NEWS

19 Jan 2023 - Oil drops to lowest level of 2022 but supply-demand is likely to tighten over the medium term

|

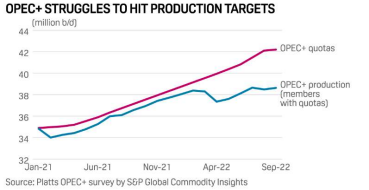

Oil drops to lowest level of 2022 but supply-demand is likely to tighten over the medium term Ox Capital (Fidante Partners) December 2022 The low oil price today is a result of weak demand (global economic malaise) and increased supply (US strategic oil reserve release). These factors will likely normalise in coming quarters. Over the longer term, demand is set to pick up driven by China opening up and the secular economic growth of other emerging economies. Demand is likely to significantly outstrip supply given the lack of investment that has gone into the sector.

Oil price has pulled back from over US$120 per barrel in June to less than US$80 per barrel over the last week. The oil market is factoring in a short-term slowdown in demand as rising interest rates start to impact real economic activities globally. We remain optimistic about the return potential of the energy sector in the coming years. Approximately 100M barrels of oil are consumed globally each day. A surplus or deficit of 1% or ~1M barrels can lead to significant price move. At present, oil demand is artificially low and is still below pre-covid levels. In China, oil demand is ~1M barrels per day below 2021 levels because of Covid lockdown, and global jet fuel consumption is ~2M barrels per day below 2019 levels. In terms of supply, the US government has been releasing its strategic petroleum reserves, adding 0.8M barrels a day to global supply since March 2022. This will slow as we go into 2023. As a result of the short-term demand and supply distortions, OPEC+ is cutting output by 2M barrels per day by the end of 2023 to support prices, illustrating supply discipline that can be flexibly applied to uphold a quasi-price floor if required going forward. Over the longer term, it has been evident that the members of OPEC+ has been struggling to produce to their quotas over 2021 and 2022. This is likely a result of a lack of investment in oil projects over the last decade. The upside for oil price can be significant as China opens up and other emerging economies continue to grow. Supply will struggle to keep up. Major oil companies in Europe are attractively valued and are trading at a significant discount to many of the oil majors in the US. Even at an oil price of US$70, European energy companies are typically trading on 5xPE, 15% free cash flow yield, compared to 14xpe and 7.5% free cash flow yield for the Americans. Ox has selective investments in some of the leading players in this space. The current pullback in oil can create additional investment opportunities for 2023, of which we are on the lookout. Funds operated by this manager: |

18 Jan 2023 - Australian Secure Capital Fund - Market Update

|

Australian Secure Capital Fund - Market Update November Australian Secure Capital Fund November 2022

