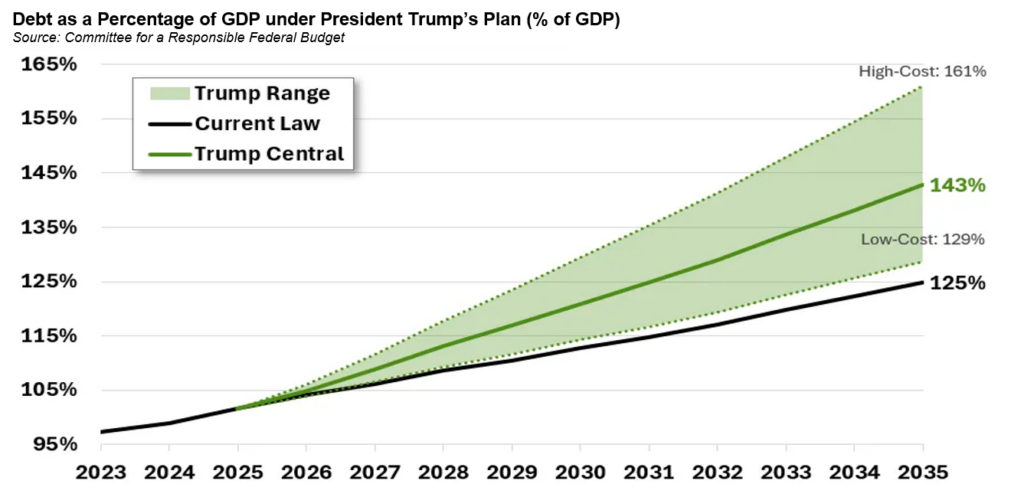

Trump trade 2.0 - Who is going to buy all this stuff? Challenger Investment Management November 2024 In 2016 the election of Donald Trump as president of the United States caused an initial panic in markets with S&P500 futures plunging over 5% as his shock win became more likely. Wall Street had favoured Clinton, fearing Trump's positions on trade. Markets settled down on the US open as investor fears of the most extreme policies abated. Fast forward to 2024 and Trump has returned with Republicans controlling the House and Senate on the back of a similar policy agenda centred around trade and immigration. This time however equities rallied prior to the election on expectation of a Trump win and post the election once his victory was confirmed. The key difference between 2016 and 2024 is the state of the US balance sheet. In 2016 the debt to GDP ratio was 105%, peaking at 132% in the second quarter of 2020 and stands at 120% today. The deficit in 2016 was 3% of GDP. In 2023 it was over 6% and according to Deutsche Bank, will average around 7% over the Trump presidency, higher than the 6% average projected by the Congressional Budget Office. Prior to the election the bipartisan Committee for a Responsible Federal Budget estimated that a Trump presidency would result in an 18% increase in the public debt to GDP ratio relative to the current trajectory (note the below chart shows the debt held by the public and excludes debt held by federal trust funds and other government accounts).

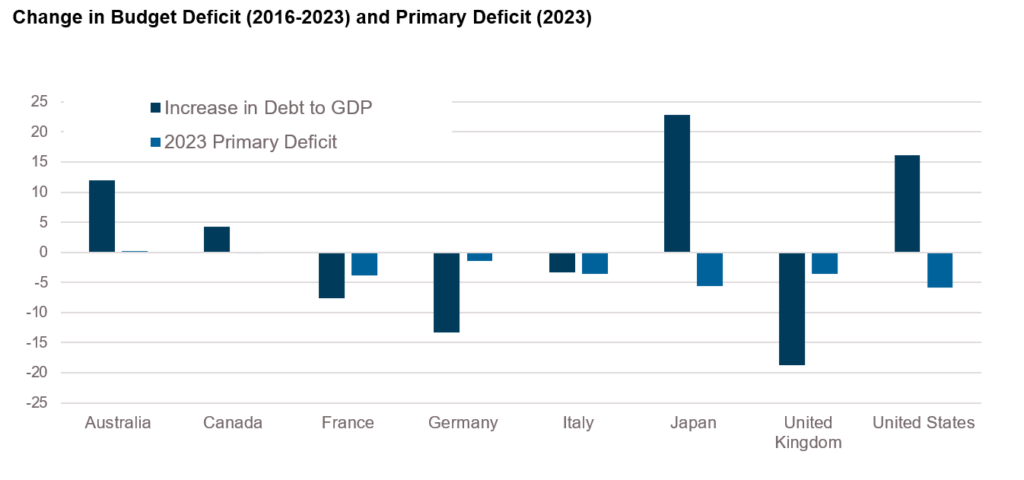

The problem for the United States is not so much the change in the deficit but that it is so much more than those observed by its peers. From 2016 to 2023, the debt to GDP in the United States increased by more than 15%, second most of the peer group above. Perhaps even more concerningly, the primary deficit in 2023 was the worst amongst these nations suggesting, if the above projections hold, the United States debt to GDP ratio will be the second highest amongst developed nations only trailing Japan.

