NEWS

12 May 2026 - Prediction Markets: The next big disruption in investing?

11 May 2026 - Performance Report: Seed Funds Management Financial Income Fund

[Current Manager Report if available]

11 May 2026 - Performance Report: Quay Global Real Estate Fund (Unhedged) Active ETF (ASX:QGRU)

[Current Manager Report if available]

11 May 2026 - Performance Report: Bennelong Twenty20 Australian Equities Fund

[Current Manager Report if available]

11 May 2026 - 10k Words | April 2026

|

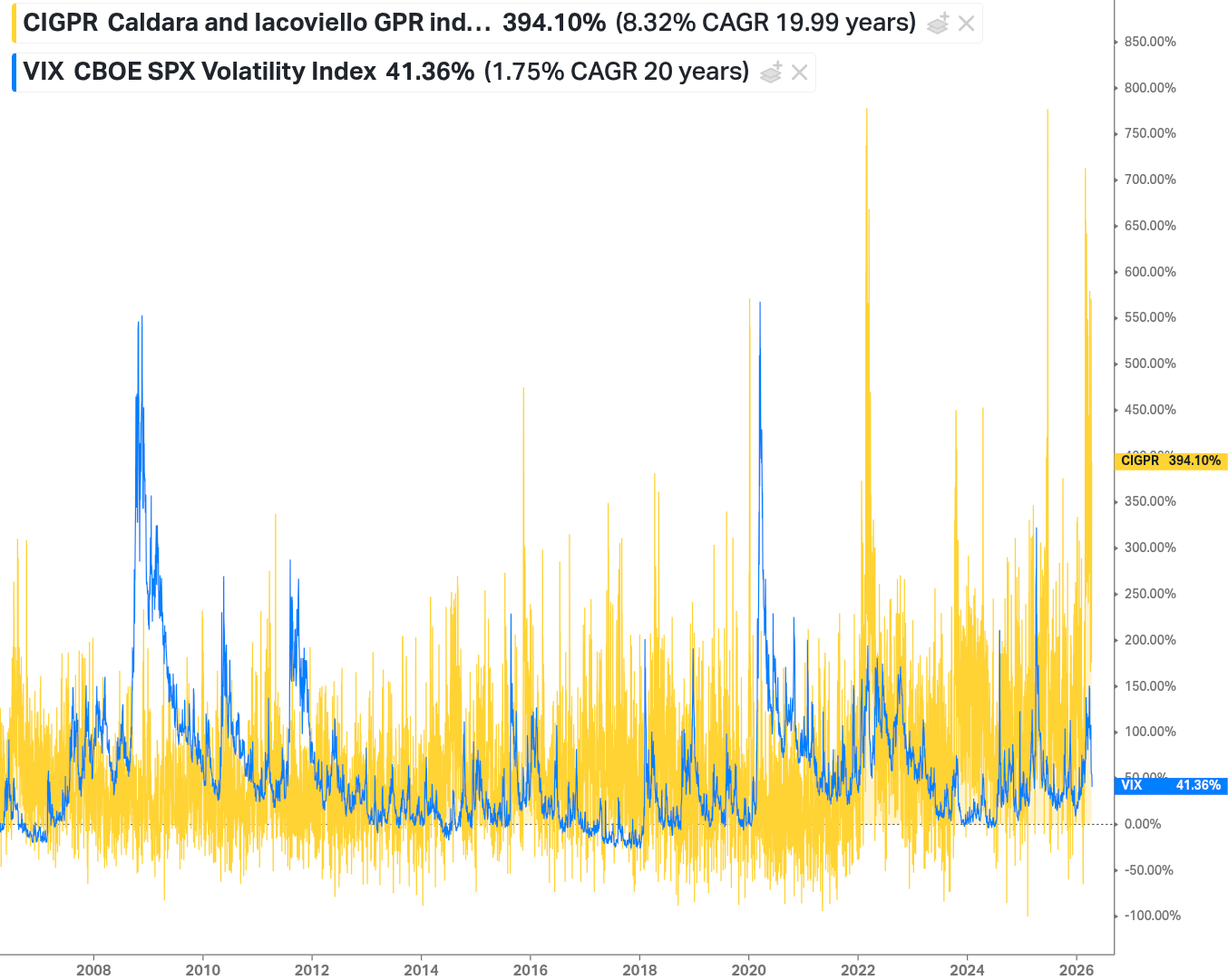

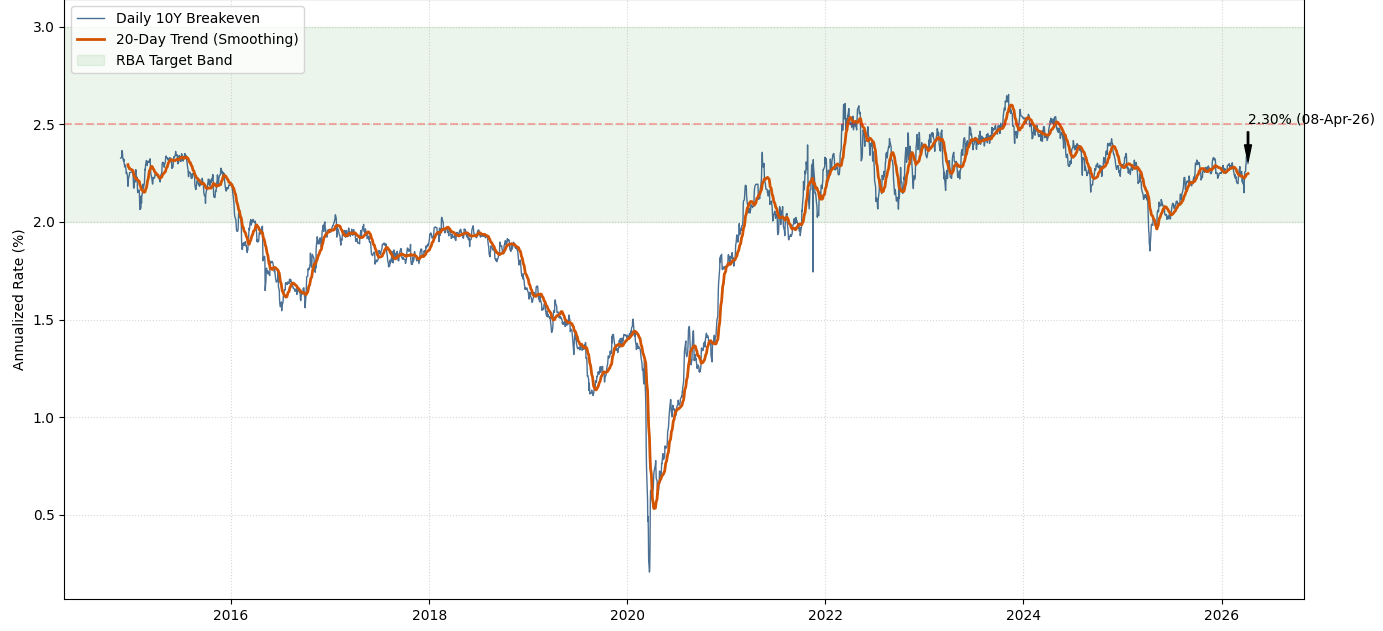

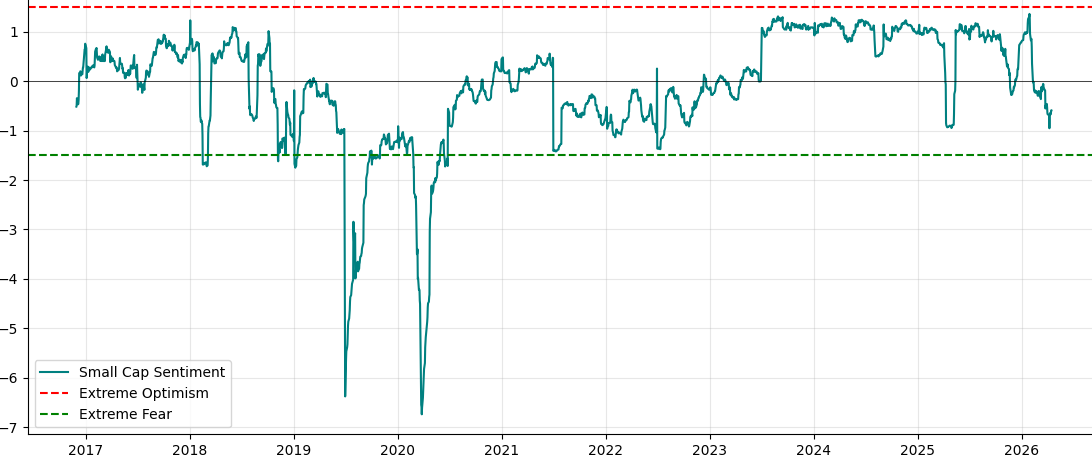

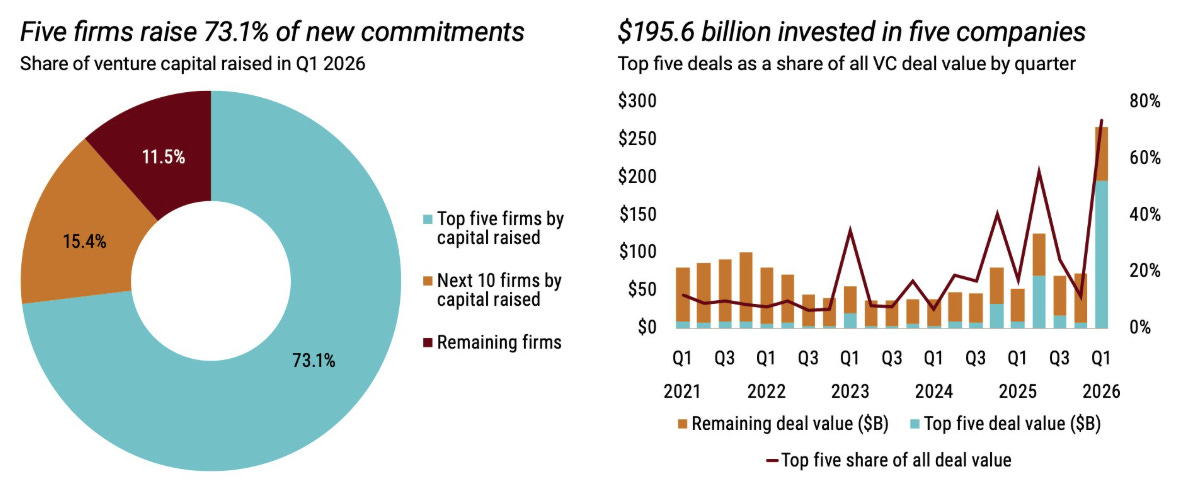

