NEWS

11 Feb 2026 - Global Equity Outlook 2026: Earnings, Expansion, Excellence

|

Global Equity Outlook 2026: Earnings, Expansion, Excellence Alphinity Investment Management January 2026 3 minutes read time |

|

As we enter 2026, global equity markets are poised for the next phase of expansion. After a year defined by policy disruption, technological revolution, and geopolitical uncertainty, investors are rightly questioning whether the narrow leadership and momentum-driven returns of recent years can continue. Our view is that 2026 represents an evolution in market dynamics: from surviving tension to capitalising on expansion, from chasing narratives to backing earnings, and from speculative fervour to quality compounding. If 2025 was the year of "Tariffs, Tech, and Tension," we believe 2026 will be remembered as the year of "Earnings, Expansion, and Excellence. Reflecting on 2025: Tariffs, Tech, Tension Judging by the opening weeks of 2026, elements of these three T's appear determined to follow us into the new year. Investors should remember last year's lesson: even in strong years, significant volatility is inevitable. The key is maintaining discipline through the swings rather than reacting to them. EARNINGS: A Constructive Global Cycle Broadens Earnings sentiment (diffusion ratio) at a 4-year high with a positive inflection across major regions

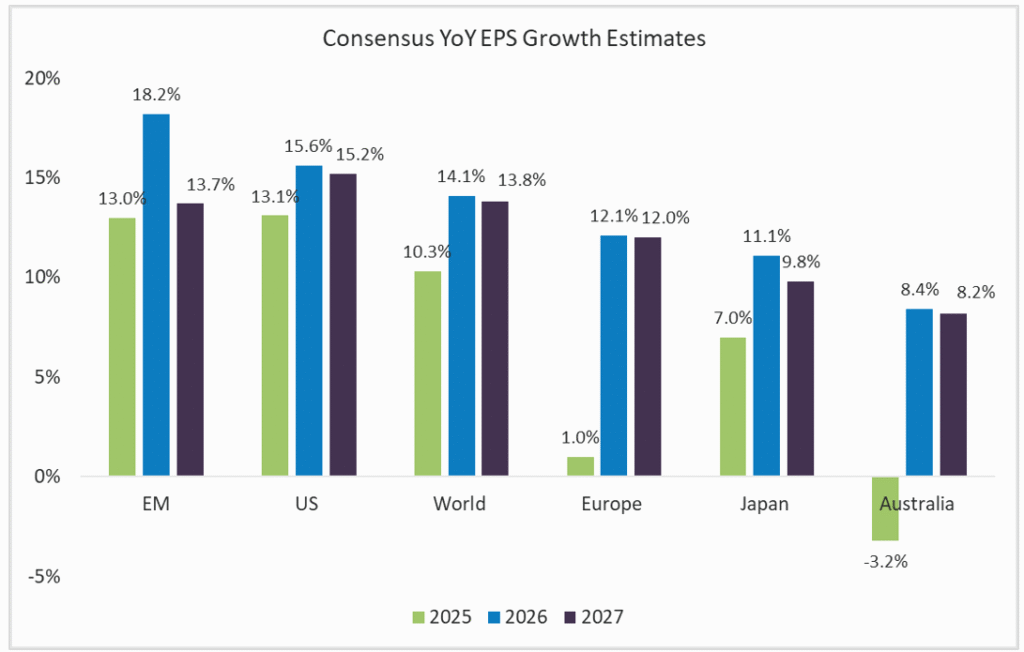

Source: Alphinity, Bloomberg, 31 December 2025 Technology and Financials continue to lead earnings growth revisions, though they have recently been joined by Materials as higher commodity prices flow through to corporate results. Healthcare, Industrials, and Consumer sectors still lag but are showing signs of stabilisation. Consensus now expects the MSCI World index to deliver healthy double-digit EPS growth of approximately 14.1% in 2026 and 13.8% in 2027. Most major markets are projected to see a rebound in earnings growth over this period, with current laggards like China and Europe positioned to catch up. This broadening earnings picture supports higher equity valuations and reduces the concentration risk that has concerned many investors. Early signs from the 4Q25 reporting season suggest the earnings trajectory remains strong, though market reactions are more subdued as elevated valuations raise the bar for positive surprises. If companies deliver the usual 4-5% beat, this will mark a fifth straight quarter of double-digit earnings growth--a streak not seen since late 2018. Consensus expects strong earnings growth across all key regions in 2026 and 2027

Source: Bloomberg, 12 January 2026 We remain relatively constructive on the outlook for corporate earnings in 2026, which we expect to be supported by generally favourable macroeconomic conditions. Importantly, these supportive conditions are not dependent on a single driver but reflect expansion across multiple fronts. EXPANSION: Multiple Tailwinds Converge