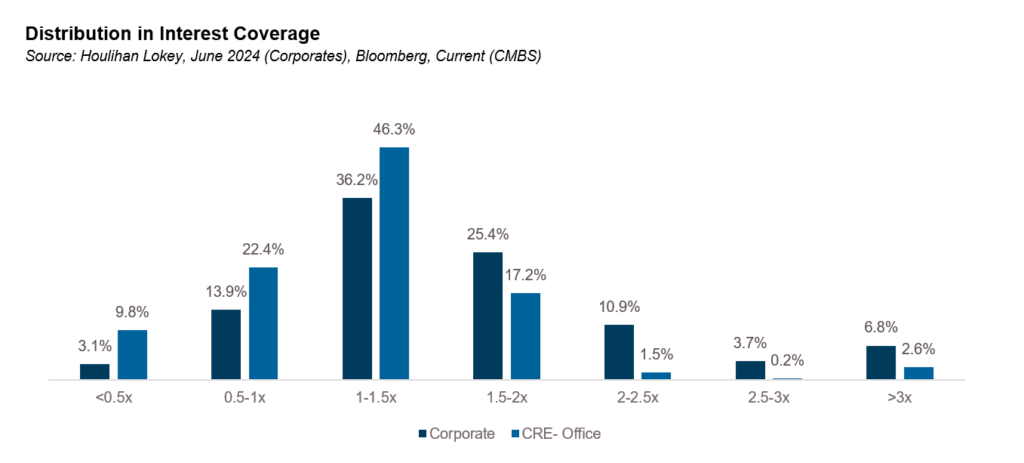

Adding to the supply story is the demand side of the equation. During periods of quantitative easing the Federal Reserve is a classic example of a price insensitive buyer. However, since mid-2022 they have been a price insensitive net seller (effectively, by not reinvesting principal repayments) with the balance sheet down by around US$0.75 trillion to US$7 trillion over the last 12 months. The Fed is currently allowing up to US$25 billion in Treasuries and up to US$35 billion in MBS to mature without reinvestment monthly which could result in another $0.7 trillion reduction over 2025 i.e. a quantitative tightening period. Contrast to 2016 when there was virtually no change to the Fed balance sheet. With the Federal Reserve out of the equation the marginal buyers over the past 12 months have been largely price sensitive buyers; money market funds (up US$1.2 trillion), private foreigners (up US$0.5 trillion) and households and nonprofits (up $0.35 trillion). Commercial banks, a price insensitive buyer has increased their holdings, up US$0.15 trillion in the 12 months to 30 June 2024. With supply increasing and the marginal buyer of treasuries transitioning from a price insensitive one to a price sensitive one the bias would seem to be for yields to move higher. Of course, the Federal Reserve remains the buyer of last resort but in all likelihood will only step in where absolutely necessary. Markets are now pricing the Fed Funds rate declining to around 3.75% by early 2026, a full 100 basis points higher than what was priced only two months ago. To be clear our view is not that Trump's election and the Republican sweep of the House and Senate will result in systemic issues within the treasury market in the United States. We're also not suggesting that treasuries now entail some level of credit risk given the increases in the debt to GDP ratio that we expect over the coming years. We would argue that tail risks have increased given the unpredictability of this administration compared to the more orthodox Biden administration which is a topic worthy of discussion (and something we'll get to in a future piece) but our central position is that a Trump presidency cements the higher for longer thesis. So, what does higher for longer mean for credit? For the most part, corporate credit has been resilient to higher interest rates and has weathered the hiking cycle well with higher earnings muting the impact of higher interest rates. For the S&P500, EBITDA has increased by 15% from the point at which interest rates started increasing. For middle market borrowers, the effect has been even more pronounced with earnings increasing by around 20% over the corresponding period. Interest coverage has stabilised at around 1.5 times with around 15% of borrowers with coverage of less than 1 times. This will improve as interest rates decline. The problem child for credit markets remains commercial real estate markets which is most acutely impacted by higher interest rates. A Bloomberg search of adjustable rate office loans contained in CMBS transactions shows that over three quarters currently have serviceability ratios of less than 1.5 times with one third below 1 time.

It's ironic given the Trump family made their name in commercial real estate that the sector we expect to be most impacted by his presidency is CRE but it is the one that is more leveraged to interest rates. And while wider equity markets have rallied strongly to the new administration, mortgage finance REITs are flat for the month. Author: Pete Robinson | Head of Investment Strategy - Fixed Income Funds operated by this manager: Challenger IM Credit Income Fund, Challenger IM Multi-Sector Private Lending Fund For Adviser & Investors Only Disclaimer: The information contained in this publication has been prepared solely for solely for the addressee. The information has been prepared on the basis that the Client is a wholesale client within the meaning of the Corporations Act 2001 (Cth), is general in nature and is not intended to constitute advice or a securities recommendation. It should be regarded as general information only rather than advice. Because of that, the Client should, before acting on any such information, consider its appropriateness, having regard to the Client's objectives, financial situation and needs. Any information provided or conclusions made in this report, whether express or implied, do not take into account the investment objectives, financial situation and particular needs of the Client. Past performance is not a guide to future performance. Neither Fidante Partners Limited ABN 94 002 895 592 AFSL 234 668 (Fidante Partners) nor any other person guarantees the repayment of capital or any particular rate of return of the Client portfolio. Except to the extent prohibited by statute, Fidante Partners or any director, officer, employee or agent of Fidante Partners, do not accept any liability (whether in negligence or otherwise) for any errors or omissions contained in this report. |

12 Dec 2024 - AI - Is the juice worth the squeeze?

|

AI - Is the juice worth the squeeze? Janus Henderson Investors November 2024 Power availability is the biggest challenge for AI growth. Portfolio Manager Hamish Chamberlayne discusses how innovation seeks to meet AI's energy needs but highlights unresolved issues regarding its energy sources and the technology's potential impact on climate.

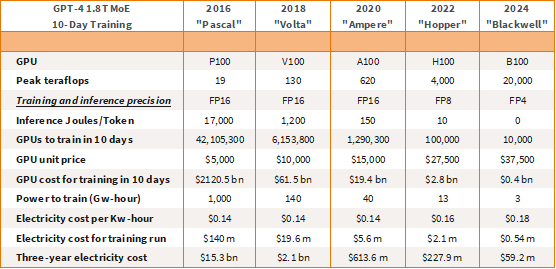

The power demands of artificial intelligence (AI), combined with the impacts of reindustrialisation, (EVs), and the transition to renewable energy, sees the technology represent a significant investment opportunity across the entire value chain, including data centre and grid infrastructure, as well as electrification end markets. However, it is important to always consider and question potential risks, particularly the physical limitations on AI's growth, where its insatiable thirst for energy will come from, and how its associated emissions may fuel new climate concerns. What is enabling AI?The advancement of AI is primarily enabled by US-based chipmaker Nvidia's increasingly efficient graphic processing units (GPUs). Figure 1 illustrates the evolution of its GPUs, showcasing the efficiency gains, depicted in terms of teraflops per GPU, per watt, across models from Pascal (2016) to its latest iteration Blackwell (2024). Currently, to train OpenAI's ChatGPT-4 in just ten days, one would need 10,000 Blackwell GPUs costing roughly US$400 million. In contrast, as little as six years ago, training such a large language model (LLM) would have required millions of the older type of GPUs to do the same job. In fact, it would have required over six million Volta GPUs at a cost of US$61.5 billion - making it prohibitively expensive. This differential underscores not only the substantial cost associated with Blackwell's predecessors but also the enormous energy requirements for training LLMs like ChatGPT-4. Figure 1: The cost curve

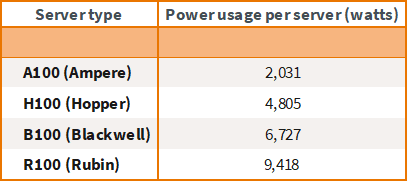

Source: NVIDIA, nextplatform, epochai.org Previously, the energy cost alone for training such an LLM could reach as much as US$140 million, rendering the process economically unviable. The significant leap in the computing efficiency of these chips, particularly in terms of power efficiency, however; has now made it economically feasible to train LLMs. This point is illustrated in Figure 1 under the metric 'inference joules/token', which is used to measure the energy efficiency of processing natural language tasks, particularly in the context of LLMs like those used for generating or understanding text (e.g., chatbots, translation systems). Here we can see a 25x improvement in efficiency from Nvidia's Hopper (10) to its Blackwell (0.4) successor. The sting in the tailNvidia's innovations in the power efficiency of its chips have indeed enabled advancements in AI. However, there is a significant caveat to consider. Although we often assess the cost-effectiveness of these chips in terms of computing power per unit of energy - Floating Point Operations Per Second (FLOPS) per watt - it's important to note that the newer chips come with a higher power rating (Figure 2). This means that, in absolute terms, these new chips consume more power than their predecessors. Figure 2: Nvidia GPU power ratings