10k Words Equitable Investors April 2026 (2-minute read) We couldn't help but look at geopolitical risk again - with the spike in a longer historical context than shown last month. Fertiliser prices are spiking in the wake of the Middle East situation. Yet the "breakeven" inflation rate based on Australian 10-year bonds remains at a relatively normal level, implying short term shocks are expected to have modest long-term ramifications. Our sentiment scores show ASX large cap sentiment rebounding but small caps trailing. The US experience has shown a large cap rebound of rare magnitude in recent days. Meanwhile, we talk about index concentration in the stock market but take a look at recent concentration in the world of venture capital. We divert to the recently-depressed valuation metrics for the tech sector. Then on to redemptions at leading private credit house Blue Owl Capital. Finally, energy consumption and income go hand-in-hand and we take a look at Australia's national debt stack. Geopolitical Risk Index relative performance to VIX (US volatility) over 20 years

Source: Caldara and Iacoviello, Koyfin Fertiliser price spikes and war

Source: Bloomberg Aus 10-year bond yield-derived breakeven inflation rate: 2014 to Apr 2026

ASX sentiment score (yield spread + VIX)

Source: St Louis Fed, Equitable Investors ASX small cap sentiment score

Source: Koyfin S&P 500 rallying 9.8% in 10-days - the 99.7th percentile of all 10 day returns

Source: 3Fourteen Research ~75% of all VC funds raised by just five firms & invested in five companies

