NEWS

10k Words | May 2026

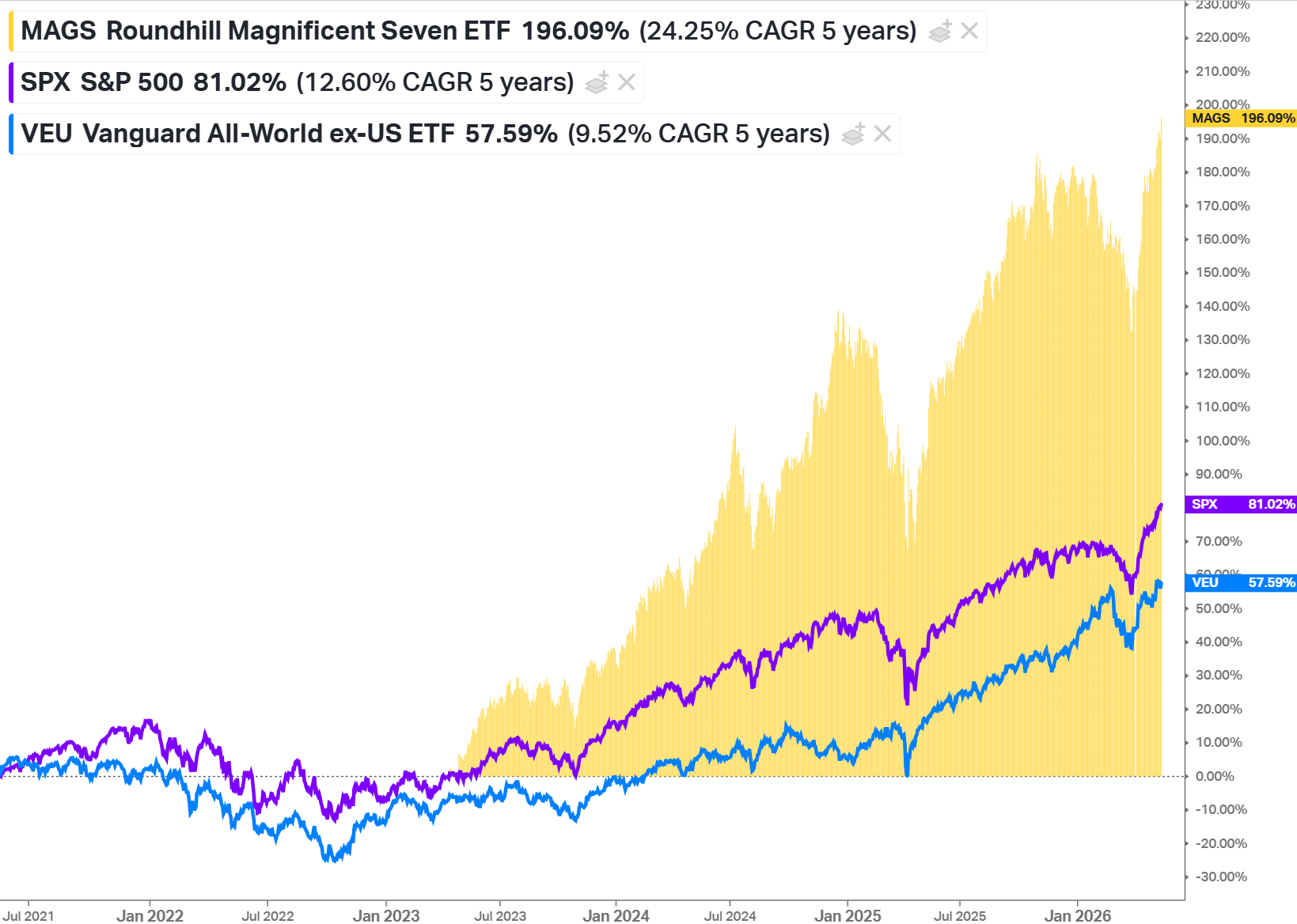

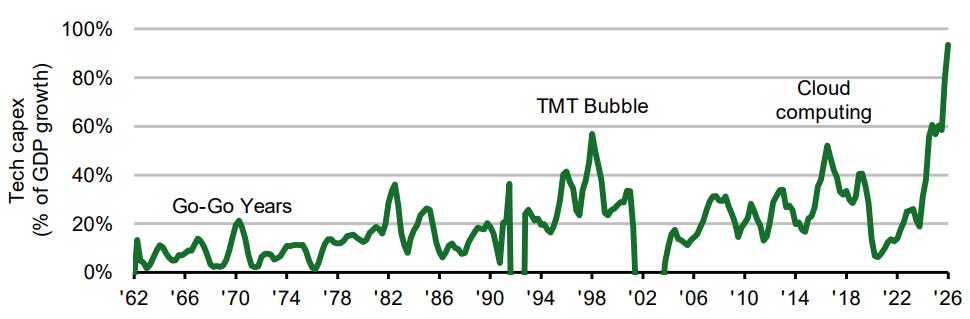

The "Magnficient 7" continue to lead the charge with investors exhibiting a strong appetite for risk. (2-minute read)

Read more...

Performance Report: Altor AltFi Income Fund

The Altor AltFi Income Fund rose by +0.86% in April, outperforming the RBA Cash Rate + 5% benchmark by +0.11%. Since its inception in April 2018, the fund has returned +11.51% per annum, an outperformance of +4.40% relative to the...

Read more...

Hedge Clippings |22 May 2026

The 2026 Budget may come to be remembered less for its promised "fairness" than for the investment shock it has unleashed.

Labor's changes to negative gearing and capital gains tax are being sold as a rebalance in favour of...

Read more...

Performance Report: Bennelong Concentrated Australian Equities Fund

The Bennelong Concentrated Australian Equities Fund rose by +3.64% in April, outperforming the ASX 200 Total Return benchmark by +1.46%. Since its inception in February 2009, the fund has returned +9.89% per annum, an outperformance of...

Read more...

Global Perspectives: Addressing the most essential questions around AI

In this episode, Portfolio Manager Denny Fish takes a deep dive into the current state of artificial intelligence (AI), including the latest advancements, its potential to propel economic growth, and the rise of agentic AI and its impact...

Read more...

Performance Report: DAFM Digital Income Fund (Digital Income Class)

The DAFM Digital Income Fund (Digital Income Class) rose by +0.01% in April. Since its inception in May 2021, the fund has returned +20.31% per annum, an outperformance of +14.37% relative to the RBA Cash Rate + 3% benchmark, which has...

Read more...

Who's winning the AI race - and does it matter?

In this episode, we explore how artificial intelligence (AI) is reshaping global competition. (Duration: 27 Mins)

Read more...

Performance Report: Cyan C3G Fund

The Cyan C3G Fund rose by +1.00% in April. Since its inception in August 2014, in the months where the market was positive, the fund has provided positive returns 77% of the time.

Read more...

Glenmore Asset Management - Market Commentary

The US market appeared to shrug off the ongoing war in Iran,

reaching new highs during April. (2-minute read)

reaching new highs during April. (2-minute read)

Read more...

Performance Report: ECCM Systematic Trend Fund

The ECCM Systematic Trend Fund rose by +4.47% in April, an outperformance of +1.62% compared with the SG Trend benchmark, which rose by +2.85%. Since its inception in January 2020, the fund has returned +14.74% per annum, a difference of...

Read more...