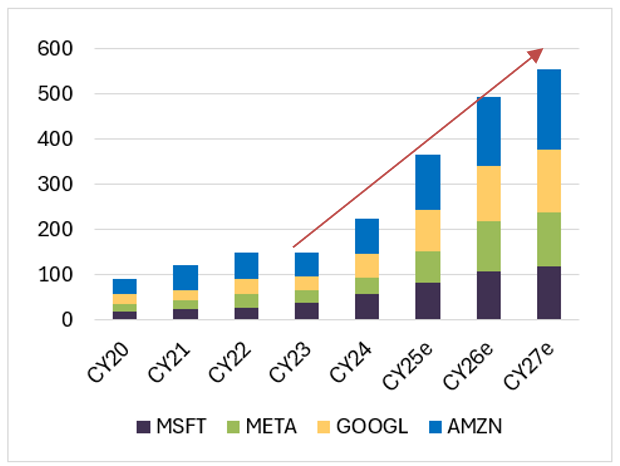

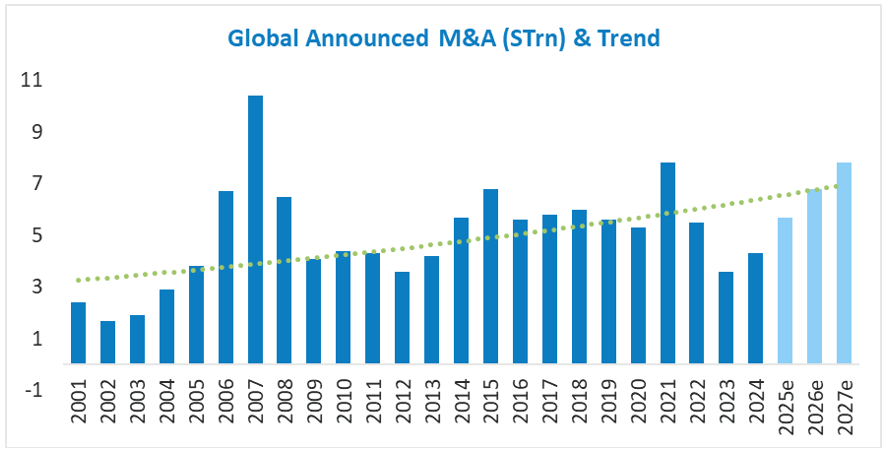

Source: Alphinity, Factset, 31 December 2025 Consumer fundamentals remain surprisingly robust despite increasing bifurcation. Unemployment sits near historic lows across developed markets, real wage growth persists, and household balance sheets are healthy following pandemic-era deleveraging. The emerging K-shaped pattern--with upper-income households benefiting from wealth effects while lower-income consumers face pressure--creates divergent retail dynamics but hasn't derailed aggregate spending. With consumption representing 70% of US GDP, this resilience provides a critical foundation for corporate earnings. Mergers and acquisitions rebounded sharply in 2025 after hitting 20-year lows in 2023. The catalysts driving this resurgence, lower rates, open capital markets, improving corporate confidence, and more favourable regulation, remain firmly in place. Companies are no longer waiting on the sidelines as they pursue growth and technology capabilities through strategic transactions. Deal activity is forecasted to reach $6.8 trillion in 2026 and $7.8 trillion in 2027*, supported by private markets industry sitting on $4.2 trillion of dry powder (approximately $8 trillion of buying power with leverage), the stage is set for sustained M&A momentum. Across our portfolios, serial acquirers like Amphenol, Parker Hannifin, Motorola Solutions, and CRH continued adding value through disciplined consolidation strategies, while investment banks JPMorgan and Morgan Stanley benefit from elevated advisory and underwriting activity.

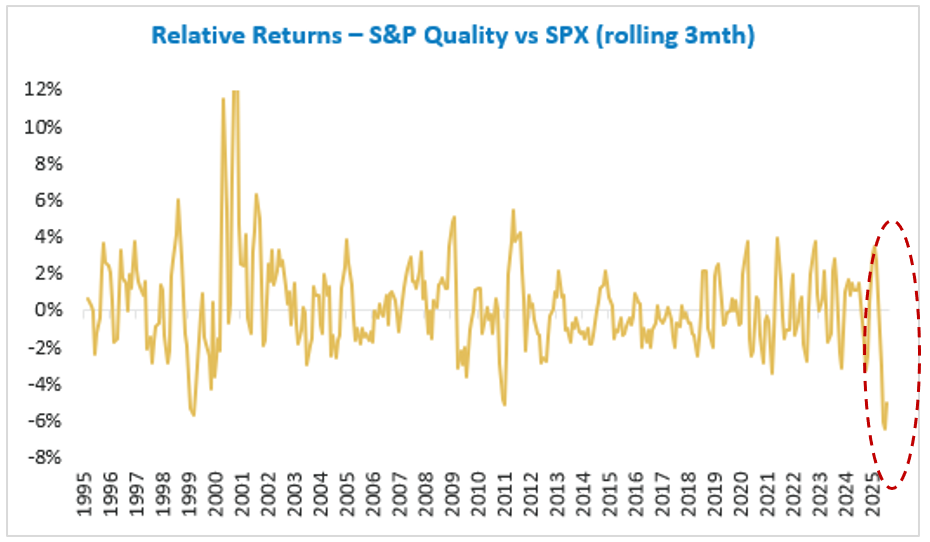

Source: *Morgan Stanley Research, Dealogic, 31 December 2025 EXCELLENCE: Quality's Overdue Mean Reversion Sector dynamics compounded the challenge. Quality indices traditionally overweight Consumer Staples and Healthcare--both facing significant idiosyncratic headwinds--while underweighting Banks, which strongly outperformed. Elevated valuations, particularly in Europe, and speculative retail activity added further pressure. AI disruption concerns also weighed on Software, Diversified Financials, and Business Services, all typical quality portfolio constituents. However, conditions now favour mean reversion. Relative valuations between quality and lower-quality stocks have normalized. Sector-specific headwinds are easing. Most importantly, as geopolitical and policy volatility persists, investors are increasingly valuing downside protection. Quality companies--those with sustainable competitive advantages, pricing power, and capable management teams with proven capital allocation track records--are better positioned to navigate uncertainty and deliver consistent returns. In an environment where fundamental differentiation matters again, excellence in business quality should separate winners from pretenders. Quality as a factor had its worst year in decades during 2025