Source: Pitchbook NVCA Venture Monitor, as of March 31, 2026 US tech sector PEG ratio (historical earnings growth)

Source: Goldman Sachs Global Investment Research Average EV/Revenue multiple (next 12 months revenue forecast) for Software industry

Source: Apollo, Illiquid Insights Blue Owl quarterly redemption requests as a % of shares outstanding

Source: Global Markets Investor US leveraged loan defaults: trailing 12-month count

Electricity & Income (per capita)

Source: EIEA, World Bank, @JoeNakamato National gross debt of Australia

Source: IFM Investors Funds operated by this manager: Equitable Investors Dragonfly Fund Disclaimer Past performance is not a reliable indicator of future performance. Fund returns are quoted net of all fees, expenses and accrued performance fees. Delivery of this report to a recipient should not be relied on as a representation that there has been no change since the preparation date in the affairs or financial condition of the Fund or the Trustee; or that the information contained in this report remains accurate or complete at any time after the preparation date. Equitable Investors Pty Ltd (EI) does not guarantee or make any representation or warranty as to the accuracy or completeness of the information in this report. To the extent permitted by law, EI disclaims all liability that may otherwise arise due to any information in this report being inaccurate or information being omitted. This report does not take into account the particular investment objectives, financial situation and needs of potential investors. Before making a decision to invest in the Fund the recipient should obtain professional advice. This report does not purport to contain all the information that the recipient may require to evaluate a possible investment in the Fund. The recipient should conduct their own independent analysis of the Fund and refer to the current Information Memorandum, which is available from EI. |

8 May 2026 - Performance Report: 4D Global Infrastructure Fund (Unhedged)

[Current Manager Report if available]

8 May 2026 - Hedge Clippings | 08 May 2026

|

|

|

|

Hedge Clippings | 08 May 2026

This week saw the RBA meet most market observers' expectations by increasing rates by 0.25% - the second such move in a row, taking them back up to their previous post-COVID peak, and eradicating the three rate cuts they made last year. Hedge Clippings checked in with our regular contributors, Nick Chaplin from Seed Funds Management, and Renny Ellis from Arculus Funds Management, to get their respective views on the wisdom - or otherwise - of the Bank's decision. Both were broadly united in the view that the RBA's latest 0.25% rate rise to 4.35% may have been widely anticipated, but was poorly timed, and raised more questions than it answered. Nick Chaplin argued the move effectively reverses last year's rate cuts, taking the cash rate back to where it was before the RBA began easing. His central concern was the distinction between temporary inflation pressures and persistent inflation. With the trimmed mean holding at 3.3%, he questioned whether the RBA was reacting too heavily to energy-driven price pressures and their knock-on effects through logistics and household costs. While he accepted the Bank is right to be focused on inflation, he was skeptical of its approach, particularly the continued reliance on incremental 0.25% increases. If the RBA believes inflation risks are still rising, Nick suggested it may need to be clearer about where rates are heading, with the possibility that the cash rate could move as high as 4.85% before year-end. Renny Ellis was more direct, describing the energy shock as transitory and arguing the RBA should have looked through it, at least until the June meeting. His concern is not that inflation should be ignored, but that the Bank has acted before the full economic impact of the previous two rate increases has flowed through. Renny also warned that the decision was made ahead of a Federal Budget due next week that may include higher taxes, housing-related measures and household handouts, all of which could materially alter the economic outlook. Both Nick and Renny highlighted the risk that policy is now being tightened into a fragile environment. Ellis was particularly concerned about the potential for diesel rationing, arguing that it would almost certainly push Australia into recession. He drew a sharp contrast with 2020, when both the RBA and the Federal Government acted aggressively to avoid recession, noting that Australia's high household debt levels make a downturn especially dangerous. A key point from Renny was that the usual transmission mechanisms for monetary policy look less effective in the current environment. With the Australian dollar already strong, he questioned how higher rates would help beyond depressing house prices and household spending. Nick added that a stronger dollar could itself make it harder for the economy to avoid recession, particularly given Australia's past reliance on currency weakness and resource exports to cushion downturns. Both agreed that further rate increases may still become necessary later in the year, particularly if wages growth, the Fair Work Commission decision, fiscal policy and household spending keep demand elevated. However, both also argued that this was not the right moment to move. Their central criticism was not that inflation is irrelevant, but that the RBA has acted in a period of unusually poor visibility, with energy markets, the Budget and household stress all still unfolding. So as Renny questions in the video below, that leaves the potential that we are headed not for the "recession we had to have" but for the "recession we can't afford"? The outcome or length of a one-page, paper-thin, so-called truce in the Middle East could tip the balance. News | Insights