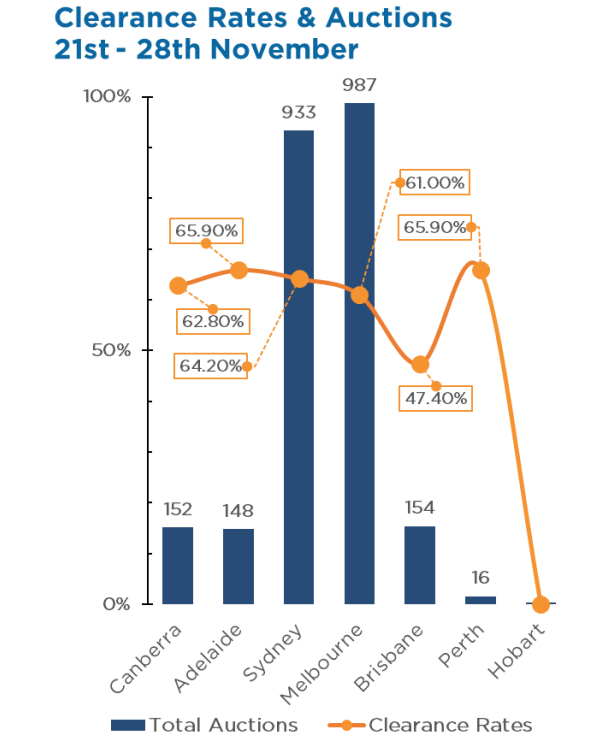

Property prices continued to fall across the nation with values declining a further 1.00% throughout November. This brings an approximate 7.00% (average of $53,400) decline since national property prices peaked in April of this year. Whilst this marks the seventh month of decline, the rate at which prices are declining is beginning to soften, with the 1.00% reduction being the smallest since the 1.60% monthly decline in August. Queensland again recorded the most significant monthly reduction, along with Tasmania with a 2.00% reduction in the Home Value Index. New South Wales, Canberra, Victoria and South Australia also experienced a reduction in value with 1.30%, 1.20%, 0.80% and 0.30% respectively. Western Australia remained stable, and the Northern Territory actually saw a small increase of 0.20% for the month. Record low vacancy rates of 1.00% have allowed unit prices continue to remain somewhat resilient, recording a 0.60% reduction for the month, bringing 4.70% reduction since prices peaked. The number of auctions held in the last weekend of November remained considerably below that of last year, with 2,393 auctions taking place as opposed to 4,251 last year. Whilst well below that of last year, the number of auctions were up 4.10% on the previous weeks results and were in fact the highest since a weekend in mid-June recorded 2,528 auctions. Clearance rates across the nation were also down on last year's figures, with only 61.50% of auctions clearing (down from 68.50% last year) indicating that vendors may not yet have responded to market conditions. Adelaide again recorded the highest clearance rate for the weekend with 65.90%, followed by Sydney (64.20%), Canberra (62.80%), Melbourne (61.00%) and Brisbane (47.40%). Source: Article, Report Funds operated by this manager: ASCF High Yield Fund, ASCF Premium Capital Fund, ASCF Select Income Fund |

17 Jan 2023 - Glenmore Asset Management - Market Commentary

|

Market Commentary - November Glenmore Asset Management December 2022 Equity markets globally were stronger in November. In the US, the S&P 500 was up +5.4%, the Nasdaq rose +4.4%, whilst in the UK, the FTSE 100 increased +6.7%, boosted by its heavy mining weighting. On the ASX, the All Ordinaries Accumulation Index rose +6.4%. Utilities were the best performing sector, boosted by the takeover bid for index heavyweight Origin Energy, which was up +41% in the month. Materials was the next best sector, driven by investor optimism around China loosening its covid lockdown measures. Telco's, financials and technology all underperformed in the month. Bond yields declined in November as investors started to become more positive that the pace of interest rate hikes from central banks will moderate along with some signs that inflation has potentially peaked. In the US, the 10 year bond yield fell -30 basis points (bp) to close at 3.74%, whilst in Australia, the 10 year rate fell -23bp to 3.53%. During the month, the RBA increased interest rates by 25bp for the seventh month in a row, taking the official cash rate to 2.85%. The A$/US$ rallied in the month, up +6.0% to close at US$0.68. Commodity prices were broadly higher. Nickel rose +23%, whilst copper, aluminium and lead also rose between +6-8%. Thermal coal rebounded +11.4% after an -18% decline in October. Also of note, iron ore was up +25.6% after falling for seven months in a row. Brent crude oil fell -10.0%. Funds operated by this manager: |

16 Jan 2023 - New Funds on Fundmonitors.com

|

New Funds on FundMonitors.com |

|

Below are some of the funds we've recently added to our database. Follow the links to view each fund's profile, where you'll have access to their offer documents, monthly reports, historical returns, performance analytics, rankings, research, platform availability, and news & insights. |

|

|

|||||||||||||||||||

| Collins St Convertible Notes Fund | |||||||||||||||||||

|

|||||||||||||||||||

|

|||||||||||||||||||

| Capital Group Global Total Return Bond Fund (AU) | |||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

|||||||||||||||||||

|

Emit Capital Climate Finance Equity Fund |

|||||||||||||||||||

|

|||||||||||||||||||

| View Profile | |||||||||||||||||||

|

Want to see more funds? |

|||||||||||||||||||

|

Subscribe for full access to these funds and over 700 others |

16 Jan 2023 - The Investment Outlook 2023

|

The Investment Outlook 2023 abrdn December 2022 As we look back on 2022, to describe the year as eventful seems an absurd understatement. So many events have dominated the news, each individually significant, and in aggregate almost overwhelming in consequence, both politically and economically. Here's a reminder of just a few of those events:

Climate crisis uncertaintyYet all these things will be relatively short-lived in their impact (and manageable) when compared to the existential threat that continues to grow relatively unabated from our failure to make progress on constraining global warming to the agreed target of 1.5°C. COP 27, the climate change conference held this year in Egypt, largely failed to expand on commitments made a year earlier with regards to phasing out fossil fuels, despite all the strong statements made around the necessity to do so. The one major step forward was the agreement of a deal that has been sought for over 30 years to launch a fund for 'loss and damage' to support those nations most exposed to the consequences of climate change. But details and financial funding have not been agreed. We can already observe more extreme weather events - notably the recent floods in Pakistan - which have devastating effects on impacted economies and contribute to the risk of a steady but dramatically expanded flow of migrants to other countries. Don't give upBut, as the old saying goes, where there are challenges, there are also opportunities. Here's where we see them:

Reasons to be optimisticIt's easy to be overwhelmed by all the uncertainty. That said, we've also seen steady progress in many places that may offer an antidote to the gloom:

2023 may well be a pivotal year for markets amid the economic challenges that remain. While these are clearly important, we mustn't take our eyes off potentially existential long-term issues. Author: Sir Douglas Flint, Chairman of abrdn |

|

Funds operated by this manager: Aberdeen Standard Actively Hedged International Equities Fund, Aberdeen Standard Asian Opportunities Fund, Aberdeen Standard Australian Small Companies Fund, Aberdeen Standard Emerging Opportunities Fund, Aberdeen Standard Ex-20 Australian Equities Fund (Class A), Aberdeen Standard Focused Sustainable Australian Equity Fund, Aberdeen Standard Fully Hedged International Equities Fund, Aberdeen Standard Global Absolute Return Strategies Fund, Aberdeen Standard Global Corporate Bond Fund, Aberdeen Standard International Equity Fund , Aberdeen Standard Life Absolute Return Global Bond Strategies Fund, Aberdeen Standard Multi Asset Real Return Fund, Aberdeen Standard Multi-Asset Income Fund |

22 Dec 2022 - Investment Perspectives: The yield curve, recessions and soft landings

22 Dec 2022 - Why the cloud investment opportunity will outlast an economic downturn

|

Why the cloud investment opportunity will outlast an economic downturn Magellan Asset Management November 2022 |

|

The global shift to cloud computing is a seismic and transformational trend that we have backed for several years at Magellan. For the hyperscale public cloud vendors outside China - Amazon, Microsoft, and Google (the Magellan Global Fund holds all three companies) - it has created unprecedented market opportunity. These vendors have consistently generated strong double-digit revenue growth at scale and continue to do so to this day. Yet in the most recent two financial quarters, hyperscale cloud revenue has faced decelerating growth as enterprise customers reign in spend amid the uncertain macroeconomic backdrop. Has the story come to an end?