Source: S&P, 31 December 2025 Positioning for 2026 AI and Technology: We maintain selective exposure across the value chain, balancing opportunity with execution risk. Our Magnificent Seven exposure include Nvidia and Microsoft for their AI leadership and supportive valuations. Beyond mega-cap tech, TSMC offers dominant semiconductor positioning with fortress balance sheet strength, Tencent combines gaming and cloud growth with exceptional cash generation, and Amphenol provides mission-critical connectivity solutions with high switching costs. We remain thoughtful about position sizes given the technology's rapid evolution, uncertain ROI timelines for hyperscalers, and disruption risks to incumbent business models. Financials: Global banks represent our primary cyclical exposure, benefiting from sustained net interest margins, robust capital return programs, and improving loan growth. JPMorgan and Morgan Stanley provide diversified financial services leadership, while NatWest and Caixa Bank offer compelling regional banking franchises in the UK and Spain respectively. Healthcare, Industrials, and Quality Defensives: Boston Scientific and AstraZeneca deliver healthcare exposure through innovation pipelines and R&D productivity. Caterpillar captures industrial recovery with pricing power and durable service revenue. Defensive positions in Coca Cola and L'Oreal (Consumer Staples) offer global scale and solid organic growth. Cyclicals such as CBRE (Real Estate) and CRH (Materials) provide quality characteristics and established competitive moats. This positioning reflects our conviction that 2026 favours portfolios combining secular growth exposure with business quality--companies that can compound earnings through volatility rather than merely benefit from beta. A diversified portfolio of earnings leaders

Source: Alphinity, 31 December 2025 *Select portfolio holdings. Conclusion The "free money" period for low-quality momentum plays appears to be ending. While volatility and policy uncertainty will undoubtedly persist, portfolios that combine exposure to secular growth trends with an emphasis on earnings certainty, balance sheet strength, and management excellence are well-positioned to deliver superior risk-adjusted returns. For investors willing to look beyond the narrow leadership that dominated recent years, 2026 offers compelling opportunities across a broadening set of quality businesses with genuine earnings power. |

|

Funds operated by this manager: Alphinity Australian Share Fund , Alphinity Concentrated Australian Share Fund , Alphinity Sustainable Share Fund , Alphinity Global Equity Fund , Alphinity Global Sustainable Equity Fund This material has been prepared by Alphinity Investment Management ABN 12 140 833 709 AFSL 356 895 (Alphinity). It is general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Any projections are based on assumptions which we believe are reasonable but are subject to change and should not be relied upon. Past performance is not a reliable indicator of future performance. Neither any particular rate of return nor capital invested are guaranteed. |

10 Feb 2026 - Performance Report: Bennelong Concentrated Australian Equities Fund

[Current Manager Report if available]

9 Feb 2026 - Performance Report: ASCF High Yield Fund

[Current Manager Report if available]

9 Feb 2026 - Performance Report: Quay Global Real Estate Fund (Unhedged)

[Current Manager Report if available]

9 Feb 2026 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

9 Feb 2026 - Australian Secure Capital Fund - Market Update

|

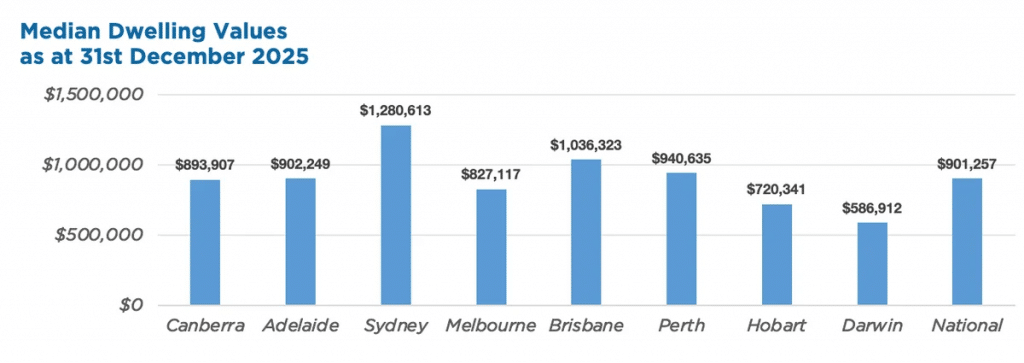

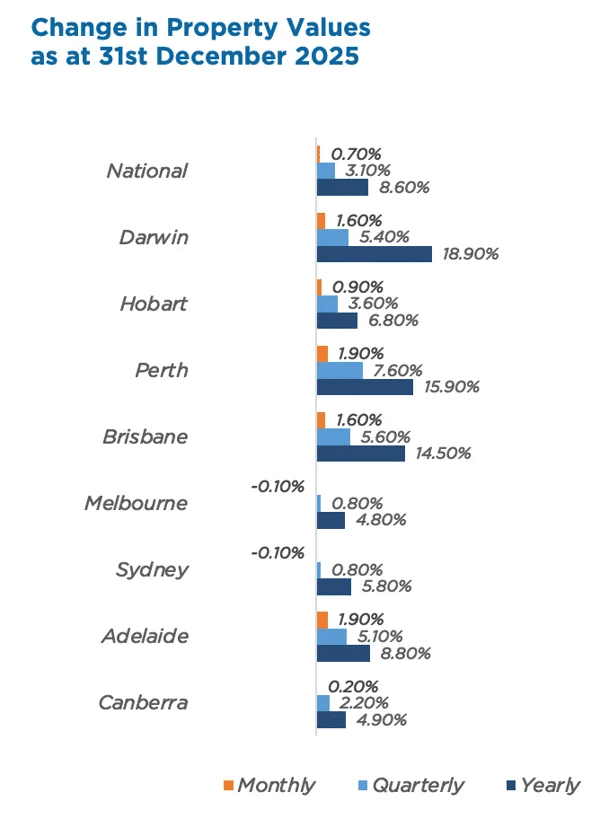

Australian Secure Capital Fund - Market Update Australian Secure Capital Fund January 2026 December saw the smallest national pricing gain in five months, rising by just 0.7%. Values in Melbourne and Sydney declining by 0.1% dragged this figure down. In contrast, Brisbane, Adelaide, Perth, and Darwin all saw increases of 1.6% or higher. More broadly, the Australian housing market finished 2025 strongly, with the national median dwelling value surging 8.6% over the year--the most since 2021. Regional markets outperformed capital cities with a 9.7% annual rise, compared to 8.2% for the capitals. In 2026, while economic uncertainty and affordability may temper the pace of growth, a persistent shortage of new housing supply should act as a floor for property values, protecting against significant price drops.