Manager Insights | Altor Capital Stock Story: Ampol | Airlie Funds Management Property Update | Australian Secure Capital Fund April 2026 Performance News Bennelong Australian Equities Fund 4D Global Infrastructure Fund (Unhedged) Quay Global Real Estate Fund (Unhedged) Active ETF (ASX:QGRU) |

|

|

If you'd like to receive Hedge Clippings direct to your inbox each Friday |

8 May 2026 - Performance Report: Bennelong Australian Equities Fund

[Current Manager Report if available]

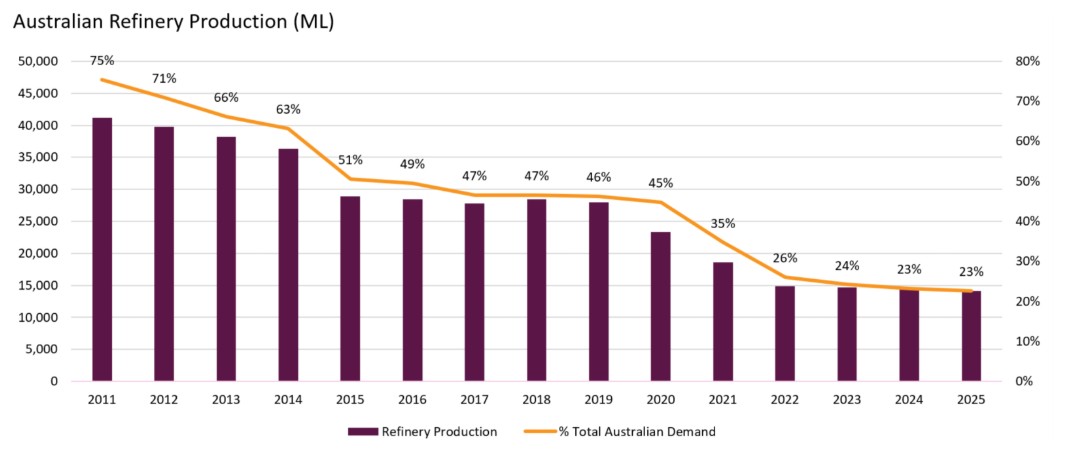

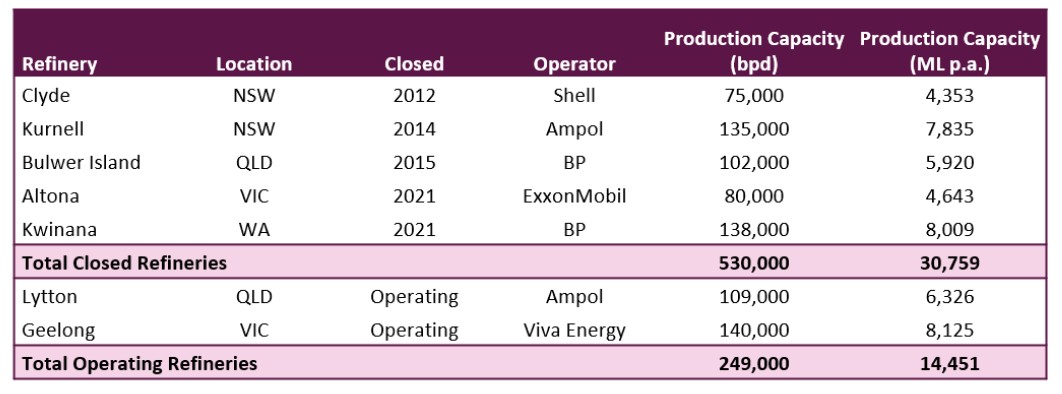

6 May 2026 - Stock Story: Ampol

|

Stock Story: Ampol Airlie Funds Management April 2026 (5-minute read) |

|

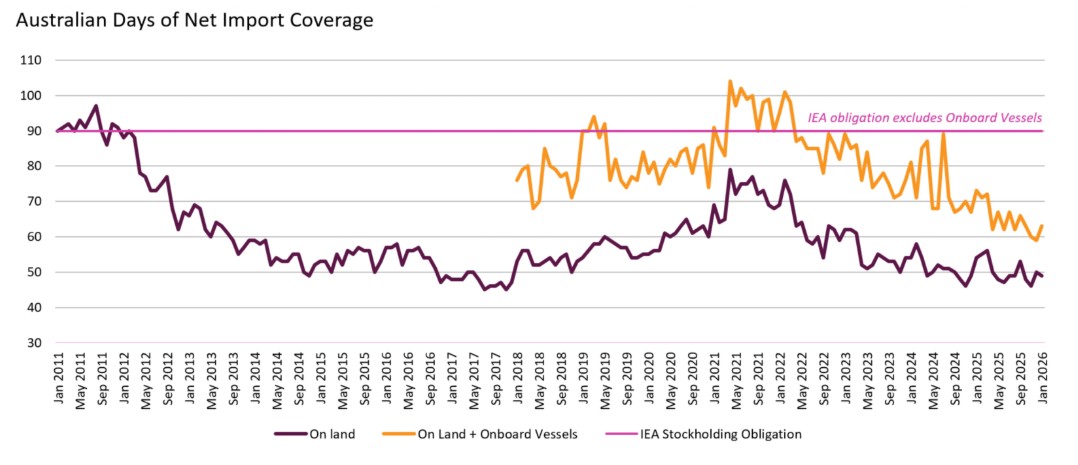

Pathway to unlocking value outside the headlines. Ampol is Australia's largest fuel refiner and distributor, playing a critical role in supplying fuel to Australian consumers and industries. While Ampol is widely recognised for its national convenience retail network, we believe the market underappreciates the strategic value of their Lytton refinery asset. Lytton is one of only two remaining refineries in Australia. While the recent Iran conflict has drawn attention to the importance of fuel security in Australia, we see the real catalyst for value realisation sitting not in the headlines themselves, but in the evolving policy discussions that underpin Lytton's long-term earnings. Australia's refining capacity has deteriorated dramatically over the past 15 years. In 2011, the country operated seven refineries, supplying around 75% of domestic fuel demand. Today, only two refineries remain, these being Ampol's Lytton Refinery in Brisbane and Viva Energy's Geelong Refinery. Combined, these refineries meet just 20% of Australia's fuel needs. The balance of fuel is imported as refined product, predominantly from South Korea, Singapore, Malaysia, China and Japan. As Australia has shifted from refining self-sufficiency to import dependence, the strategic value of these last two refineries has grown considerably, given their role in national fuel security.

The outbreak of the war against Iran and subsequent closure of the Strait of Hormuz triggered a major global supply disruption. Notably, Ampol does not use Middle Eastern crude oil, yet the cascading effects on Asian refining production and product flows still materially affected supply chains into Australia. With Australia's fuel stockholdings well below the IEA's 90-day requirement, concerns around supply security were heightened.