Source: Morgan Stanley research Note: Power usage per server (assuming four chips per server). Couple this with Nvidia's strong sales growth, indicating an incredible demand for computing power from companies like Alphabet (Google), OpenAI, Microsoft and Meta, driven by the ever-increasing size of datasets to develop AI technologies, the power implications of AI's rapid expansion have begun to raise eyebrows. Interestingly, thanks to efficiency improvements, global data centre power consumption has remained relatively constant over the past decade, despite a massive twelvefold increase in internet traffic and an eightfold rise in datacentre workloads.1 An International Energy Agency (IEA) report highlighted how data centres consumed an estimated 460 terawatt-hours (TWh) in 2022, representing roughly 2% of global energy demand,2 which was largely the same level as it was in 2010. But, with the advent of AI and its thirst for energy, data centre energy consumption is set to surge. In fact, the IEA estimates that data centres' total electricity consumption could more than double to reach over 1,000 TWh in 2026 - roughly equivalent to the electricity consumption of Japan.3 This highlights how demand for AI is creating a paradigm shift in power demand growth. Since the Global Financial Crisis (GFC), demand for electricity in the US has witnessed a flat 1% bump annually - until recently.4 Driven by AI, increasing manufacturing/industrial production and broader electrification trends, US electricity demand is expected to grow 2.4% annually.5 Further, based on analysis of available disclosures from technology companies, public data centre providers and utilities, and data from the Environmental Investigation Agency, Barclays Research estimates that data centres account for 3.5% of US electricity consumption today, and data centre electricity use could be above 5.5% in 2027 and more than 9% by 2030.6 The innovation, efficiency, and sustainability paradoxThis paradigm shift introduces the concept of the Jevons Paradox, which has implications for energy consumption and environmental sustainability. It suggests that simply improving the efficiency of resource use is not enough to reduce total resource consumption. The paradox is named after William Stanley Jevons, an English economist who first noted this phenomenon in the 19th century during the Industrial Revolution. In his 1865 book "The Coal Question," Jevons observed that technological improvements in steam engines made them more efficient in using coal. However, instead of leading to a reduction in the amount of coal used, these efficiencies led to a broader range of applications for steam power. As a result, the overall consumption of coal increased dramatically. This paradox appears to be equally applicable today as we stand at the threshold of a new AI powered industrial revolution. As innovation by chipmakers drives a rapid rise in the computational power and efficiency of chips, the potential productivity benefits of AI across various industries is resulting in even greater demand for the technology, which in turn is leading to an increase in energy consumption despite these efficiency improvements. To put this into context, in theory, transitioning from a Hopper to a Blackwell-powered data centre should result in a fourfold reduction in power consumption. However, as depicted by the data in Figure 3, the opposite is true, because large AI companies and hyperscalers are instead maximising the use of these more powerful, efficient chips. This has resulted in the number of GPUs within a data centre increasing, underscoring the essence of the Jevons Paradox whereby increased efficiency leads to greater overall consumption due to expanded use. Figure 3: Data centre provider energy and electricity use

Source: Company reports and Barclays Research Critical questionsA historical barrier to AI development has been energy costs. Considering prevailing trends and their power implications, a crucial question arises: Where is this additional power going to come from and what are the implications for emissions? In exploring this issue, three key areas emerge as focal points:

The power demands of AI, combined with the impacts of reindustrialisation, EVs, and the shift to renewable energy, is creating strong market conditions for companies exposed to electrification. This is exemplified by power companies Vistra and Constellation Energy, which were among the best-performing US stocks year-to-date, rising more than 282% and 105% respectively at the time of publication.7

The potential physical constraints to AI's growth must also be examined. This encompasses not only the limitations of current technology and infrastructure but also the availability of resources needed to sustain the rapidly rising power demands of the technology.

To address these issues big hyperscalers have restated their commitments to decarbonisation pathways and some have turned towards nuclear energy as a solution, but this brings its own environmental considerations. We must consider the emissions profile of AI and the broader environmental impact of increased power consumption. This includes not just the immediate emissions from power generation but also its long-term sustainability. The emissions profiles of big tech companies have barely declined over the last several years, with the rise of AI creating even larger energy demands. According to research by AI startup Hugging Face and Carnegie Mellon University, using generative AI to create a single image takes as much energy as full charging a smartphone.8 Nuclear energy to fuel AI power demandTo illustrate the real-world implications of AI's increasing power demands, Microsoft recently announced a deal with Constellation Energy concerning the recommissioning of an 835 megawatt (MW) nuclear reactor at the Three Mile Island site in Pennyslyvania.9 This deal highlights the sheer scale of efforts being made to meet the growing power needs of AI. The move is part of Microsoft's broader commitment to its decarbonisation path, demonstrating how corporate power demands are intersecting with sustainable energy solutions. The cost of recommissioning the nuclear reactor is estimated at US$1.6 billion, with a projected timeline of three years for the reactor to become operational, with Microsoft targeting a 2028 completion date. In October, Alphabet finalised an order for seven small modular reactors (SMRs) from California-based Kairos Power to provide a low-carbon solution to power its data centres amid rising demand growth for AI and cloud storage. The first of these SMRs is due to be completed by 2030 with the remainder scheduled to go live by 2035.10 Amazon also announced that it has signed three new agreements to support the development of nuclear energy projects - including the construction of several new SMRs to address growing energy demands.11 These initiatives underscore the significant investments and timeframes involved in securing the additional power capacities required to support the escalating energy demands of modern computing and AI technologies. Further initiatives are expected given the incremental demand for data centre capacity in the US market is projected to grow by 10% per year for the next five years.12 This growth could result in data centres potentially representing up to 10% of the total US energy supply by 2030, which is significant given that Rystad Energy forecasts that total US power demand will grow by 175 TWh between 2023 and 2030, bringing the country's demand close to 4,500 TWh.13 While Microsoft is committing to nuclear power, a carbon-free source of electricity as part of its decarbonisation efforts, we remain cautious and concerned about how the energy gap required to support this growth in AI and data centres will be filled. Powering the futureEarlier this year, we engaged with Microsoft on its increase in emissions and commitment to renewable energy sourcing for data centres. In August, we were pleased to see Microsoft address concerns regarding the increasing energy requirements of AI and the resulting shift towards sustainable practices across the industry during its presentation to the Australian Senate Select Committee on Adopting AI.14 The hyperscaler acknowledged that AI models and related services require a lot more power than traditional cloud services and was a key issue the industry needed to address. Microsoft also stated that it remained on course to achieve its 2030 net zero and water-positive targets in its sustainability strategy. While the increased power demands were unknown in 2020 when the targets were set, the use of renewable and nuclear energy should enable the commitment to be sustainably met. Microsoft Founder Bill Gates has urged global policymakers to refrain from going "overboard" with regards their concerns about AI's energy footprint, noting that the technology will likely play a decisive role in achieving net zero ambitions by reducing global demand. AI and the energy transitionAdvancements in AI, when paired with innovations in renewables, may hold the key to sustainably meeting rising energy demand. The IEA reported that power sector investment in solar photovoltaic (PV) technology is projected to exceed US$500 billion in 2024, surpassing all other generation sources combined.15 By integrating AI into various solar energy applications, such as using technology to analyse meteorological data to produce more accurate weather forecasts, intermittent energy supply can be mitigated.16 Researchers are also relying on AI to accelerate innovation in energy storage systems, given existing conventional lithium batteries are unable to fulfil efficiency and capacity requirements.17 While AI will create additional demand for energy, it also has the potential to solve challenges related to the net zero transition. In April, the US Department of Energy (DoE) released a report outlining how AI will likely play a vital role in accelerating the development of a 100% clean electricity system.18 Significant opportunities in the following areas were outlined:

Beyond the grid, AI has the potential to play a significant role in supporting a variety of applications that can contribute to the development of a fair, clean energy economy, the DoE noted. Achieving a net zero greenhouse gas (GHG) emissions target throughout the economy involves overcoming distinct challenges in various sectors, such as transportation, buildings, industry, and agriculture. We are witnessing signs of growing demand for AI across various sectors including healthcare, transportation, finance, and industry, and we anticipate this to be a sustained, long-term trend. As a team we have benefited from involvement in AI and the wider movements towards electrification and re-industrialisation. However, we are conscious of the potential increase in carbon emissions due to AI's expansion and are closely monitoring the decarbonisation pledges of companies like Nvidia and Microsoft. While we anticipate a short-term rise in emissions, we are optimistic that AI will ultimately contribute positively to decarbonisation efforts through innovation and productivity enhancements and are confident that the heightened demand for power will be addressed by increased investment in clean energy. Despite this being a year marked by significant political changes worldwide, our outlook for investing in sustainable equities remains positive. Inflationary pressures are easing, and monetary policy appears to be taking a more supportive direction. Regardless of the political landscape, the fundamental trends we are focused on are continuing to advance and develop. |

|

Funds operated by this manager: Janus Henderson Australian Fixed Interest Fund, Janus Henderson Australian Fixed Interest Fund - Institutional, Janus Henderson Cash Fund - Institutional, Janus Henderson Conservative Fixed Interest Fund, Janus Henderson Conservative Fixed Interest Fund - Institutional, Janus Henderson Diversified Credit Fund, Janus Henderson Global Equity Income Fund, Janus Henderson Global Multi-Strategy Fund, Janus Henderson Global Natural Resources Fund, Janus Henderson Tactical Income Fund

IMPORTANT INFORMATION References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns. Sustainable or Environmental, Social and Governance (ESG) investing considers factors beyond traditional financial analysis. This may limit available investments and cause performance and exposures to differ from, and potentially be more concentrated in certain areas than the broader market. Footnotes and definitions 1International Energy Agency, 'Global trends in internet traffic, data centre workloads and data centre energy use, 2010-2019 (last updated 3 June 2020) 2International Energy Agency, 'Electricity 2024: Analysis and forecast to 2026' 3International Energy Agency, 'Electricity 2024: Analysis and forecast to 2026' 4University of Wisconsin-Madison, 'The Hidden Cost of AI' by Aaron R. Conklin (21 August 2024) 5Goldman Sachs, 'Generational growth: AI, data centres and the coming US power demand surge' (28 April 2024) 6Barclays Research, 'Artificial Intelligence is hungry for power' (28 August 2024) 7Google Finance, Market summary for Vistra, Constellation Energy (12 November 2024) 8MIT Technology Review, 'AI's carbon footprint is bigger than you think' (5 December 2023) 9Constellation Energy, press release (20 September 2024) 10Kairos Power, Press release (14 October 2024) 11Amazon, press release (16 October 2024) 12McKinsey, 'Investing in the rising data centre economy' (17 January 2023) 13Rystad Energy, 'Data centers and EV expansion create around 300 TWh increase in US electricity demand by 2030' (25 June 2024) 14ARNnet, 'Microsoft A/NZ acknowledges local energy usage increase due to AI' (August 2024) 15International Energy Agency, World Energy Investment 2024 Report 16World Economic Forum, 'Sun, sensors and silicon: How AI is revolutionizing solar farms' (2 August 2024)15Source: ERGO Group, 'How AI is helping with battery development' (20 August 2024) 17Dean H. Barrett and Aderemi Haruna, Molecular Sciences Institute, School of Chemistry, University of the Witwatersrand, 'Artificial intelligence and machine learning for targeted energy storage solutions' 18Source: US Department of Energy, AI for Energy: Opportunities for a Modern Grid and Clean Energy Economy (April 2024) FLOPS: Stands for Floating Point Operations Per Second (FLOPS), and it's a measure of a computer's performance, especially in fields that require a large number of floating-point calculations. Higher FLOPS indicate more calculations can be done per second, which is particularly relevant for training and running complex machine learning models. FLOPS/Watt is a measure of computational efficiency, indicating how many floating-point operations a system can perform per unit of power consumed. The higher the FLOPS/Watt, the more energy-efficient the system is. Inference: Within the context of this article, this refers to the process of using a trained model to make predictions or decisions based on new, unseen data. In the context of language models, inference would involve tasks like generating text responses, translating languages, or answering questions. Joule: A unit of energy in the International System of Units. It's a measure of the amount of work done, or energy transferred, when applying one newton of force over a displacement of one meter, or one second of passing an electric current of one ampere through a resistance of one ohm. Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. Monetary policy tools include setting interest rates and controlling the supply of money. Monetary stimulus refers to a central bank increasing the supply of money and lowering borrowing costs. Monetary tightening refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money. See also fiscal policy. Net zero: A state in which greenhouse gases, such as Carbon Dioxide (C02) that contribute to global warming, going into the atmosphere are balanced by their removal out of the atmosphere. Per token: In natural language processing (NLP), a "token" typically refers to a piece of text, which could be a word, part of a word, or even a character, depending on the granularity of the model. Thus, "per token" means that the energy usage is being measured with respect to each individual piece of text processed by the model. Watt: A unit of power in the International System of Units, representing the rate of energy transfer of one joule per second. All opinions and estimates in this information are subject to change without notice and are the views of the author at the time of publication. Janus Henderson is not under any obligation to update this information to the extent that it is or becomes out of date or incorrect. The information herein shall not in any way constitute advice or an invitation to invest. It is solely for information purposes and subject to change without notice. This information does not purport to be a comprehensive statement or description of any markets or securities referred to within. Any references to individual securities do not constitute a securities recommendation. Past performance is not indicative of future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested. Whilst Janus Henderson believe that the information is correct at the date of publication, no warranty or representation is given to this effect and no responsibility can be accepted by Janus Henderson to any end users for any action taken on the basis of this information. |