January Edition Funds operated by this manager: ASCF Select Income Fund , ASCF High Yield Fund , ASCF Premium Capital Fund , ASCF Private Fund

|

6 Feb 2026 - Hedge Clippings |06 February 2026

|

|

|

|

Hedge Clippings | 06 February 2026 Tuesday's rate increase by the RBA of 0.25% to 3.85% was well telegraphed by market expectations leading up to the meeting, thanks to December's annual inflation number jumping to 3.6%, even though those same market expectations had been for a reduction in inflation prior to the number being released. One could cynically assume that the market is no better at forecasting the movement of either inflation or the cash rate than the RBA itself. What is also clear, albeit with the benefit of hindsight, is that the RBA should not have cut rates three times in 2025, and even when they did so for the third time in August, the market - particularly the big four banks, but also practically every other noted economist - should not have jumped on the bandwagon and forecast a further 2 or 3 reductions by mid to late 2026. Seed Fund Management's Nick Chaplin and Renny Ellis from Arculus Funds Management have both been arguing against last year's cuts from the RBA, and the banks' forecasts, every time we met with them over the past year, but without the benefit of hindsight. We caught up with Nick and Renny immediately after Michele Bullock's media presentation on Tuesday, (see video link below) and they were adamant (again, without the benefit of hindsight) that the RBA had got it wrong, including the view that the first cut in February, in the lead-up to a federal election, was unwise. That was followed by a further cut in May, and under intense pressure from the media and Treasurer, again in August, even though the inflation outlook at that time was questionable, thanks to multiple government energy rebates. For a homeowner with a mortgage, you've just got to suck it up and take the view that at least you had 6 to 12 months of reduced payments before your repayments went back up again. Shame about the budget planning though! Now those same budget plans are having to factor in the market expectations for two or possibly three further rate rises this year, in place of the two reductions expected just 3 months ago, so in effect a reversal of over 1%. However, the RBA is not alone. Rates are expected to remain unchanged in the Euro area over the remainder of 2026, and possibly increase in Japan and New Zealand. The US is, of course, the outlier, in that it could go either way, once Powell has been replaced by Trump's nominee in May. One would expect whoever Trump had nominated would do his bidding, but there are suggestions that Kevin Warsh may hold the line on the Fed's independence. News | Insights Expert Analysis of the RBA's February 03 Rate Decision Global Matters: 2026 Outlook | 4D Infrastructure Quarterly State of Trend report - Q4 2025 | East Coast Capital Management January 2026 Performance News Quay Global Real Estate Fund (Unhedged) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

6 Feb 2026 - 2026: A Year of Calm Before the Market Storm?

|

2026: A Year of Calm Before the Market Storm? JCB Jamieson Coote Bonds January 2026 (3-minute read) Top of mind this summer, more so than any other recent summer, is the extent to which the recent remarkable streak of performance across almost all asset classes powers ahead, or loses momentum. As we enter 2026, markets are tinder-dry with risk, and for now the winds are calm. Since last month, global markets have seemingly settled into a tranquil yet uneasy holding pattern, having made considerable progress to date in navigating the turbulence presented by tariffs, policy uncertainty, geopolitical travails, and stagflation. What might occur in the year ahead to potentially ignite a sparkcould it be another policy surprise from the U.S. Administration, geopolitical tensions, or macroeconomic developments? Let's map out and break down the key risks that might cast a long shadow over current pricing in global markets. In the U.S., markets appear to be much less responsive than usual to surprises in economic data after the U.S. Federal Government shutdown late last year. This stands to reason the U.S. Administration has challenged the independence of not only the U.S. Federal Reserve, but ostensibly also the civil servants at the Bureau of Labor Statistics and the Bureau of Economic Activity who produce the data releases. Some believe, and there is very little evidence that contradicts their view, that President Trump intends to do what he sees as necessary to frame the macro outlook and asset price dynamics in the best possible light for the Grand Old Party ahead of this year's midterm elections. In China, authorities have held back on announcing significant fiscal stimulus, instead preferring to outmaneuver the U.S. on trade and foreign policy, particularly with respect to rare earths supply. All the while President Xi has tirelessly advanced China's economic and strategic interests, most recently allowing the renminbi to reach its strongest level against the U.S. dollar in the past several years, and applying ever-increasing pressure on Taiwan's independence (given its semiconductor fabrication infrastructure after the U.S. set a dangerous precedent in Venezuela, which has the world's largest oil reserves). In Japan, Prime Minister Sanae Takaichi has just called snap elections in an effort to shore up support for planned fiscal stimulus and policy support intended to ease the cost of living. However, she must also contend with a lack of macro policy coordination with yen weakness; a reticence from the Bank of Japan to continue tightening policy and preserve its "virtuous cycle" between activity, wages and prices; and ceaselessly rising Japanese government bond yields. This is a potent combination that also indirectly led to the downfall of the Prime Minister's predecessor, Shigeru Ishiba. And these thematic patterns are repeated in kind throughout Europe, Canada and the UK: unsteady political leadership, complex macro and broader policy challenges, and the fragmentation of the regional and international order via superficial cooperation amid divergent national interests. All the while, risk assets are priced for continuing material gains, and valuations are stretched to record levels, whilst central banks globally are making marginal adjustments to gradually recalibrate policy towards the elusive, ever-shifting mirage of neutrality loosening here, tightening there all second order given the macro backdrop described above. When could valuations adjust and risk potentially be adjusted or even repriced? It is the critical question we are all focused on this year in global markets. Pricing may well continue its onward march higher this year, but after a period of such impressive asset market performance, history would suggest the largest gains are behind us. Coupled with the possibility of complacency amongst market participants who have become accustomed to outsized gains in recent times, this sets the stage for an interesting and eventful year ahead and does create opportunities for those prepared to question the current consensus that underpins market pricing. Funds operated by this manager: CC Jamieson Coote Bonds Active Bond Fund (Class A) , CC Jamieson Coote Bonds Dynamic Alpha Fund |