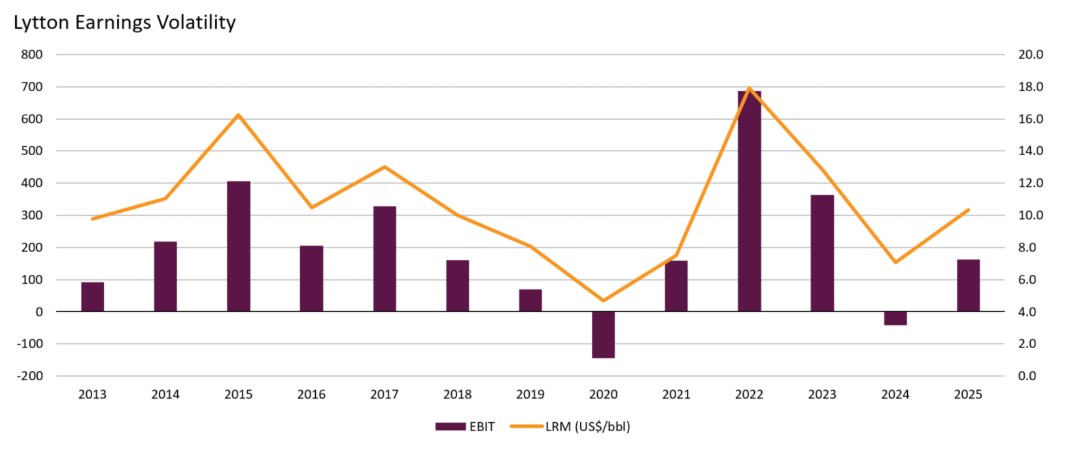

Ampol is Australia's largest fuel refiner and distributor, playing a critical role in supplying fuel to Australian consumers and industries. While Ampol is widely recognised for its national convenience retail network, we believe the market underappreciates the strategic value of their Lytton refinery asset. Lytton is one of only two remaining refineries in Australia. While the recent Iran conflict has drawn attention to the importance of fuel security in Australia, we see the real catalyst for value realisation sitting not in the headlines themselves, but in the evolving policy discussions that underpin Lytton's long-term earnings. Australia's refining capacity has deteriorated dramatically over the past 15 years. In 2011, the country operated seven refineries, supplying around 75% of domestic fuel demand. Today, only two refineries remain, these being Ampol's Lytton Refinery in Brisbane and Viva Energy's Geelong Refinery. Combined, these refineries meet just 20% of Australia's fuel needs. The balance of fuel is imported as refined product, predominantly from South Korea, Singapore, Malaysia, China and Japan. As Australia has shifted from refining self-sufficiency to import dependence, the strategic value of these last two refineries has grown considerably, given their role in national fuel security. On a regulated basis, we estimate Lytton's value at $1.5-2.0 billion, compared to our estimate of the market's current implied valuation of less than $1.0 billion. This gap implies $3-$5 per share of incremental value to Ampol's current share price from the Lytton re-rate alone, before considering further upside from the EG Group acquisition and the rollout of U-GO conversions across the convenience retail network.

Funds operated by this manager: Airlie Australian Share Fund , Airlie Small Companies Fund Important Information: This material has been delivered to you by Magellan Asset Management Limited ABN 31 120 593 946 AFS Licence No. 304 301 trading as Airlie Funds Management ('Airlie') and has been prepared for general information purposes only and must not be construed as investment advice or as an investment recommendation. This material does not take into account your investment objectives, financial situation or particular needs. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer documentation, offer or invitation to purchase, sell or subscribe for interests in any type of investment product or service. You should obtain and consider the relevant Product Disclosure Statement ('PDS') and Target Market Determination ('TMD') and consider obtaining professional investment advice tailored to your specific circumstances before making a decision about whether to acquire, or continue to hold, the relevant financial product. A copy of the relevant PDS and TMD relating to an Airlie financial product or service may be obtained by calling +61 2 9235 4760 or by visiting www.airliefundsmanagement.com.au. Past performance is not necessarily indicative of future results and no person guarantees the future performance of any financial product or service, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. This material may contain 'forward-looking statements'. Actual events or results or the actual performance of an Airlie financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. This material may include data, research and other information from third party sources. Airlie makes no guarantee that such information is accurate, complete or timely and does not provide any warranties regarding results obtained from its use. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of Airlie. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. No representation or warranty is made with respect to the accuracy or completeness of any of the information contained in this material. Airlie will not be responsible or liable for any losses arising from your use or reliance upon any part of the information contained in this material. Any third party trademarks contained herein are the property of their respective owners and Airlie claims no ownership in, nor any affiliation with, such trademarks. Any third party trademarks that appear in this material are used for information purposes and only to identify the company names or brands of their respective owners. No affiliation, sponsorship or endorsement should be inferred from the use of these trademarks. This material and the information contained within it may not be reproduced, or disclosed, in whole or in part, without the prior written consent of Airlie. |