11 Dec 2024 -

|

"A is for Ambition": Apple and Amazon Bet Big on the Future Alphinity Investment Management December 2024 |

|

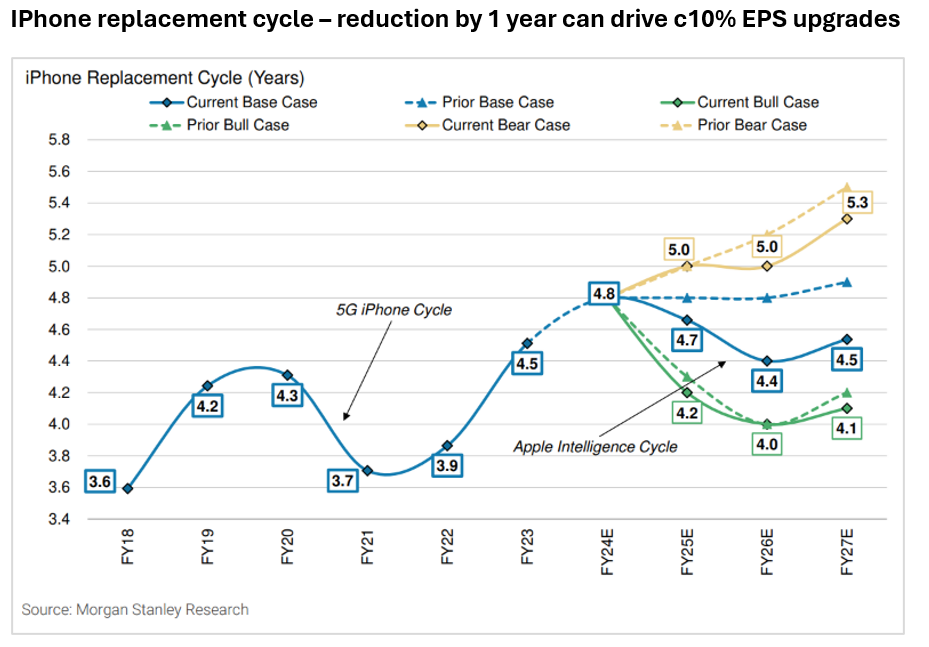

The recent Apple and Amazon third quarter 2024 results revealed further details around the critical leg of their strategies, with these tech giants continuing to lay down markers for how they see the next stage of tech evolution unfolding and staking out positions to profit from it. Looming large in this evolution is AI, with Apple looking to leverage capabilities across what is an enormous ecosystem of 2.2bn active devices while Amazon is focusing on pushing AI applications across their Cloud and consumer business. The recent results also provided key insights into shorter term business performance.  Key takeaway from the result? The key takeaway from the Apple result is that while the gains from the release of "Apple Intelligence" will be significant, they will take time. This was evidenced by the fact that despite this recent result coming in ahead of expectations, it was coupled with a guide for the coming quarter that was mildly below what the market was looking for (Apple guided to revenue growth of low to mid-single digits vs a market that was expecting +7%). This makes sense as "Apple Intelligence" has only just rolled out in the US in recent weeks, and will not become available in the UK, Australia, Canada, and New Zealand until December 2024. Other geographies will follow over the course of 2025. Most importantly, it is also December 2024 before we see a meaningful expansion of the AI features including the long-awaited Chat GPT integration. As such, the powerful iPhone upgrade cycle that we expect to come with "Apple Intelligence" is likely to be a slow burn, with momentum building through 2025 and into 2026. What impressed? The ability of Apple to turn a benign demand environment into double digit EPS growth is impressive. Products growth has been tepid but the higher growth Services business, margin expansion and a buy-back continues to drive EPS growth above 10%. What disappointed? While we appreciate that Apple Intelligence will take time, the pace of the roll-out driving the weaker than expected outlook for 4Q (which is their biggest quarter of the year) was mildly disappointing. However, Apple tend to focus on quality rather than speed, so we do think that their ability to monetise AI across an installed base of 2.2bn active devices is a compelling, multi-year opportunity. Interesting chart? The next phase for Apple is all about an iPhone replacement cycle coupled with an expansion of associated Services revenue. The chart below shows what happened the last time a compelling technology shift occurred, with 5G driving a compression in this replacement cycle. Since the most recent trough in FY21, replacement cycles have shifted out by more than 12 months. A compression of this replacement cycle back towards 4yrs will drive circa 10% EPS upgrades.  What are the key risks? There are a few key risks facing Apple in the coming years. Key among these are:

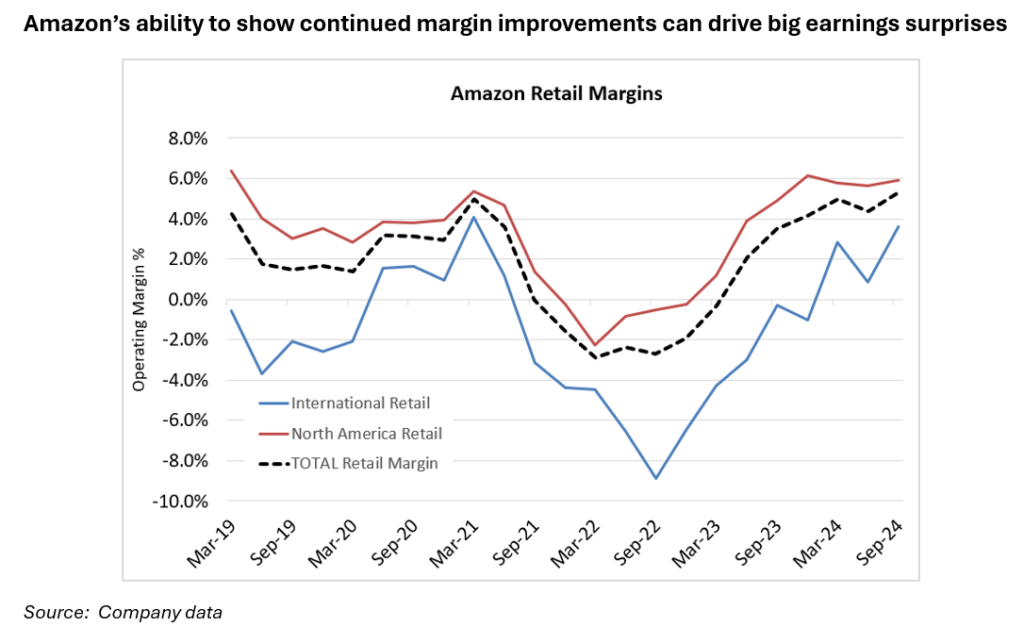

In summary, Apple's ability to monetise their enormous consumer ecosystem is almost unrivalled. They will find a structure through which to monetise Ai, both through device sales but more importantly through an expansion of Ai related Services offerings. There is no company better placed to be the window into Ai for the average consumer.  Key takeaway from the result? Margins, margins, margins. Given the scale of the Amazon business, a mild shift in margin outcomes can drive enormous gains in operating income and EPS. Amazon spooked the market during their 2Q24 results which showed margins for their core retail business to be weaker than expected, which was blamed on everything from mix (lower priced "everyday essentials" in baskets) to building extra satellites for their broadband business. However, come the 3Q24 result last week, all was forgotten as Amazon blew those margin expectations (that they ironically had guided to themselves) out of the water. So, the question becomes, will this margin expansion continue? What impressed? The margin outcome in the core retail business was impressive, particularly in the international segment. Despite pressures from mix and what appears to be heightened competition from legacy retailers (eg Walmart) and Chinese players (Temu, Shein), Amazon generated solid topline growth and exceptional margins. The Amazon cloud business AWS also showed a continuing reacceleration driven in part by AI. A combination of the "law of large numbers" plus optimisations had driven compression in cloud growth rates across Amazon (AWS), Microsoft (Azure) and Google (GCP). However, the advent of AI has driven a reacceleration in cloud growth, which is impressive given the base of business is significantly larger. What disappointed? While it may seem unusual to have any source of disappointment in an exceptionally strong result, the variability of the margin outcomes compared to what management expected could indicate a lack of visibility. While a "miss vs expectations" is very happily received when it is an upside surprise, it does raise some concerns that perhaps next time the "surprise" could be the other way. Interesting chart? Given the scale of the retail business, a shift in margin expectations has a material impact on earnings. A circa 100bps improvement in Retail margins vs current expectations for CY25 would drive a 7% beat in Amazon operating income.  What are the key risks? For Amazon, risks are on a couple of key fronts:

In summary, Amazon's 3Q24 earnings report highlighted the significant earnings potential of the business and underscored the company's strong market position and attractive consumer offerings. However, it is crucial to closely monitor Amazon's ability to sustain margin improvements and effectively navigate ongoing consumer pressures in the future. |

|

Funds operated by this manager: Alphinity Australian Share Fund, Alphinity Concentrated Australian Share Fund, Alphinity Global Equity Fund, Alphinity Global Sustainable Equity Fund, Alphinity Sustainable Share Fund |

10 Dec 2024 - Mixed market sentiment for 2025 driven by global geopolitics and central bank easing cycles

|

Mixed market sentiment for 2025 driven by global geopolitics and central bank easing cycles Bennelong Funds Management November 2024 The incoming Trump administration has raised uncertainty about the outlook for global markets in 2025, particularly around the implementation of Trump's protectionist policies, according to Bennelong and its boutique partners Canopy Investors, 4D Infrastructure and Quay Global Investors.

The new US administration's activities and policy changes will be very important in driving market sentiment in 2025, and will create both opportunities and risks, according to Canopy Investors' portfolio manager, Kris Webster. "There remains significant uncertainty about the actual policies that will be introduced, and their ultimate impact, making the outlook for 2025 very uncertain. "However, based on Trump's stated policy positions, several domestic US sectors appear well positioned to benefit from his presidency. These include manufacturers, energy companies, and industries targeted for deregulation, for example financials. "Conversely, certain sectors may face headwinds including global exporters to the US, US importers, and companies with substantial China exposure. "Markets have already priced in some of these policy expectations, as evidenced by US dollar strength against major currencies. This dynamic has created increasingly attractive valuations for many high-quality stocks in markets outside the US, particularly those with limited exposure to US policy changes. Mr Webster says a critical uncertainty centres on how these policies might affect inflation and, by extension, interest rates - both of which significantly influence asset prices and highly leveraged companies. "It's possible the US government will moderate its policies around taxation, tariffs, and immigration, if inflation picks up again. "While we don't make short-term macro or market predictions, it is likely that the policy uncertainty anticipated in 2025 will drive increased market volatility. This environment should create opportunities for active investing, particularly in global small and mid-cap companies, where market inefficiencies tend to be more pronounced," he says. For global listed infrastructure, there is likely to be heightened policy noise in the US on what policies are prioritised for actual implementation, according to 4D Infrastructure CIO, Sarah Shaw. "Most notably, these include the 60 per cent tariff on Chinese goods and a universal 10 to 20 per cent tariff on all other countries. These could have an impact on infrastructure assets, in particular port and rail volumes in both export and import countries, with some volumes pulled forward ahead of the anticipated tariff increases, whilst some export markets will be substituted with other destination markets away from the US. "Trump is also looking to repeal some aspects of the Inflation Reduction Act (IRA), which may impact the growth outlook of some heavily US renewable focused developers and utilities. This could lead to an ongoing overhang till we see what is exactly implemented. "This pivot away from renewables and preferring traditional fossil fuels may be positive for north American pipelines if more federal lands are permitted for exploration. An undoing of Biden's pause of new LNG Export terminals will also help the long-term capital plans of those businesses," she says. "Lastly, the proposed policies are inflationary and a reversal in trend of interest rates could be a headwind for US nominal rate utilities which have had an incredibly strong year in 2024" Elsewhere in the world, Ms Shaw says there are divergent economic outlooks. "In Europe demand remains soft with interest rate trajectory down. China continues to struggle with a dormant economic outlook, increasing stimulus. In Brazil, growth continues to surprise to the upside with a reversal in the interest rate trajectory." Ms Shaw says that this macro uncertainty and geopolitical tensions will create volatility and noise, however by separating the attractive fundamentals of infrastructure from this noise and continuing to invest against the inefficiency of markets, investors can capture future earnings and growth in this asset class. "Infrastructure offers a unique combination of defensive characteristics and earnings resilience but with significant long-term growth thematics as well as an ability to capture economic cycles. "The need for global infrastructure investment over the coming decades is clear with five globally relevant and necessary thematics under pinning a multi decade growth story. With governments unable to wholly fund the infrastructure need, there's a significant opportunity for private investors to tap into this growth story. We can think of no more compelling or enduring global investment thematic for the coming 50 years," says Ms Shaw. Chris Bedingfield, portfolio manager at Quay Global Investors, sees a similar mixed story for global real estate assets. "Investors continue to make the mistake of thinking real estate is interest rate driven but the value in real estate can be found by focusing on thematics not influenced by macros factors or politics. "The aging population is a thematic we are focused on and 2025 marks the 80-year anniversary of the end of the second world war, meaning that next year, the first of the Baby Boomers will turn 80, an age where many turn to some type of assisted living. "Retail also continues to look very attractive. The recovery of in-store retail sales since COVID remains well above the prior pandemic trend. We expect good financial results from the best malls in 2025 as landlords continue to mark rents back to economic reality." Mr Bedingfield says there are signs that suggest a positive outlook for global REITs. "Timing the markets is hard. Miss a few good days and long-term total returns can alter significantly. This is especially so for listed real estate. "History suggests listed REITs run in anticipation of US Fed rate cuts and continue to perform for some time after, and we've seen this materialise after the first rate cut in September. "Moreover, higher building costs is already resulting in a shortage of global real estate, as the development equation does not work. This will simply squeeze future tenants, all the more to the benefit of landlords and investors of REITs," he says. The content contained in this article represents the opinions of the authors. The authors may hold either long or short positions in securities of various companies discussed in the article. The commentary in this article in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader. |