5 Feb 2026 - Expert Analysis of the RBA's February 03 Rate Decision

|

Expert Analysis of the RBA's February 03 Rate Decision FundMonitors.com February 2026 |

|

Chris Gosselin, CEO of FundMonitors.com, speaks with Nicholas Chaplin, Director and Portfolio Manager at Seed Funds Management, and Renny Ellis, Director & Head of Portfolio Management at Arculus Funds Management. The discussion examines the Reserve Bank of Australia's latest rate hike, with both guests arguing the RBA misjudged conditions by cutting rates last year and is now reacting too heavily to short-term data. They highlight the role of policy lags, the strengthening Australian dollar, and bond market signals, warning that further tightening risks overshooting and undermining economic stability. |

5 Feb 2026 - Emerging markets outlook (and drinking tea) in 2026

|

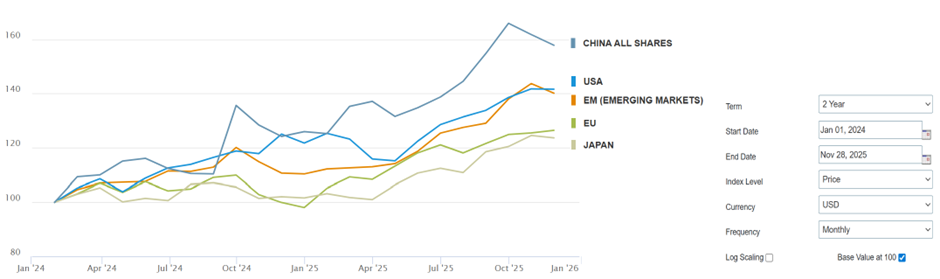

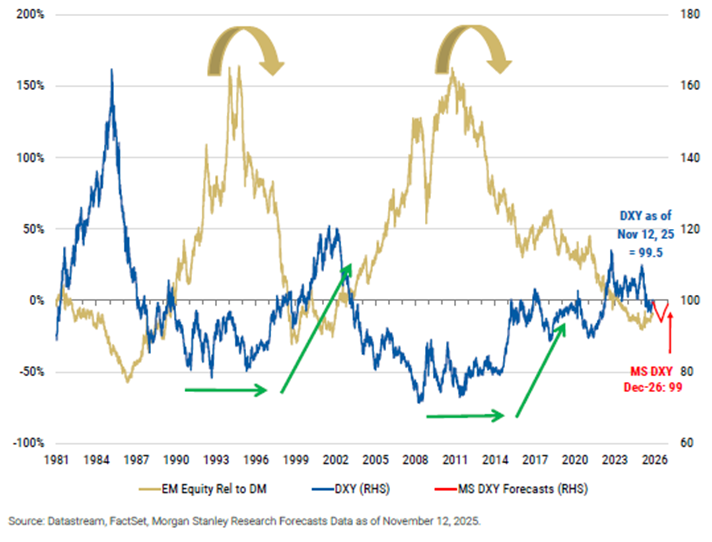

2025 EM Outlook: Reading the tea leaves Ox Capital (Fidante Partners) January 2026 (15-minute read) Investing is like boiling a kettle. When the kettle is hot, one can get burnt. In the investing world, it doesn't always pay to chase what is hot. When an economy is running hot, central banks will need to hike interest rates to ensure inflation stays under control. When an investment theme is "hot", its future potential is rapidly priced in by investors. In comparison, when the kettle is warming up, one has time to set up the tea set, watch the kettle boil, take a moment to brew the tea to hit its full flavour, and finally sit back and enjoy. EM equities have been "cold" for over a decade, but the kettle is finally warming up. Between Jan-24 and Nov-25, EM equities performed just as well as US equities. In particular, the Chinese equity market, which was considered "uninvestible" by some funds, has outperformed the US, Europe, and Japan markets over the same period. Figure 1: Chinese equity performance overtook key DMs in 2025

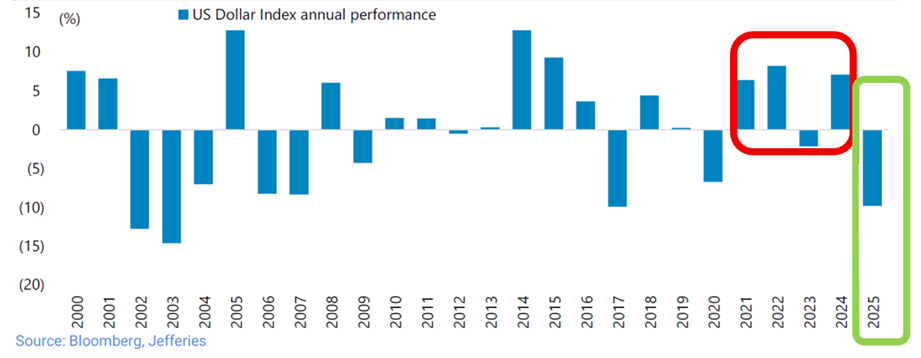

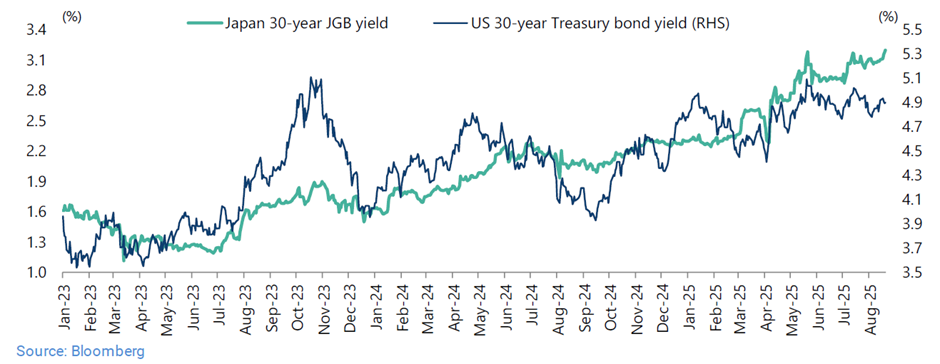

Source: MSCI.Developed markets have been running too "hot" In 2026, the "hot" developed markets (DMs) will have their share of challenges. Many developed economies have been running "hot" for some years propelled mostly by debt accumulation and rising asset prices. Since the pandemic, most developed economies have added debt to fund deficit spending for the maintenance of living standards. Politicians have often picked the easy option of further spending rather than reining in budget deficits. Global markets are starting to contemplate these latent risks. The weakening US dollar (USD), surging gold prices, and rising bond yields in the US and Japan (now over 3% for 30-year Japanese Government Bonds) are perhaps foretelling the problems ahead. Figure 2: USD weakening of 2025

Source: Bloomberg, Jefferies.