5 May 2026 - Australian Secure Capital Fund - Property Update

|

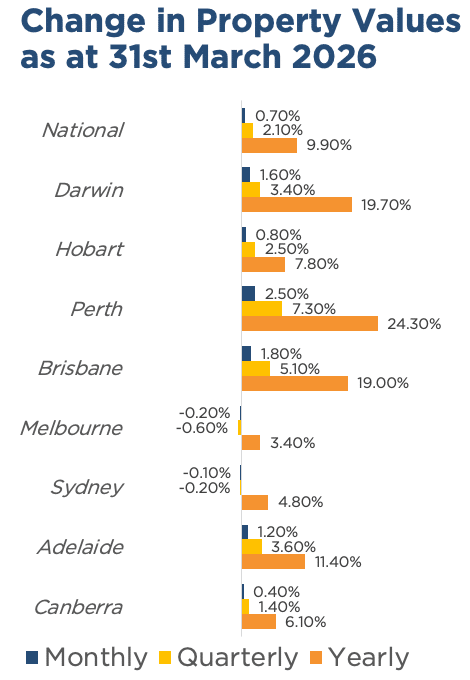

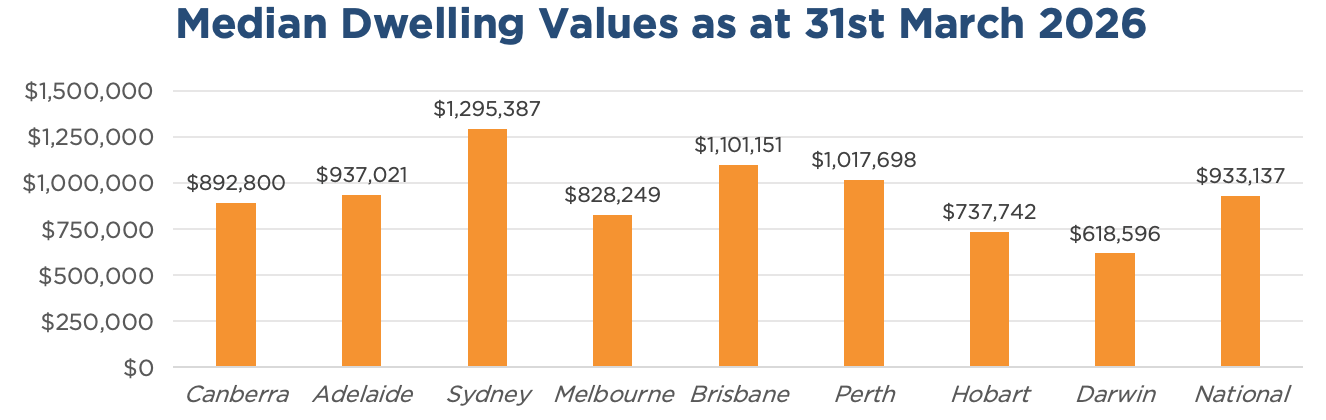

Australian Secure Capital Fund - Property Update Australian Secure Capital Fund March 2026 (1-minute read) March was another steady month for Australian property values, posting a national rise of 0.7%, down slightly from 0.8% in February.

Once again, Perth (+2.5%) led the way with a third consecutive monthly rise of greater than 2%, with the annual increase now reaching 24.3%. Likewise, Brisbane (+1.8%) and Adelaide (+1.2%) continued to add value, again posting monthly increases of greater than 1%. Conversely, values in Melbourne (-0.2%) and Sydney (-0.1%) declined for a second straight month, with the cities notching rolling quarterly declines of -0.6% and -0.2%, respectively. Due to this, regional areas (+1.1%) continue to outpace the capitals (+0.6%) by nearly double, with regional WA leading the way, posting a 6.2% quarterly increase.

Source: Cotality HVI, 02 April 2026 March Edition Funds operated by this manager: ASCF Select Income Fund , ASCF High Yield Fund , ASCF Premium Capital Fund , ASCF Private Fund

|