The trend this year is apparent. Excluding the impact of currency movements, hyperscale cloud revenue grew in aggregate 42% year-over-year in Q1. In Q2, the growth rate fell to 38%, and in the most recent Q3, the growth fell further to 34%. The two largest vendors, Amazon and Microsoft, expect this deceleration to continue, which means we should expect the growth rate to decline even more in Q4. On top of that, margins are falling, with both companies dealing with rising energy costs in their data centres while continuing to maintain their pace of double-digit operating expense growth. All of this may seem dire but let us unpack it further. We start by recognising that the deceleration this year appears more severe because it is being compared to several quarters of strong growth in 2021 due to cloud demand created by the pandemic responses. To try to adjust for this by looking at this year's quarterly growth rates on a 2-year annualised basis, we see a steadier growth trend, albeit one that is still slowing - from 40% in Q1, to 39% in Q2, to 38% in Q3. (The fact that we are seeing this type of growth on an aggregate US$160 billion in annualised revenue is staggering on its own). These decreases are more marginal and subject to noise, but there is broader evidence that IT spend is generally tightening. The unfavourability of these recent IT spending trends are, we believe, cyclical not structural. Market uncertainty has compelled enterprise customers to become more prudent or selective about their IT investments. Some customers are in industries facing challenges of their own such as supply chain issues, inflation, or labour shortages. We also expect some spend was driven by the period of excessive cheap, available money and this spend will not return. And as their customers seek to tighten their belts, hyperscale cloud vendors are taking it a step further and in fact helping customers to improve the efficiency of their spend (e.g., through lower priced options). In other words, the cloud vendors are effectively contributing to their own growth headwinds. Why do this? It is about driving trusted partnerships with customers for long term growth, rather than short-sightedly focusing on maximising growth today. This makes sense if one believes, as we do, that cloud has a significant multi-year growth runway ahead. In fact, the ability for customers to proactively dial up and down cloud spend according to their needs - rather than being burdened with the large, fixed costs of an on-premises data centre when times are tough - is one of the fundamental value propositions of the cloud, and the current environment reinforces this validity. Put another way, hyperscale cloud is doing exactly what it was meant to do. The effect of rising energy costs on the hyperscale cloud vendors has been negative but comparably modest so far. Amazon cited a 200bps impact to AWS margins in aggregate over two years, and for Microsoft we expect an impact of less than 100bps to its cloud margins this financial year, unless costs rise significantly higher. The cloud vendors are absorbing these higher costs in the near term, but we believe they possess the pricing power to share rising costs with customers over the longer term. An underappreciated point is that the energy efficiency of hyperscale data centres is far superior to what customers can achieve on their own, which is further demonstrating to these customers the advantages of being in the cloud. Cloud computing is proving its value to customers as much in this environment as it ever has, and we can see this when we delve beyond the quarterly headlines. It is why we continue to view this investment opportunity as compelling on the longer time horizon. It is an attractive, enduring, and multi-year opportunity that will deliver robust growth and attractive margins on the other side of the economic cycle we find ourselves in today. Author: Adrian Lu, Investment Analyst Sources: Company filings and Magellan estimates |

|

Funds operated by this manager: Magellan Global Fund (Hedged), Magellan Global Fund (Open Class Units) ASX:MGOC, Magellan High Conviction Fund, Magellan Infrastructure Fund, Magellan Infrastructure Fund (Unhedged), MFG Core Infrastructure Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 ('Magellan') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. A copy of the relevant PDS relating to a Magellan financial product or service may be obtained by calling +61 2 9235 4888 or by visiting www.magellangroup.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to be implemented and its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of a Magellan financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Magellan makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Magellan. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Magellan. |

21 Dec 2022 - RBA likely to move to quarterly tightening in 2023

|

RBA likely to move to quarterly tightening in 2023 Pendal December 2022 |

|

THIS week's 25-point rate rise probably won't be the last — but the Reserve Bank's pace of tightening is likely to move from monthly to quarterly increments next year. The cash rate will now sit at 3.1% for the summer. The RBA's next monetary policy statement is due on February 10. Between now and then we will see fourth quarter inflation data released on January 25. It will be high. The annual headline inflation rate will be around 8% for 2022. This will set the case for another hike in February. Tuesday's RBA statement contained nothing new. The central bank remains data dependent while the global outlook has deteriorated. Domestically the labour market remains tight. Economic growth has been strong and household spending will start to slow due to policy tightening delivered so far. For some this is yet to occur, given the higher-than-usual number of fixed-rate mortgages that are yet to reset. This is the reason why the RBA doesn't need to be as aggressive. Fixed-rate mortgages at rates around 2% will be resetting closer to 5.5% mid next year. The RBA acknowledges they are walking a tight rope. "The path to achieving the needed decline in inflation and achieving a soft landing for the economy remains a narrow one." The further they push policy, the harder the landing becomes. The RBA doesn't want to cause a recession. But given a choice of embedded higher-inflation expectations or better growth, the former wins out for any central banker. The longer-term task is no simpler. Policy action to date "has been necessary to ensure that the current period of high inflation is only temporary", the RBA statement said. "High inflation damages our economy and makes life more difficult for people." In a speech late last month RBA governor Phil Lowe pointed out that variability in inflation outcomes was more likely to increase than what we've become accustomed to. He cited four key areas where supply issues in the longer term will occur:

The RBA has under-shot or over-shot its 2-3% target band more often than not over the past 15 years. More variability in inflation outcomes? Who would want to be a central banker. Central banks have tightened policy significantly over 2022 — and that will weigh on demand over 2023. The current Christmas spendathon — where we are let loose for the first Christmas in three years — will hold activity up for now. But it's unlikely continue into the new year hangover. The supply side of the global economy is also likely to see capacity increase and downward inflationary pressure next year. The supply issues that have resulted from the pandemic and Russia's invasion of Ukraine will resolve over time. But with it comes another set of challenges. And those are more likely to be skewed towards higher inflationary pressure in the longer term. Author: Steve Campbell, Head of Cash Strategies |

|

Funds operated by this manager: Pendal Focus Australian Share Fund, Pendal Global Select Fund - Class R, Pendal Horizon Sustainable Australian Share Fund, Pendal MicroCap Opportunities Fund, Pendal Sustainable Australian Fixed Interest Fund - Class R, Regnan Global Equity Impact Solutions Fund - Class R, Regnan Credit Impact Trust Fund |

|

This information has been prepared by Pendal Fund Services Limited (PFSL) ABN 13 161 249 332, AFSL No 431426 and is current as at December 8, 2021. PFSL is the responsible entity and issuer of units in the Pendal Multi-Asset Target Return Fund (Fund) ARSN: 623 987 968. A product disclosure statement (PDS) is available for the Fund and can be obtained by calling 1300 346 821 or visiting www.pendalgroup.com. The Target Market Determination (TMD) for the Fund is available at www.pendalgroup.com/ddo. You should obtain and consider the PDS and the TMD before deciding whether to acquire, continue to hold or dispose of units in the Fund. An investment in the Fund or any of the funds referred to in this web page is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and principal invested. This information is for general purposes only, should not be considered as a comprehensive statement on any matter and should not be relied upon as such. It has been prepared without taking into account any recipient's personal objectives, financial situation or needs. Because of this, recipients should, before acting on this information, consider its appropriateness having regard to their individual objectives, financial situation and needs. This information is not to be regarded as a securities recommendation. The information may contain material provided by third parties, is given in good faith and has been derived from sources believed to be accurate as at its issue date. While such material is published with necessary permission, and while all reasonable care has been taken to ensure that the information is complete and correct, to the maximum extent permitted by law neither PFSL nor any company in the Pendal group accepts any responsibility or liability for the accuracy or completeness of this information. Performance figures are calculated in accordance with the Financial Services Council (FSC) standards. Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs. Performance data (pre-fee) is calculated by adding back management costs to the post-fee performance. Past performance is not a reliable indicator of future performance. Any projections are predictive only and should not be relied upon when making an investment decision or recommendation. Whilst we have used every effort to ensure that the assumptions on which the projections are based are reasonable, the projections may be based on incorrect assumptions or may not take into account known or unknown risks and uncertainties. The actual results may differ materially from these projections. For more information, please call Customer Relations on 1300 346 821 8am to 6pm (Sydney time) or visit our website www.pendalgroup.com |

20 Dec 2022 - The Rate Debate - 2023 predictions on the economy, inflation, and the fixed-rate mortgage cliff

|

The Rate Debate - Episode 34 2023 predictions on the economy, inflation, and the fixed-rate mortgage cliff Yarra Capital Management December 2022 The RBA delivered an eighth-straight rate hike to hit a 10-year high to round out a tumultuous 2022. Speakers: Darren Langer and Chris Rands, seasoned fixed-income specialists |

|

Funds operated by this manager: Yarra Australian Equities Fund, Yarra Emerging Leaders Fund, Yarra Enhanced Income Fund, Yarra Income Plus Fund |

19 Dec 2022 - Managers Insights | Glenmore Asset Management

|

|

||

|

Damen Purcell, COO of FundMonitors.com, speaks with Robert Gregory, Founder and Portfolio Manager at Glenmore Asset Management. The Glenmore Australian Equities Fund has a track record of 5 years and 6 months and has outperformed the ASX 200 Total Return benchmark since inception in June 2017, providing investors with an annualised return of 21.78% compared with the benchmark's return of 8.69% over the same period.

|