Figure 3: The gold price has rallied nearly 60% YTD at time of writing

Source: Goldprice.org.

Figure 4: Rising 30-year bond yields in the US and Japan

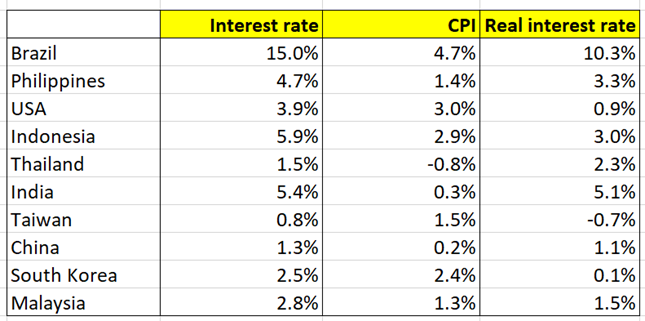

Source: Bloomberg.A changing geopolitical landscape and global alliances deepen the challenge ahead, as countries are also compelled to fund new defence spending. To fund this ever-growing government debt, it is likely that major DM central banks will loosen monetary policy (i.e. cut rates or even pursue QE in some form) in the face of moderately high inflation rates. Emerging markets are only "warming up" in 2025EM countries have better economic and demographic foundations than most of the developed world. Most EM governments have managed their finances responsibly. Consider Malaysia, which is actively pursuing fiscal reform, and Indonesia, which under President Joko Widodo has improved in leaps and bounds. Meanwhile, the Chinese and Vietnamese governments have both made tough decisions to keep their property markets in check. Having learnt their lessons from previous debt crisis, EM governments have worked hard to keep fiscal deficits under control, while still pursuing effective pro-development agendas. Even through COVID, they refrained from large government handouts. EM central banks broadly have no hesitation pushing interest rates higher to support domestic currencies and keep inflation in check where needed, even as many of the DM central banks' have begun new easing cycles. Case in point in monetary policy responsibility is Brazil, where the central bank has kept interest rates at 15% despite inflation running at a much lower 4-5%! As governments remain sensible in EM, many countries in EM have reasonable real interest rates (>3%). That is, there can be more monetary policy easing to come, supporting economic growth and equity markets in many EMs. Figure 5: Brazil, Indonesia, Philippines and India have high real rates of over 3%

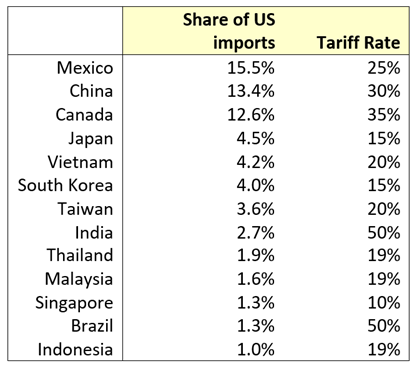

Source: Trading Economics.2025 can be best characterised as a year of "de-risking" across EM. By and large, EM economies have emerged unscathed from US tariff negotiations. The final tariffs were largely between 10-20% in Asia, much lower than the initial "targets". This left the relative competitiveness of these Asian EM export nations unscathed. Two EM countries which were singled out by the US were Brazil and India. However, exports to the US from India and Brazil only account for a small percentage of GDP (≈2%), and likely any loss in volumes from the US can be taken up by other trading partners. Finally, China and the US agreed to a trade truce in November 2025, meaning trade and key external risks are settled for now, and we expect this to remain at least through 2026. Figure 6: Key Asian nations we invest in remain highly competitive exporters, despite new tariffs imposed by the US

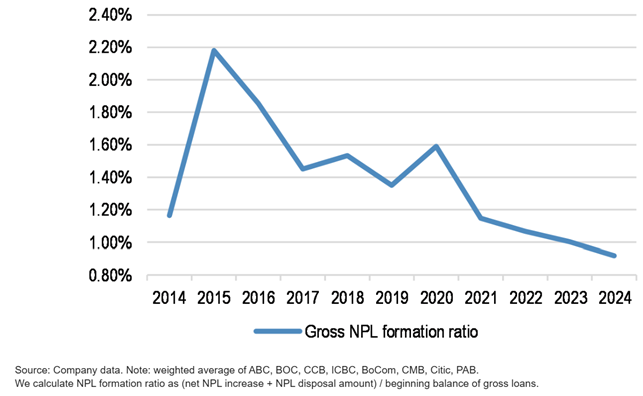

Source : Ox Capital research.In China, it has been four years since the property market peaked. Property prices have declined as much as 30 to 40% in most cities. Several large private property developers have defaulted and been liquidated. Notably, the banking system has negotiated its way through the property market downturn well, with bad debt formation for Chinese banks trending down since 2021. With the banking system intact, China is NOT Japan. The country is only working through a cyclical property market downturn, and it is at the later stage of this adjustment. We expect property prices to bottom in late 2026 / early 2027. Figure 7: NPL formation in China is showing a healthy decline and banks' balance sheets are resilient