9 Dec 2024 - How Trump will impact equity markets

|

How Trump will impact equity markets Magellan Asset Management November 2024 |

|

The United States has spoken. President Trump will return to the White House in the new year. But how can we cut through the noise to reveal the investment, economic and geopolitical ramifications? Magellan's Head of Global Equities and Portfolio Manager, Arvid Streimann, has over 25 years' experience of following markets and politics, and over this time has built up a network of trusted contacts, he can offer a measured, independent view of the situation, including his expectations on Donald Trump's policy initiatives and decision making. He's joined by Investment Director Elisa Di Marco for an exploration of the implications of a Republican clean sweep, including the impact on standards of living and consumer sentiment, as well as the potential for deregulation, and President Trump's promise to adopt protectionist policies in an effort to develop self-sufficiency. They share insights into geopolitical dynamics, including U.S.-China relations, Iran and Ukraine, and discuss the risks and opportunities for investors. |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Core Infrastructure Fund, Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged) Important Information: Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to a Magellan financial product may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Magellan will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Magellan claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

6 Dec 2024 - Risks & Issues for 2025 - Part 1

6 Dec 2024 - How Co-Investments are Transforming Affordable Housing

|

How Co-Investments are Transforming Affordable Housing HOPE Housing Fund Management November 2024 Wholesale and sophisticated investors have traditionally pursued two objectives: achieving strong returns while remaining sufficiently diversified. More recently, they've had to consider a third objective, which is to potentially incorporate ESG principles into their investment process. What makes this challenging is that it can feel like there is tension between the three objectives; that pursuing one must come at the expense of one or both of the others. That's why investors will always look closely at any investment option that appears to align with all three objectives. Now that housing affordability has become such a serious social issue in Australia, an opportunity exists for a clever fund manager to offer a new way to invest in residential real estate. To really attract investors, it would need to deliver all three objectives - the prospect of strong returns and prudent diversification, while simultaneously addressing the affordability crisis. Australia's housing affordability problem is getting worseThe reason this kind of idea is now on the radar of the investment community is because, as property prices keep increasing, the affordability crisis keeps growing. The biggest issue is not paying off ever-larger mortgages but saving the deposit required to enter the market in the first place; because, for many people, especially essential workers on lower incomes, property prices can increase faster than their capacity to save. A 2023 report1 from ANZ and CoreLogic found that the time required for people on the median income level to save a 20% house deposit was 10.7 years across Australia, including 15.7 years in Sydney, 11.6 years in Melbourne and 10.8 years in Brisbane. Domain research2 from 2024 found that the sum required for a 20% house deposit more than doubled in Sydney between 2013 and 2023, from $153,361 to $319,062, and almost doubled in Melbourne ($117,574 to $209,455) and Brisbane ($92,153 to $177,657). Meanwhile, a 2023 report3 from the Australian Housing and Urban Research Institute (AHURI) revealed that successive generations have been experiencing lower rates of home ownership. "Home ownership rates at age 30 have fallen from a high of 65% among those born in the late 1950s to around 45% among those born in the 1980s. By age 50 there is incomplete catch-up in home ownership rates - which means that younger cohorts do not close the gap and catch up with their older counterparts. Around 25% of the homeownership gap remains," according to the report. First home buyers are co-investing with the Bank of Mum & DadThe AHURI report noted that parents are increasingly helping their children enter the market, by letting them live rent-free in the family home while they save a deposit, providing direct cash support or going guarantor on a loan. Remarkably, there has been such a rise in Bank of Mum & Dad activity that, in aggregate, it is now "among the top 10 mortgage providers in the country". The report also pointed out the important link between Bank of Mum & Dad support and entry into home ownership. "The receipt of large parental transfers (over $10,000) is associated with a doubling of the rate of transition into home ownership; additional time spent co-residing with parents increases the probability of transitioning into home ownership by around 40% relative to those in rental tenure," according to the report. Two conclusions come to mind after reading this research:

Exploring government co-investment opportunitiesSo what options do people have if they can't access Bank of Mum & Dad support? The most obvious option is to stay in the rental market, but this is tougher than it sounds. As of January 2024, the national rental vacancy rate was at a record-low 0.8%, according to Domain4, making it hard for tenants to find accommodation. As a result, rents5 in the combined capital cities were at record highs at the end of 2023, with median house rents jumping 12.3% in Sydney over the course of the year, 14.6% in Melbourne and 9.1% in Brisbane. That means renters on below-average incomes are being forced out further and further from the city centre. Another option is to try to save a deposit for a home on the outskirts of the city, where prices can still be dear but are much more affordable than close to the city. The downside, though, is that buyers face an exhausting commute if they work in the city's inner ring. A third option is to take advantage of government co-investments. In November 2024, the Senate passed the Help to Buy program, a shared-equity scheme under which the Federal government will make an equity contribution of up to 40% for new homes and 30% for existing homes. This scheme will be limited to buyers with a household income of less than $90,000 for single buyers or $120,000 for couples. New South Wales previously had a similar equity co-investment scheme, called Shared Equity Home Buyer Helper. This offered the same equity contribution (40% for new homes, 30% for existing homes) and had similar income caps. Under the Victorian Homebuyer Fund, the state government acts as co-investors by providing an equity contribution of up to 25%. Income caps apply - $130,485 for individuals and $208,775 for joint applicants. Queensland helps public housing residents buy the home they're renting with the Pathways Shared Equity Loan. The government makes an equity contribution of up to 40%. Western Australia offers equity co-investments of up to 30% through its Keystart program. Income caps (which are variable) apply. South Australia also does property co-investments. Under HomeStart, the state makes equity contributions of up to 25%. Participants' household income must be less than $100,000. Tasmania has a co-investment program called MyHome, which makes an equity contribution of up to 40% for new homes and 30% for existing homes. Income caps (which are variable) apply. In the ACT, the Shared Equity Scheme helps public housing tenants purchase their home through a government equity contribution of up to 30%. Australia's aspiring homeowners need institutional investors to step into the residential property marketCo-investments of the kind launched by state and federal governments play a positive role in making it easier for Australians to get on the property ladder. However there are only so many places available in these programs and they are (reasonably) targeted at people on lower incomes. Yet research shows middle-income earners are just as challenged by home ownership, however are often excluded from government support. To broaden the reach of co-investment, especially to those without the bank of mum and dad, there is a role for private market solutions, sponsored by Australia's deep pool of institutional capital - superannuation. By expanding the reach of shared equity schemes that have been proven to work, more Australians who are dealing with housing affordability challenges and mortgage stress can be assisted. To date, large institutional investors in Australia have not turned their mind to this new co-investment opportunity. This is despite many institutional investors in the UK, Canada and the US having great success in shared equity and shared ownership. Much of this is to do with the narrow focus local superannuation funds have had on residential investing, mainly looking at investing in new rental projects aimed at low-income workers. These projects, often termed 'Build to Rent' carry significant construction and occupancy risk and can require government subsidies to obtain commercial returns. For these reasons, among others, the majority of Australia's institutional investors have found the risk-adjusted returns in affordable housing investments unappealing. Over time, it is expected that local superannuation funds will broaden their residential portfolio construction approach, to ensure they are investing to support their members across both increased affordable rental and home ownership solutions. The latter is important, as home ownership contributes to security in retirement in a way long-term renting cannot, and furthers their mission of enabling Australians to have a dignified retirement. How HOPE Housing Fund Management has made co-investments profitableThe question of how institutional investors can identify opportunities in the affordable housing space, that deliver optimal risk-adjusted returns leads us back to the issue raised at the start of this article: could a clever fund manager create an investment option that not only addressed the housing affordability crisis, but also provided investors with strong returns and prudent diversification, with no need for government subsidies? The answer is yes, thanks to HOPE Housing Fund Management (HOPE/HOPE Housing/Fund Manager), the first co-investor that helps essential workers - such as cleaners, nurses, teachers, social workers and first responders - purchase a home close to work. The Fund Manager successfully closed its first fund, HOPE Fund I in October of 2024, and has recently launched its second fund, HOPE Fund II, pursuing the same shared equity strategy. In the HOPE Housing model, buyers make an equity contribution of around50%, through a deposit and mortgage, and the HOPE Fund II will provide the rest. This significantly lowers the deposit hurdle for essential workers, who often have limited incomes, giving them the chance to not only get on the property ladder but also buy close to the city. The Fund Manager's innovative solution also supports essential workers to stay in their jobs, rather than being forced to switch to a higher-paid profession, just so they can buy a home. HOPE Fund II accepts contributions from wholesale or sophisticated investors, who must invest at least $100,000. These funds are pooled, so investors back a portfolio of co-investment opportunities, rather than just one. As at September 2024, HOPE Fund I has achieved a 11.2%(A) portfolio asset growth since inception, exceeding the broader Sydney property market's 7.3% (B) growth calculated for the same period. HOPE uses pre-purchase independent valuations and an investment committee review process, to ensure buyers purchase investment-grade properties. HOPE's co-investing model offers a different risk/return profile than the Build-To-Rent model and gives high-net-worth and institutional investors the chance to achieve much loved property market returns while helping to solve a hugely challenging social issue. Since establishing in October 2022 , HOPE Fund I has invested in 20 properties that house 31 essential workers (as some households have more than one), as of September 2024. Invest in property, without compounding the problemThanks to HOPE's unique solution, wholesale and sophisticated investors no longer have to make a trade-off between making money and doing good. Now, they can fulfil their investment mandates while helping to solve one of Australia's biggest social problems. What makes this solution so heartening is that it really is win-win - investors benefit, but so do their co-investors, the essential workers who are supported by the scheme. HOPE is leading the way with this Australia-first initiative. As its impact grows, it wouldn't be surprising if other organisations were inspired to create something similar. Webinar Invitation Join us to learn more about how an investment in the HOPE Housing Residential Property Trust works. HOPE Housing Investment Webinar - Wednesday 11th December 2024, 12.00pm - 12.45pm |

|

Funds operated by this manager: HOPE Housing Investment Trust, HOPE Housing Residential Property Trust Footnotes 1 https://media.anz.com/posts/2023/november/undersupply-of-housing-impacts-affordability 2 https://www.domain.com.au/news/house-deposits-have-nearly-doubled-in-the-last-decade-1259217/ 3 https://www.ahuri.edu.au/research/final-reports/404 4 https://www.domain.com.au/group/media-releases/competition-easing-amidst-record-low-vacancy-rates/ 5 https://www.domain.com.au/research/rental-report/december-2023/ Important Information Past performance is not a reliable indicator of future performance. Prospective investors should carefully review HOPE Fund II's Information Memorandum (IM) in full and seek professional advice prior to making any investment decision. For more information about the Fund, please refer to the Investor Disclaimer on our website. The information in this article was finalised in November 2024. (A) The Portfolio Growth since inception p.a. represents the cumulative growth since HOPE Fund I portfolio inception date of 16 November 2022. Portfolio growth is determined by estimating market value of the properties within the Fund's portfolio monthly, using CoreLogic IntelliVal (Automated Valuation Estimate) and PropTrack AVM. The change in total portfolio value is indexed from a base value of 100, established at the inception of the Fund's portfolio, to account for the addition of new properties during the same period. The portfolio growth information does not take into account liabilities or expenses of the Fund and therefore may not reflect overall Fund performance. (B) The CoreLogic Benchmark is derived using the 'CoreLogic Hedonic Home Index reports' for 'All Dwellings' in the Sydney market, since the HOPE Fund I portfolio inception date of 16 November 2022. This is the growth of residential real estate in the Sydney market. The detailed methodology of the CoreLogic Hedonic Home Index can be found on the CoreLogic Australia website. © Copyright 2024. RP Data Pty Ltd trading as CoreLogic Asia Pacific (CoreLogic) and its licensors are the sole and exclusive owners of all rights, title and interest (including intellectual property rights) subsisting in this publication, including any data, analytics, statistics and other information contained in this publication (Data) . All rights reserved. The article has been prepared by HOPE Housing Fund Management Limited ACN 629 589 939 (Investment Manager/Manager/Company/HOPE/HOPE Housing) directed to wholesale clients and is strictly for general information and discussion purposes only, without taking into account your personal objectives, financial situation or needs. Before acting on this general information, you must consider its appropriateness having regard to your own objectives, financial situation and needs. The information provided is not intended to replace or serve as a substitute for any accounting, tax or other professional advice, consultation or service and nothing in this article shall be construed as a solicitation to buy or sell any financial product, or to engage in or refrain from engaging in any transaction. The Investment Manager is a corporate authorised representative (number 001289514) of SILC Fiduciary Solutions Pty Ltd ACN 638 984 602 (AFS licence number 522145). The authority of the Investment Manager is limited to general advice and deal by arranging services to wholesale clients relating to the HOPE Housing Residential Property Trust (Fund/HOPE Fund II) in Australia only. |