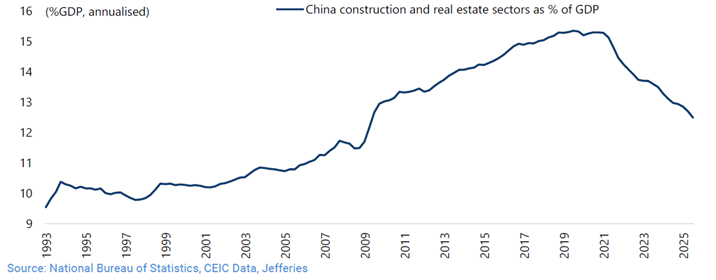

Source: JPMorgan.What is often less mentioned is the transformation of the Chinese economy. The construction and real estate sectors have shrunk as percentage of GDP. Figure 8: The construction and real estate sectors peaked at just over 15% of Chinese GDP in 2019, and are now around 12% of GDP

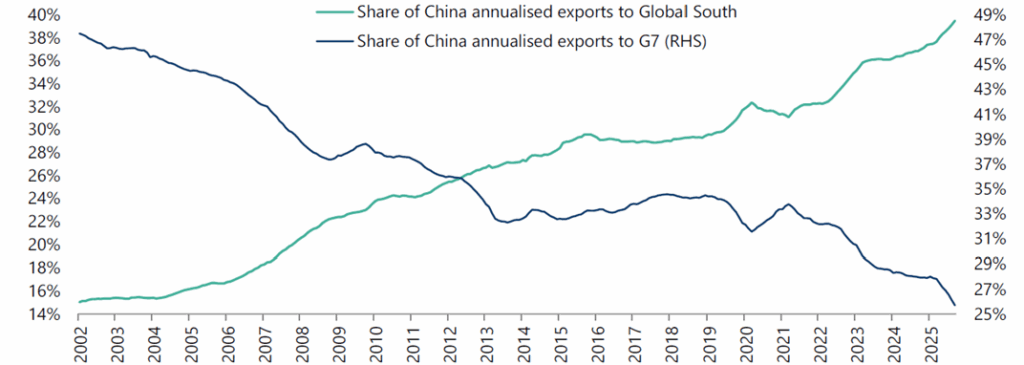

Source: Jefferies.Despite this, the Chinese economy still managed to grow ~5% p.a. between 2021 to 2025. The shortfall in growth coming from the slowing real estate and construction sectors was made up by the export and industrial sectors. Since the first Trump administration, China has been developing other export markets. Between 2021 to 2025, we can see the rise of Chinese exports to the Global South (ASEAN, Latin America, Africa, India, Pakistan, Saudi Arabia, UAE and Turkey), which have been able to offset falling exports to G7 nations. Figure 9: G7 nations are no longer the top end markets for Chinese exports

Source: Jefferies, CEIC Data, General Administration of Customs.Its growth potential is further bolstered by the rise of new and innovative industries. These days, China is the leading producer of solar and wind energy equipment. In 2023, it overtook Japan as the largest auto exporting country, and it is today leading the world in the transition to electric vehicles (EVs). While China is now having success in various industrial and manufacturing end markets, for a time there was a fear that US sanctions could hold back China in the technology race by restricting access to semiconductor technology. Instead of becoming stifled, China has made it a national priority to develop domestic semiconductor know-how. In some product segments, the domestic suppliers are finally good enough to be considered as replacements for foreign imports. After semiconductors, the next front was AI. Again, China has shown that it is firmly in the race after the unveiling of DeepSeek in January 2025. Chinese AI companies, along with the open source community, can innovate and are often much more cost effective than the well-known hyperscalers. In summary, EM economies are resilient and capable of withstanding external pressures. Emerging markets are "heating up" in 2026There are multiple catalysts on the horizon. We are optimistic on EM in 2026: The weak USD:As a rule of thumb, a weak USD is a tailwind for EM. Central banks in EM economies need to consider the impact on their currencies in their rate cut decisions. Hence, a weak USD affords EM economies greater flexibility, with inflation largely under control. A key event to watch next year is the appointment of the new US Federal Reserve Chairman, as Jerome Powell's term will expire in May 2026. If the new Federal Reserve looks to quickly cut rates to support the economy, there will be greater downwards pressure on the USD.

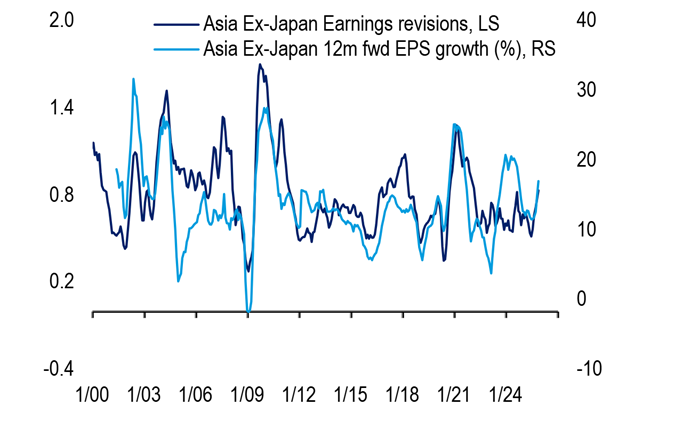

Source: Morgan Stanley.Anything-but-AI:AI has been the focus of investors for over two years now. Many traditional non-technology stocks have been left behind and de-rated. At some point in the future, momentum behind AI spending will inevitably slow. Hence, investors will need to look for the "anything-but-AI" investment. EM, in particular Asian equities, can be a fertile hunting ground for new ideas. Earnings are expected to grow strongly (17% YoY) in 2026 in Asia ex-Japan. Figure 11: Asia ex-Japan forward earnings growth forecasts are strong and expected to stay high in 2026

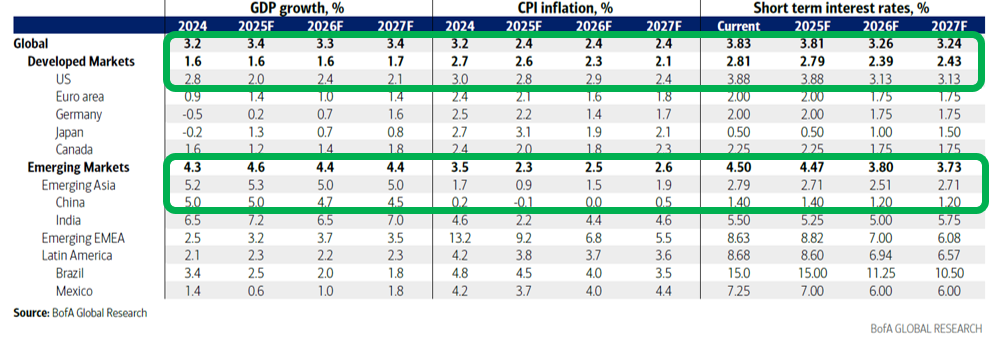

Source: BofA, MSCI, FactSet.EM macro is better:In 2026, EMs are expected to grow faster than DMs (4.4% vs. 1.6%, respectively). Low inflation and high real interest rates suggest further room for multiple rate cuts in many EM economies. An important catalyst to watch out for is new stimulus policies in China in 2026. Most investors are not expecting much on this front. There will be upside if and when the Chinese government delivers on these measures in 2026. Figure 12: GDP growth for EMs in Asia is higher than DMs in 2026

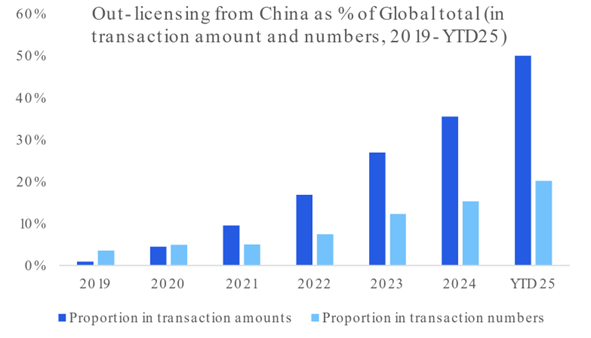

Source: BofA.Value-up/shareholder return:In 2025, we saw the rise of value-up programs emphasising minority rights in Asia. This is something we have not seen much of in our time investing in Asia. Korea, which drew attention from global investors with its value-up program, was one of the best performing markets in EM in 2025. Other countries are taking notice. Indonesia set up its sovereign wealth fund (Danantara) in February 2025. Danantara is pushing state-owned enterprises to improve return on equity, and provide better shareholder returns. Elsewhere, the Singaporean government is investing $5bn with fund managers under its market development program to improve the liquidity of small and mid-caps in Singapore. These initiatives can be rewarded more strongly as execution begins to come through. Sunrise industries:The US/China rivalry is leading to the rapid growth of many "sunrise" industries (and stocks) in China. China is looking to promote and create domestic champions to reduce its reliance on US suppliers. We are particularly encouraged by the strong returns seen in the Chinese biotech space in 2025 as investors have begun to wake up to their potential. Almost 50% of global drug licensing deals in 2025 were sourced from China. Outside of biotech companies, many of the emerging leaders in fields such as robotics, medical device, AI, SaaS, autonomous driving, LIDAR, semiconductor and fintech, for example, are listed and poised to deliver sharply accelerating growth in 2026 and beyond. Many of these companies are looking to expand globally. There are just as many exciting thematic ideas in EM as on the Nasdaq. Figure 13: China is beginning to dominate global drug licensing with its innovative companies

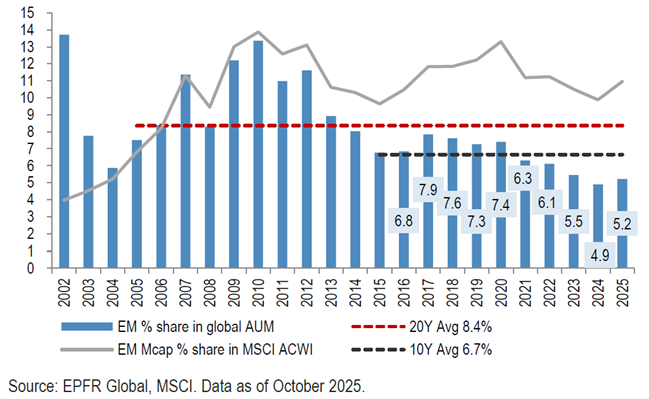

Source: Citi Research.Stronger shareholders in EM:EM equities are in stronger hands and better supported than in years past, making them less susceptible to global fund flows. While mainland capital used to only make up 10 to 15% of turnover in Hong Kong, Chinese investors have now displaced global funds as the key investor, regularly accounting for two to three times this volume today, at 25 to 30% of daily turnover. In addition, another nice surprise for us, compared to years past, is the fact that we are seeing Chinese companies buying back their stocks aggressively. Some companies have shareholder return targets of as much as 10 to 15% a year. Similarly, the Indian stock market is well supported by local investors (through their regular saving plans). The Indian market has been resilient despite foreigners reducing their positions throughout 2025. Time to sit back and enjoy the teaSince COVID and the Russian invasion of Ukraine, the world has been in a state of flux. The Trump administration has been working to re-cast the global order. Despite this, China has withstood and successfully countered challenges and a trade war with the US. Its local economy has proven sceptics wrong, and despite property prices being crunched in a bid by the Chinese government to reduce systematic risk, the banking system has hardly missed a beat. Outside of China, governments in EM are sticking to orthodox economics, by keeping budget deficits low, maintaining stable domestic currencies, with central banks fighting to keep inflation in check. Just like any good tea, it will take time to brew. Despite a favourable macroeconomic backdrop, global investors are only lightly positioned in EM, well below the historical average. Figure 14: EM positioning by global investors can pick up a long way from here |